|  |

|  |

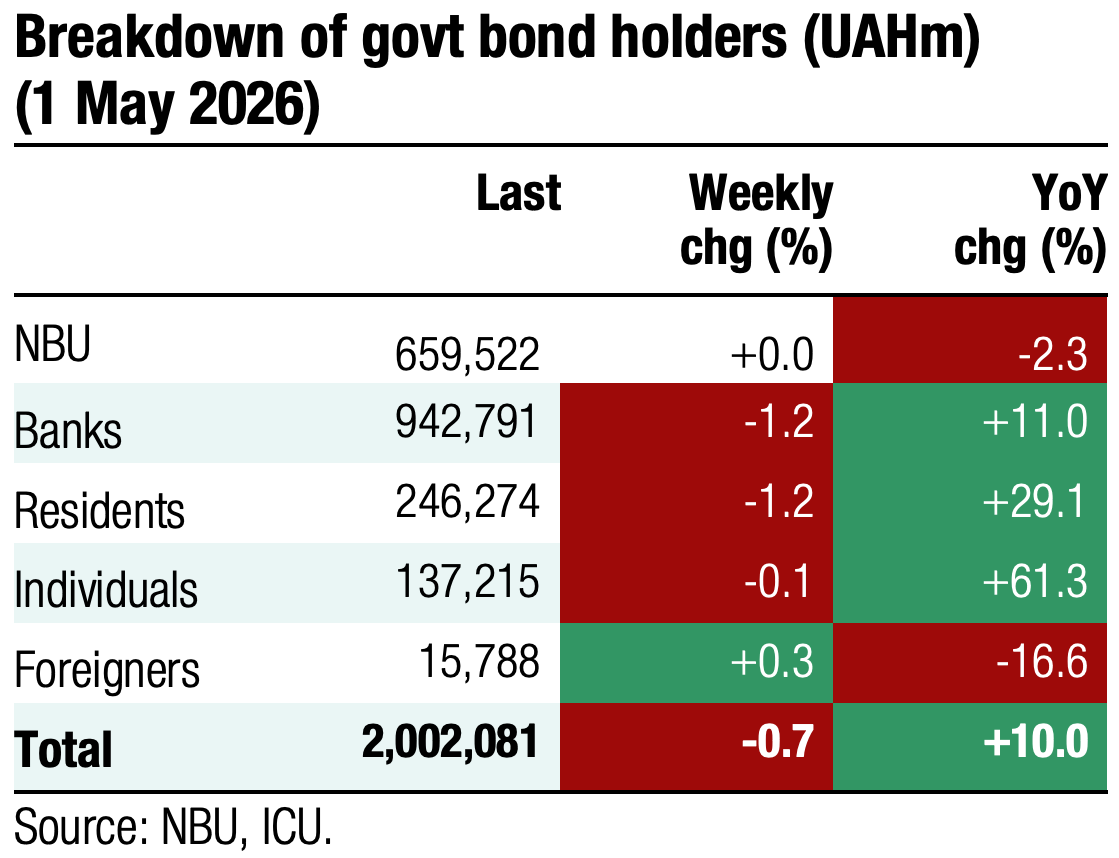

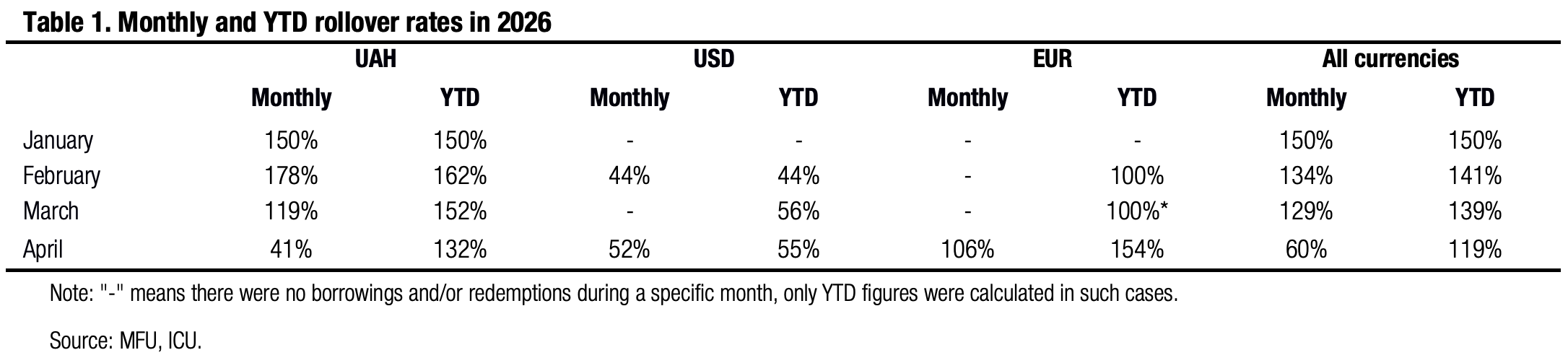

Bonds: MoF reduces local debt rollover sharply in April

In April, the MoF significantly reduced borrowings in the local debt market compared with previous months.

The MoF redeemed almost UAH38bn of domestic bonds in April: UAH20bn of UAH bonds that includes UAH5.7bn of bonds due in May exchanged for longer securities in April, as well as US$192m and EUR189m of FX-denominated bonds. However, the ministry sold only UAH22.8bn worth of bonds, including bonds issued for the exchange. Thus, the debt rollover was just 60% in April.

For 4M26, the domestic debt rollover decreased to 119% from 139% in 1Q26. The rollover rate was 132% for hryvnia debt (152% in 1Q26), remained at 55% for debt in USD, and was set at 154% in EUR thanks to debut issuance this year.

All in, net redemption stood at UAH15.2bn across all currencies in April after net borrowings were positive in each of the first three months of the year. In total, in 4M26, net borrowings amounted to UAH28bn, significantly down from UAH43.1bn in 1Q26.

