|  |

|  |

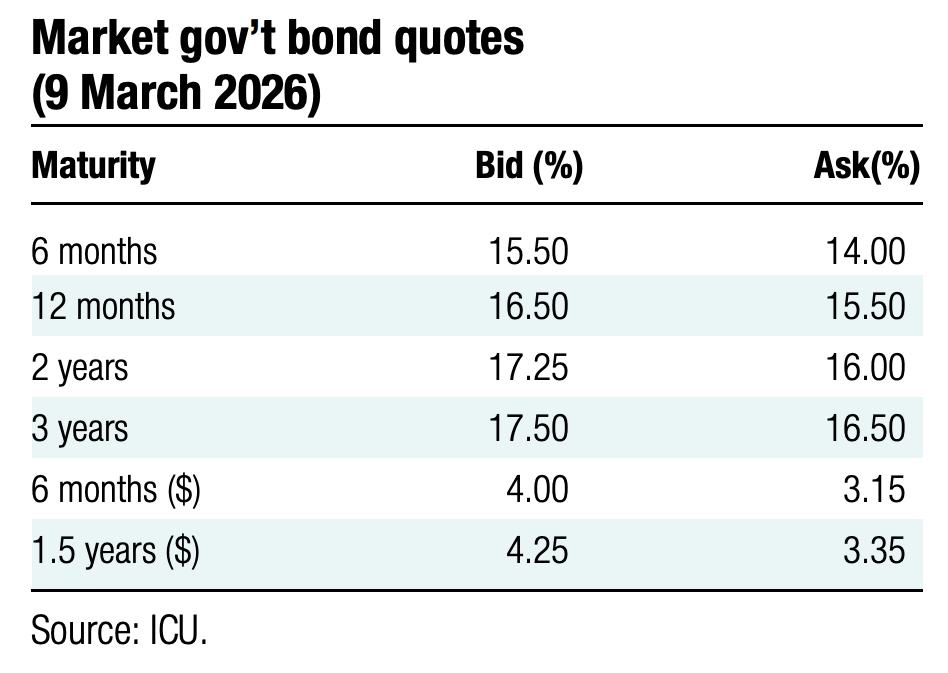

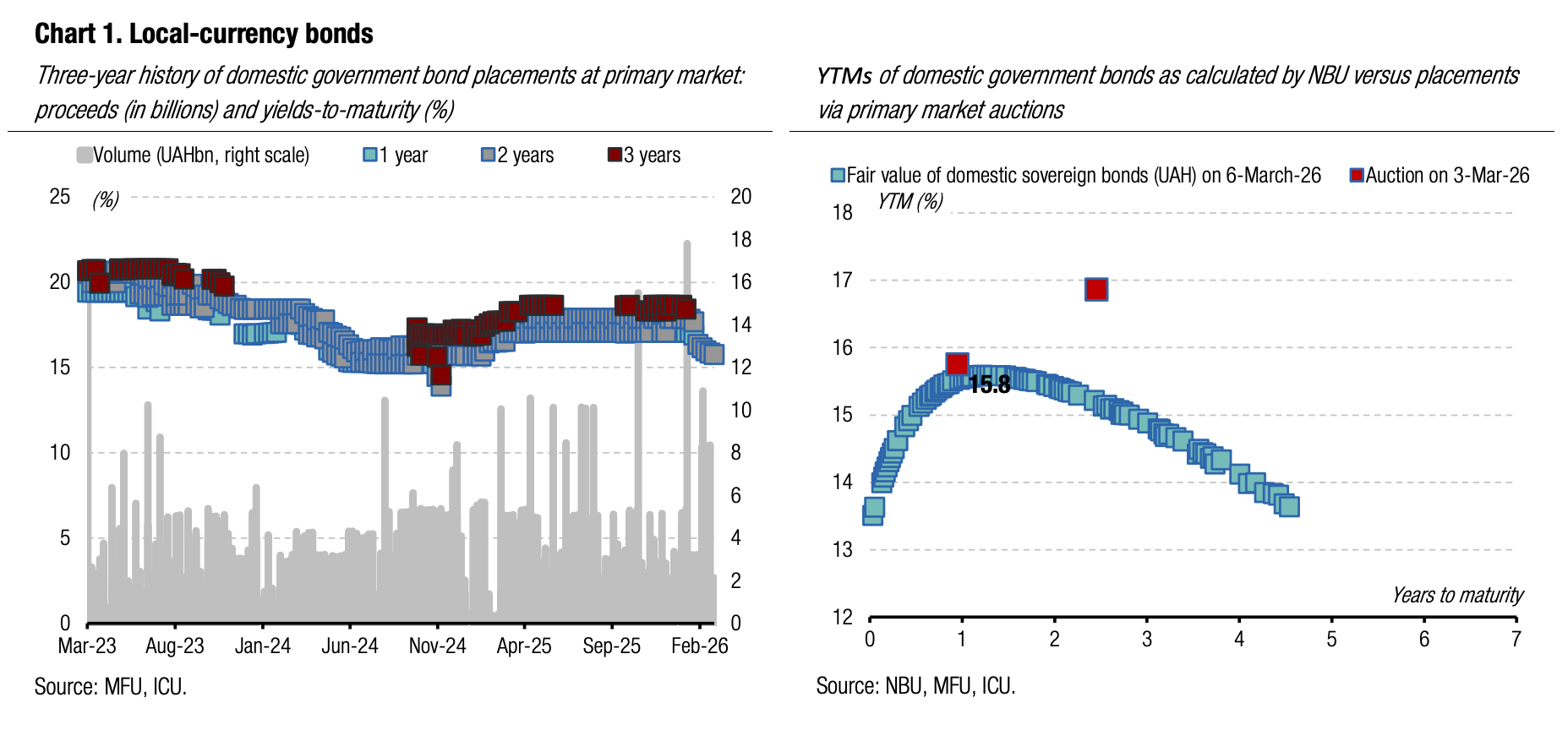

Bonds: New round of rate cuts by MinFin

Last week, the Ministry of Finance continued to cut yields in the primary bond market, but the room for further rate adjustments is narrowing.

Cut-off rates decreased again last week to 15.19% for one-year government bonds and 16.20% for three-year bonds (see the auction review for details). However, the noteworthy thing last week was that the minimum bid rate for a one-year bill remained unchanged at 15.1%, and for a three-year note it even edged down to 15.99%. Thus, the cut-off rates were very close to the minimum bid rates.

For tomorrow, the Ministry of Finance announced an offering of the usual one-year paper and a new two-year UAH bond. The new security will have a maturity of June 14, 2028. The MoF last sold a similar instrument before the NBU switched to monetary policy easing, so we can only make guesses about MinFin’s target yield on the new security. Given the current rates on one-year and three-year bonds, the new issue may yield in the range of 15.6%-15.8%. This roughly implies a premium of 40-50bp for the two-year bond vs one-year securities.

ICU view: The MoF currently has very limited room for further yield cuts in the primary market until the NBU makes another step to cut the key policy rate. The NBU key rate is currently 15%, and the yields on one-year bills in the primary market are 15.1%-15.19%. Therefore, the Ministry of Finance may face challenges if it tries to push the rate lower without the NBU revisiting its forecasts of the key rate trajectory. However, for longer-term securities, the MoF may maintain its efforts to reduce the term premium from the current 50bp for each additional year of maturity to approximately 40bp.