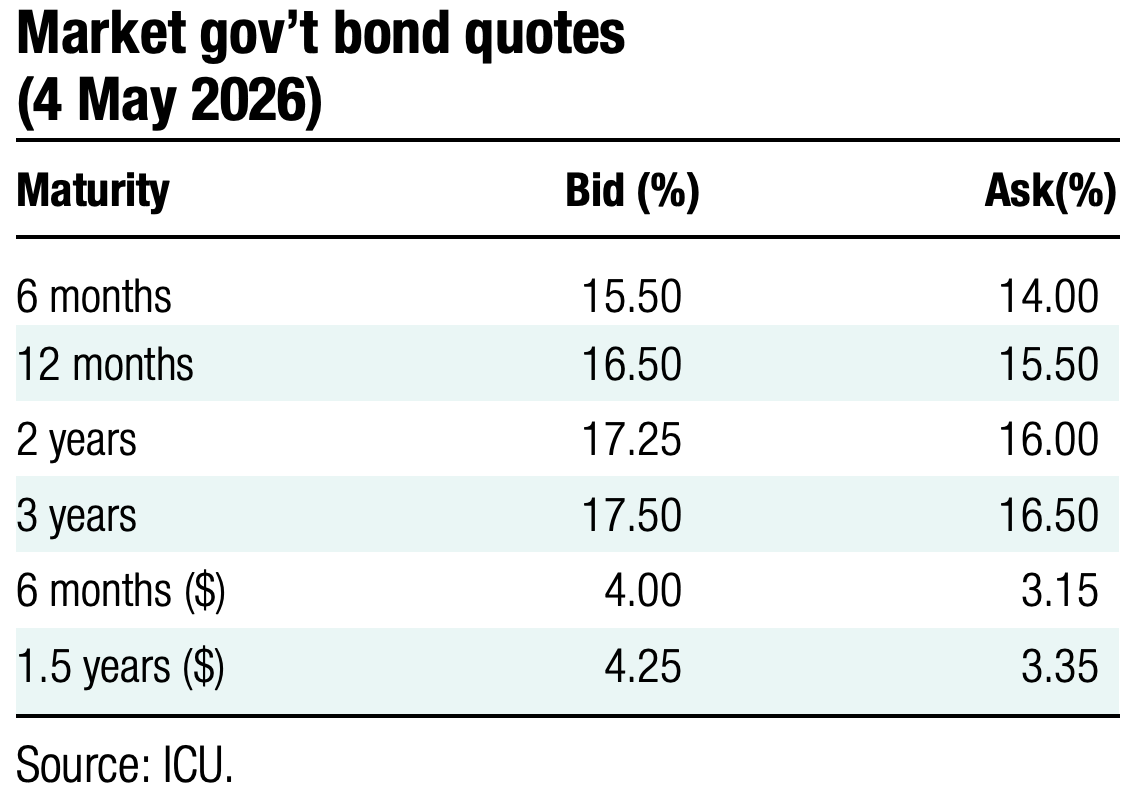

ICU view: The EU has finally approved a two-year EUR90bn loan to Ukraine, of which EUR16.7bn will be disbursed for this year’s budgetary needs. The first tranche could be in as early as 2Q26. Therefore, the MoF is unlikely to step up domestic borrowing considerably. It will likely gradually continue towards a cumulative 100% rollover after net borrowings were significant at the beginning of the year due to a temporary lack of external assistance. Given that and the NBU's decision to keep the key policy rate unchanged (see comment below), the Ministry of Finance will maintain the current yield terms for the UAH bonds in the primary bond market for an extended period of time.

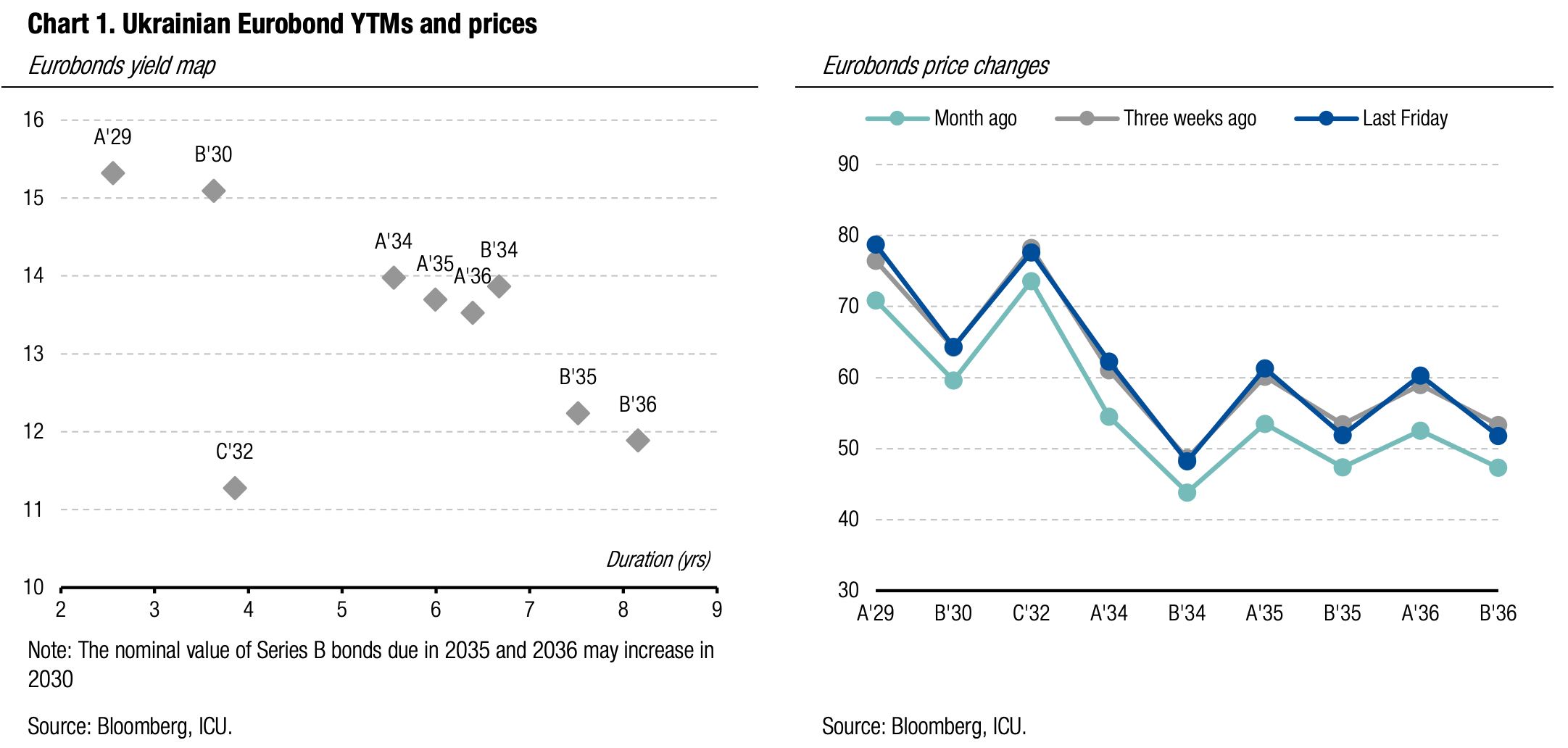

Bonds: Ukrainian Eurobonds follow global EM trend

The delays in US-Iran negotiations have had little impact on general investor sentiment towards emerging markets. Ukrainian Eurobond prices followed broader market trends.