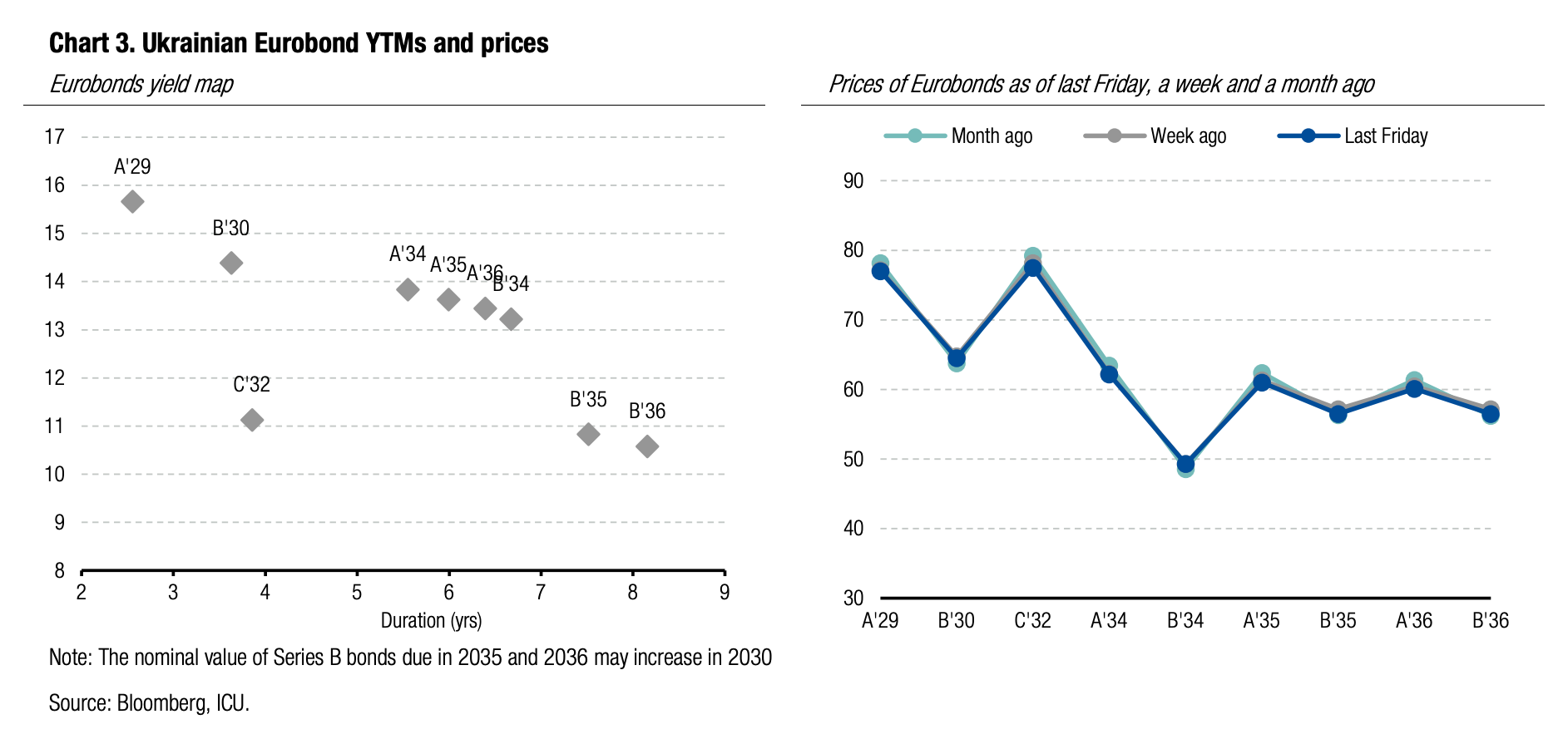

Bonds: Bondholders cooling off as excessive optimism wanes

Ukrainian Eurobond prices fell slightly over the past few weeks as bondholders' optimism about the peace talks has once again proven overblown.

The lack of progress in the peace talks, once again, is yet another sign that the market tends to take signals from the trilateral meetings of the US, Ukraine, and russia in an overly optimistic manner. Ukraine Eurobond prices began to decline in mid-February. With the outbreak of war in Iran, sentiment towards emerging market debt markets worsened notably – the EMBI index fell by 1.6% last week. Global sentiment has only exacerbated the decline in Ukrainian bond prices by over 5% over the past three weeks.

ICU view: The war in Iran is indirectly affecting Ukraine, both through a change in the focus of the global news and through a forced pause in peace talks. At present, events in Iran are more likely to be negative due to a possible reduction in the supply of critical ammunition for Ukraine, such as air defence missiles. The next round of negotiations has been postponed, leaving investors without any new guidance about prospects for a peace deal.