The US stopped active military operations in Iran, and moved to blockade Iranian ports to maintain pressure for peace negotiations. Despite the blockade—that commenced on April 13—the general sentiment towards emerging markets has not changed significantly: the EMBI index moved less than 0.2% in three weeks. Ukrainian Eurobonds were in line with the trend in emerging-market bond prices, especially amid positive news about the EU financing for Ukraine being finally approved. Ukrainian Eurobond prices have fluctuated within a few cents for the past three weeks and remained almost unchanged after a small rally in early April.

ICU view: The trilateral talks among Ukraine, the US, and russia show little signs of life. The US is focusing on Iran's nuclear program and gradually increasing pressure on Cuba, while the russia war in Ukraine seems to be below radar for a while. Russia continues to insist on the withdrawal of Ukrainian troops from Donbas, and Ukraine has unequivocally rejected the idea. At this point there are no clear triggers that may accelerate peace talks in the near future.

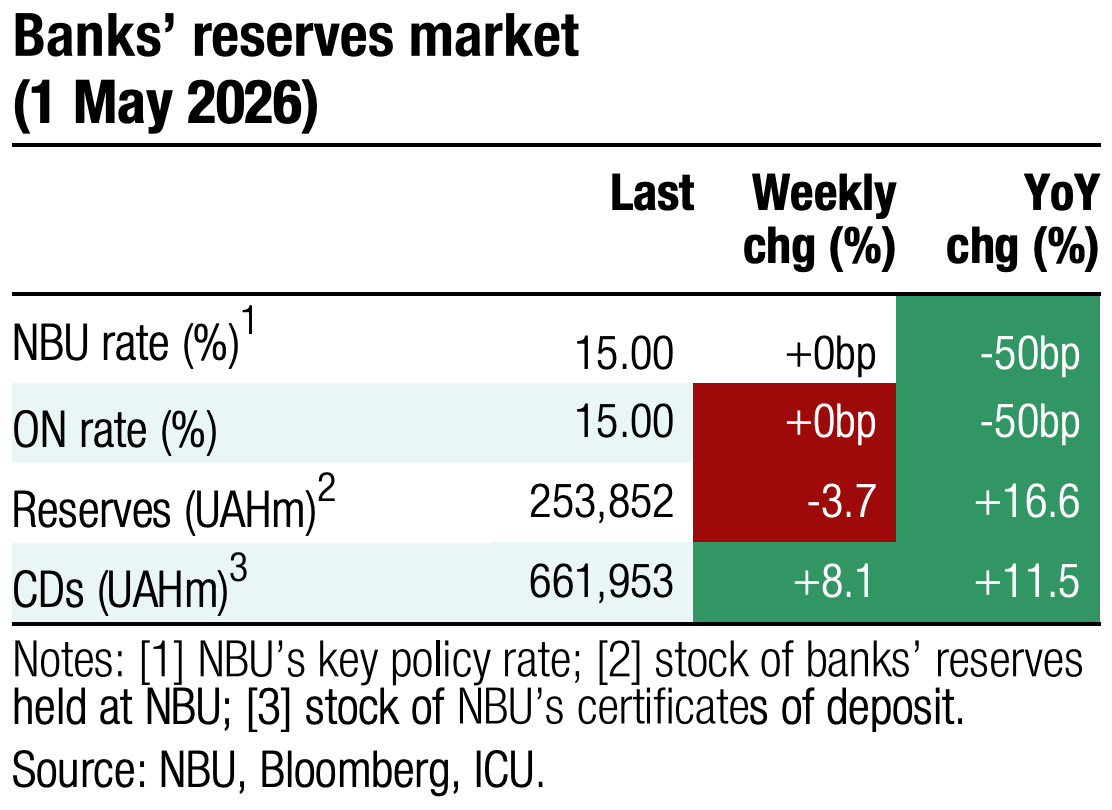

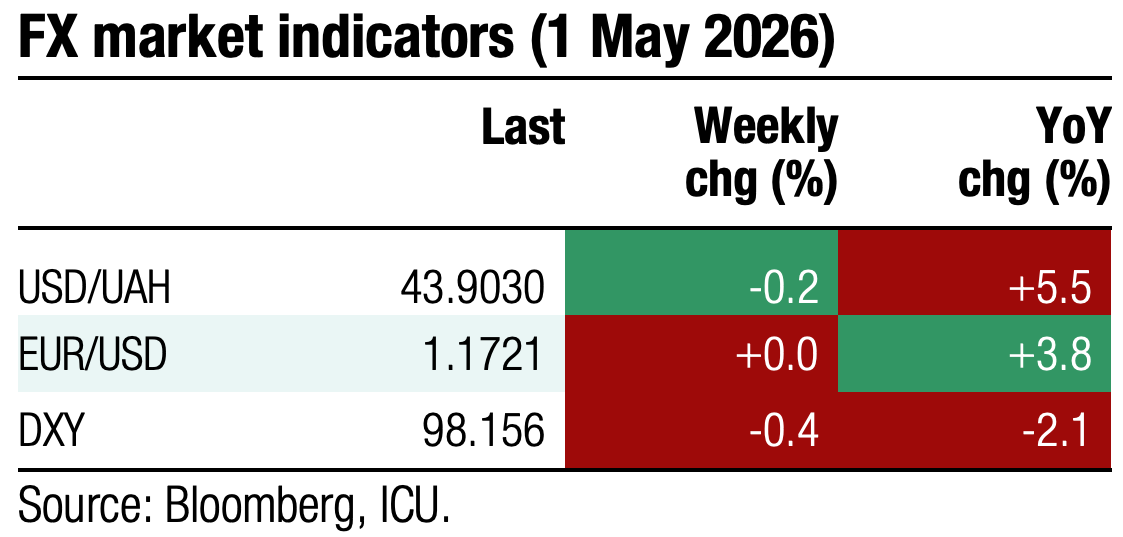

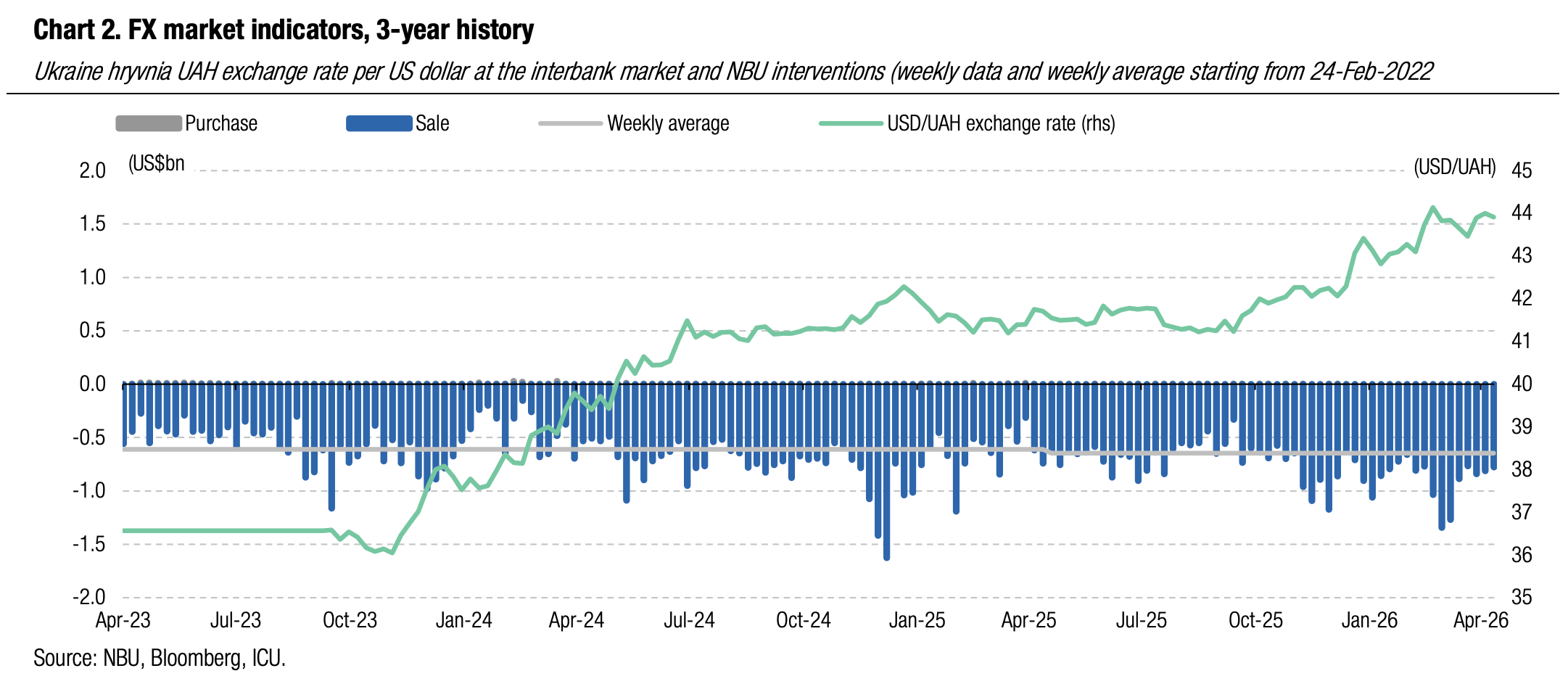

FX: NBU managed to stabilise FX market

After a sharp increase in the FX deficit in late March, the NBU managed to offset excess demand and stabilise both the market and the hryvnia exchange rate.

During April, the NBU allowed fluctuations of the official hryvnia rate in the range of UAH43.38—44.12/US$, and for the month the hryvnia weakened by 0.1% against the US dollar and by 2% against the euro. The hryvnia weakened by 3.8% YTD vs. the US dollar and 3.3% YTD vs. the euro.

The FX market shortage significantly narrowed in April after this year's record imbalances at the end of March. The weekly hard currency deficit fluctuated around US$700m during the month. Yet, last week, the deficit subsided significantly vs. the previous weeks.

NBU weekly interventions stood at US$3.6bn, a quarter less than in March. In 4m26, the sale interventions reached US$15.1bn, which is a 29% YoY increase.

ICU view: The NBU allows a fairly wide range of fluctuations in the hryvnia-US dollar rate. However, it shows little appetite for an even stronger devaluation of the hryvnia. The NBU revised the inflation forecast up vs. the January expectation and signalled monetary policy easing may not resume until 2027. The central bank aims to maintain high nominal yields to ensure UAH-denominated assets are attractive enough. To ensure this principle is maintained and to prevent excessive inflationary acceleration, the NBU is unlikely to change its exchange rate policy and will maintain a very gradual pace of hryvnia devaluation. Accordingly, we maintain our year-end exchange rate forecast at UAH45/US$.

Economics: NBU worsens macro outlook

The NBU kept its key policy rate at 15.0% and now expects it to remain unchanged through April 2027.

The revision reflects faster-than-projected inflation, a deterioration in household inflation expectations, and elevated global energy prices following the escalation of the Middle East war. Fuel prices rose sharply in recent weeks, with direct and secondary pass-through effects expected to push end-year CPI above the January forecast of 7.5%, now projected at 9.4% by December. The NBU signalled that, should inflation expectations deteriorate further and actual CPI approach double-digit levels, a rate hike cannot be ruled out.

External financing assumptions remain within the January baseline, with the €90bn EU Ukraine Support Loan and IMF program disbursements treated as the base case. International reserves remain elevated, providing a buffer for currency market stability.

ICU view: The NBU's revised rate trajectory — on hold through April 2027 — is consistent with our view that the easing cycle is effectively suspended for an extended period. A rate hike remains a tail risk rather than a base case, contingent on sustained deterioration in CPI dynamics and expectations. We see no basis for cuts resuming before mid-2027 absent a significant and broad-based improvement in the inflation and external risk outlook.