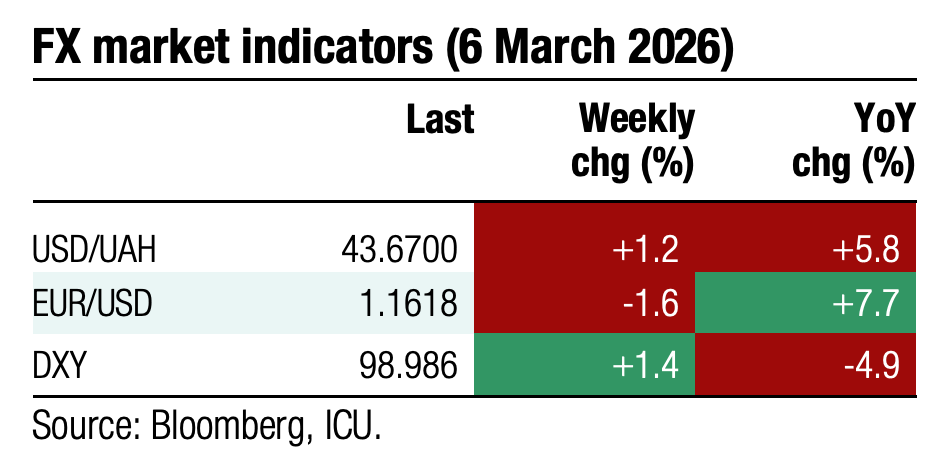

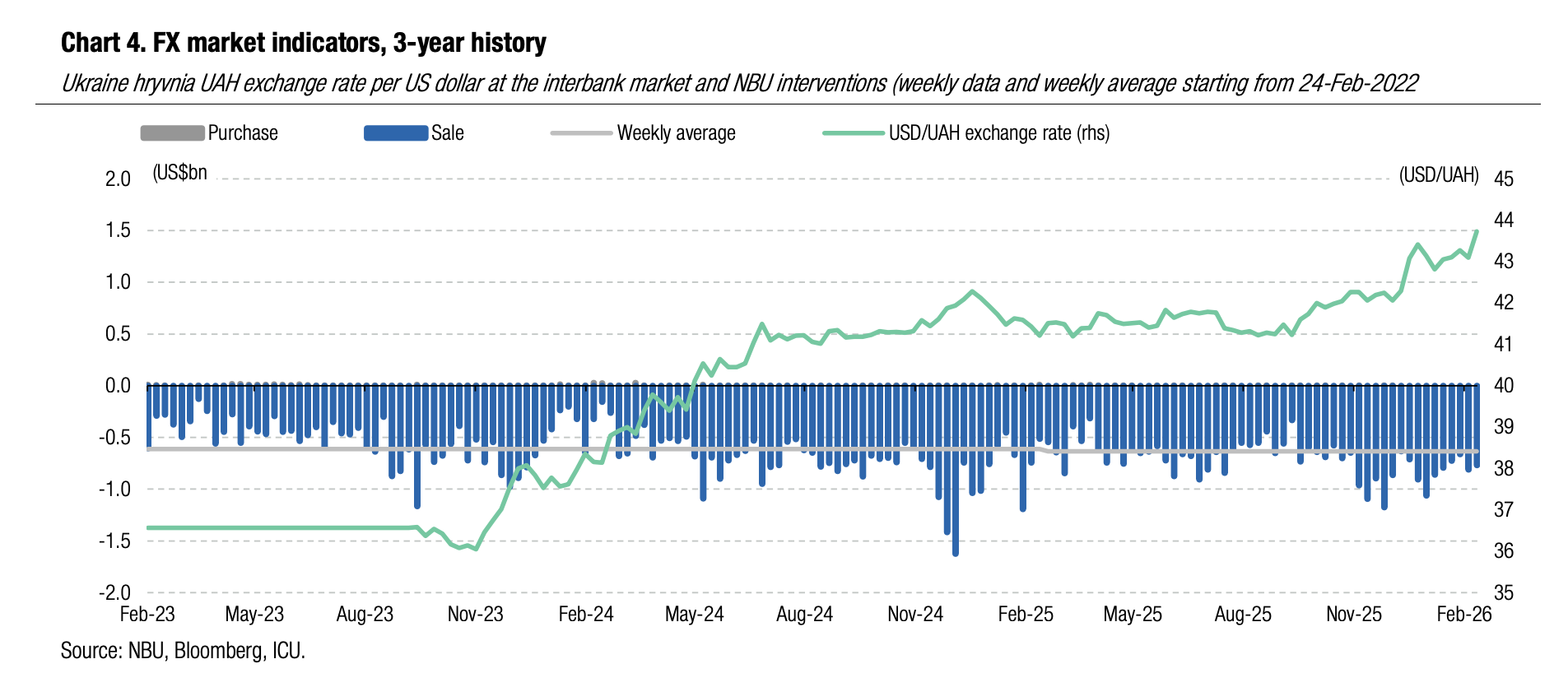

FX: NBU tests new lows for hryvnia

Last week, the NBU sharply weakened the hryvnia exchange rate to over UAH43.8/US$ despite a relatively low FX market deficit.

The shortage in the FX market increased by only 7% to US$579m over the four business days, while shifting towards the retail segment. Net foreign currency purchases in the interbank FX market fell by 28% to US$338m, while in the retail segment, they amounted to US$241m, which is a 13-month high.

The NBU interventions were also little changed WoW at US$770m, below average weekly volume YTD.

Against this backdrop, the hryvnia hit to UAH43.81/US$ last Thursday, the lowest level on record. Overall, the hryvnia weakened by 1.5% over the week to UAH43.73/US$, and by 3.3% YTD. In contrast, the hryvnia strengthened against the euro by 0.6% last week.

ICU view: The NBU’s decision to sharply weaken the hryvnia last week can hardly be explained purely by market factors, as neither the market deficit nor NBU interventions changed noticeably from the previous week. Therefore, the devaluation of the hryvnia should be interpreted as an NBU decision to take yet another step towards managed devaluation. To prevent strengthening depreciation expectations among local businesses and households, the NBU will likely seek to strengthen the hryvnia somewhat in the coming weeks. However, we expect the NBU will take another steps to weaken the hryvnia in the coming months so that the rate moves towards UAH45/US$ by end-2026.