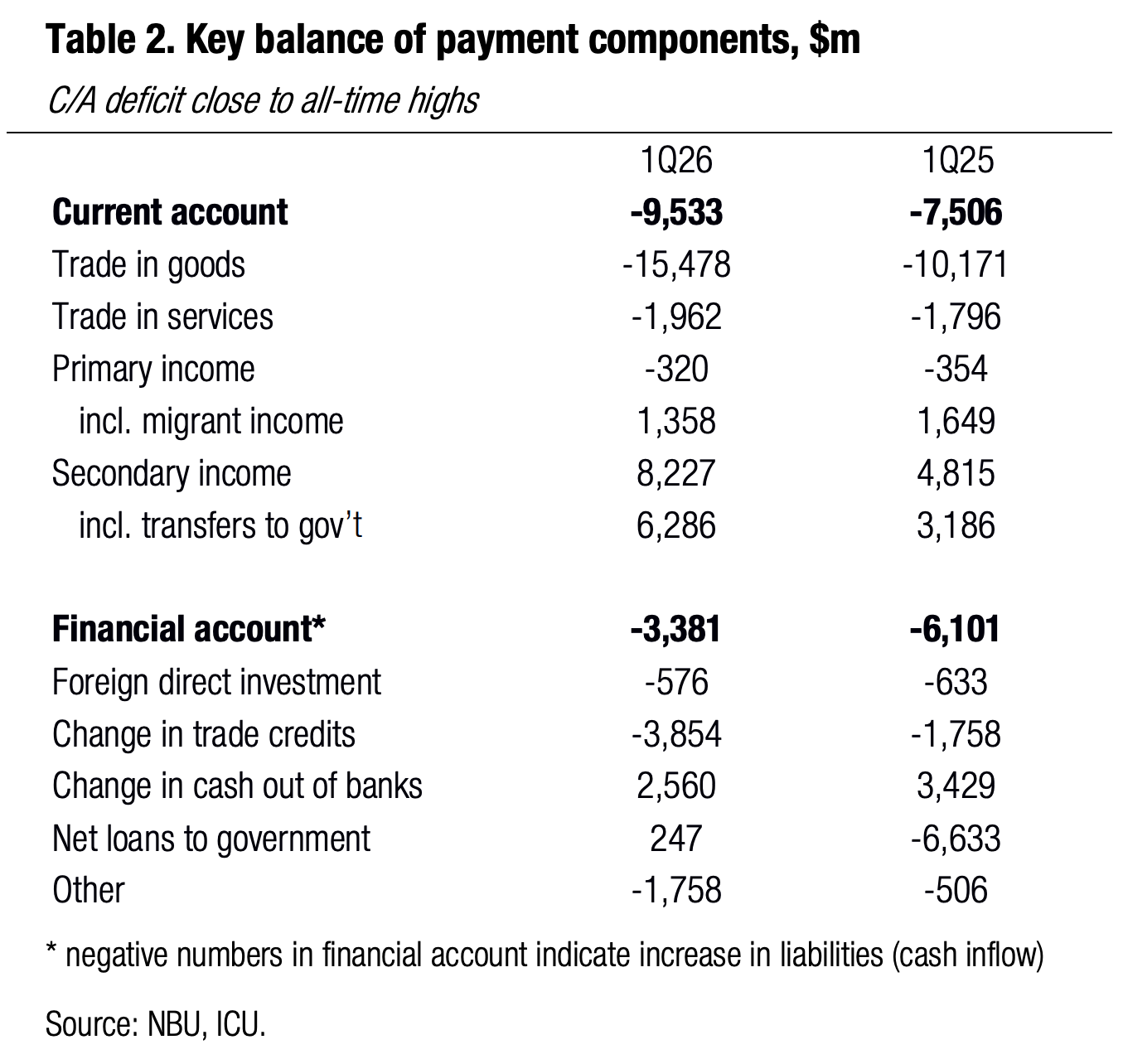

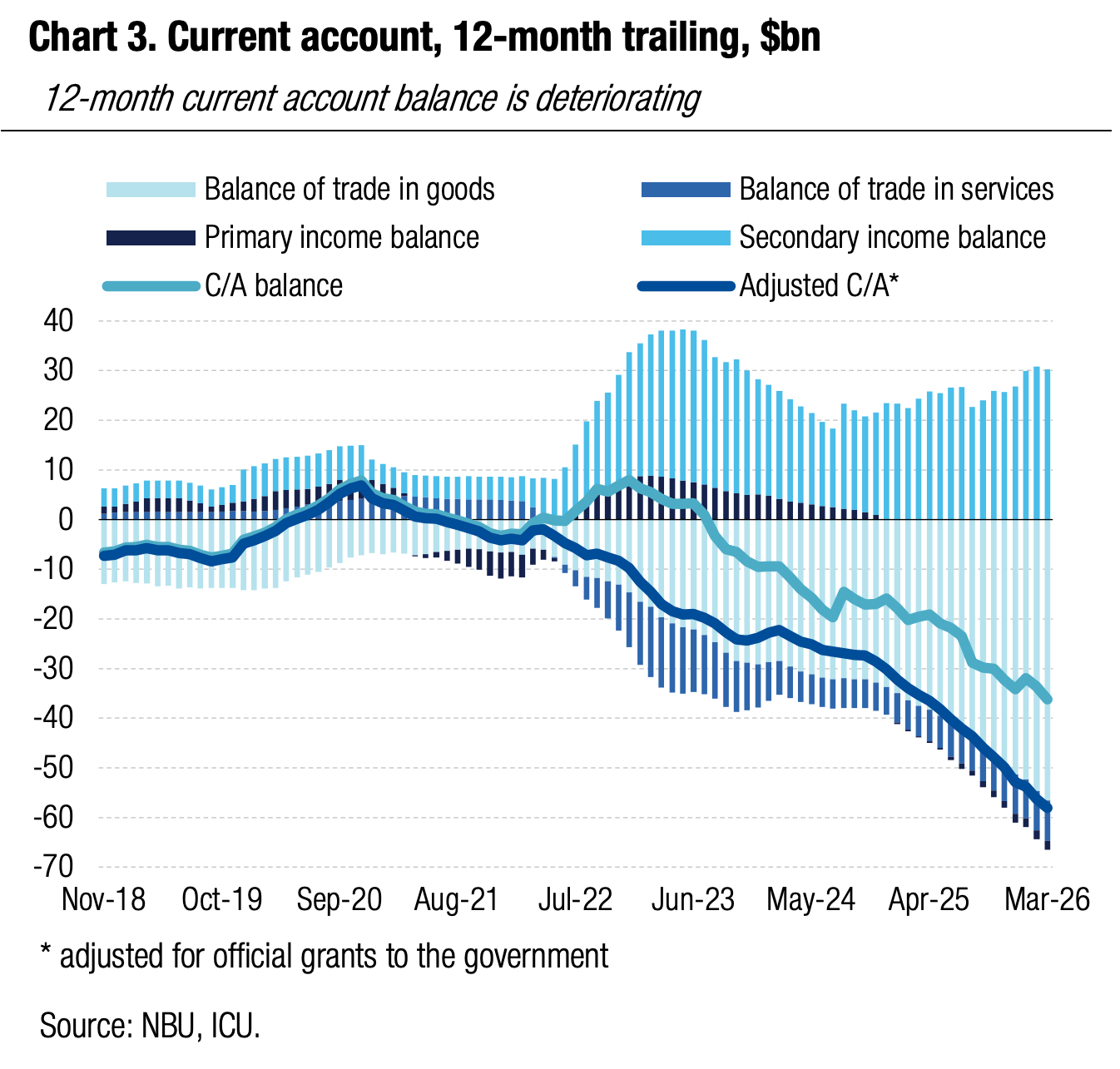

Economics: External accounts deteriorate in 1Q26

Ukraine’s current account (C/A) deficit reached US$9.5bn in 1Q26 vs. US$7.5bn in 1Q25 as foreign trade-in-goods gap surged.

Import of goods was up by a third in 1Q26 primarily driven by machinery & equipment and mineral products, including motor fuel. Export of goods remained nearly flat YoY, propelling the trade-in-goods shortfall to US$15.5, close to all-time highs. The balance of trade in services remained nearly flat YoY with both export and import little changed vs. 1Q25. Primary income was also almost unchanged as a weaker inflows of labor income of Ukrainians abroad was offset with a comparable decline in non-resident dividend and interest incomes in Ukraine. Secondary income surplus was hefty at US$8.2bn, largely due to inflows of ERA facility to the government’s accounts.

The financial account remained in surplus even in the absence of foreign official credits to the government in 1Q26 (all financial aid was channeled as grants during the quarter). The key channels for capital inflows within the financial account was a reduction of the stock of trade credits, with FDI complementing the flow, albeit to a much smaller extent. Increase in cash out of banks (purchases and withdrawal of FX cash by the population) remained the key drag, but was down ¼ YoY.

Net capital inflows via the financial account were not sufficient to offset the C/A gap, implying the NBU reserves were under pressure and declined 9% QoQ to US$52.0bn.

|  |

ICU view: Imbalances of external accounts (net of foreign financial aid) continue to grow, yet the regular inflows of foreign financial aid helps keep the gap fully covered. With the Ukraine Support Loan from the EU now secured, we expect much the same pattern at least through end-2027. Inflows of official funding will remain hefty, yet further widening of external imbalances is an alarming signal and will likely force the NBU to maintain a gradual hryvnia depreciation trend going forward.