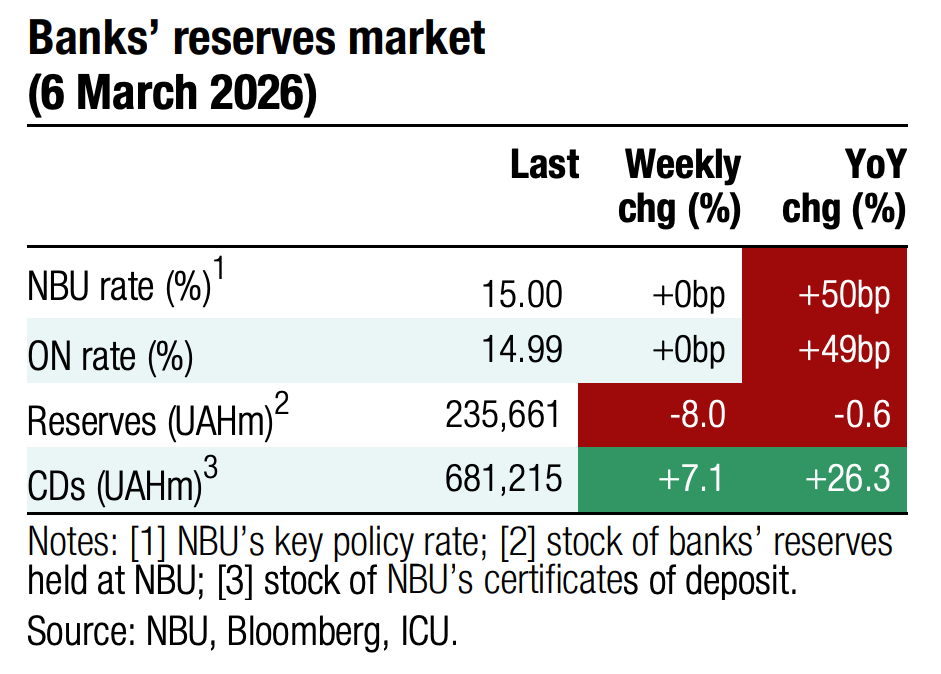

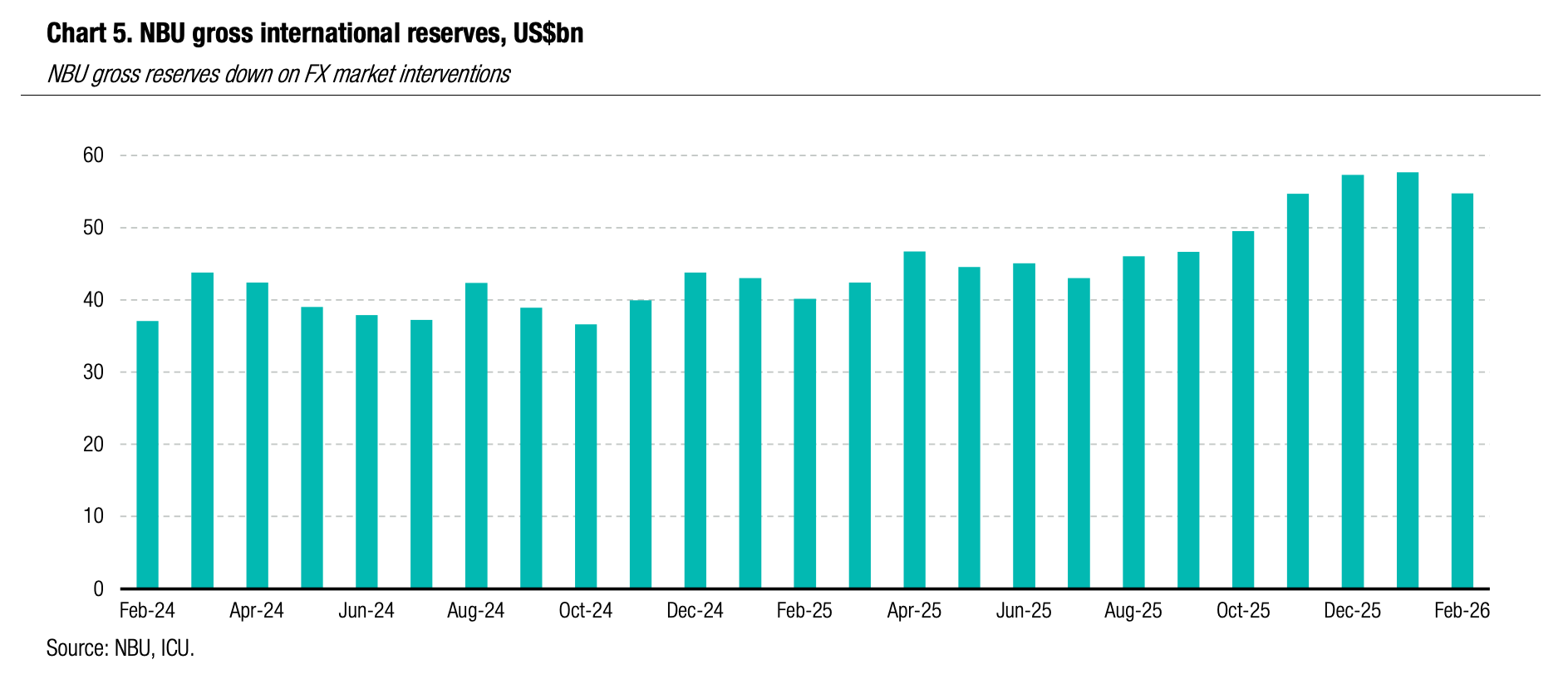

Economics: NBU reserves down 5% in February

The gross international reserves of the NBU decreased 5% in February to US$54.8bn, an equivalent of 5.7 months of future import as per NBU estimates.

NBU interventions in the FX market were the key drag even though the net sales were down by a fifth MoM to US$3.0bn. The repayments of external public debt, including to the IMF, erased another $0.6bn in reserves. Meanwhile, new inflows of foreign financial aid were relatively small at US$0.7bn.

ICU view: A significant monthly decline in reserves is related to the uneven schedule of foreign aid inflows. We expect NBU reserves will remain above US$50bn though 2026, as scheduled foreign aid should fully cover NBU needs for FX market sale interventions. While a likely delay in the Ukraine Support Loan from the EU due to Hungary’s resistance is a risk, such a delay will not weaken the NBU’s capacity to fully control the FX market and hryvnia exchange rate.