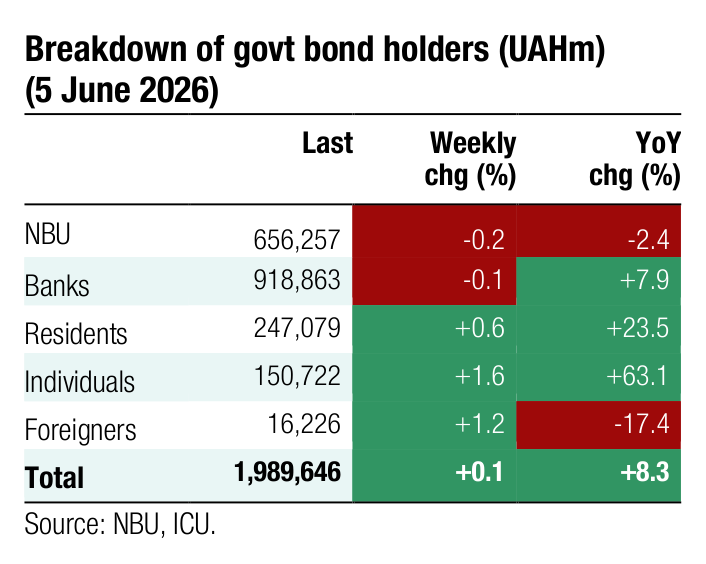

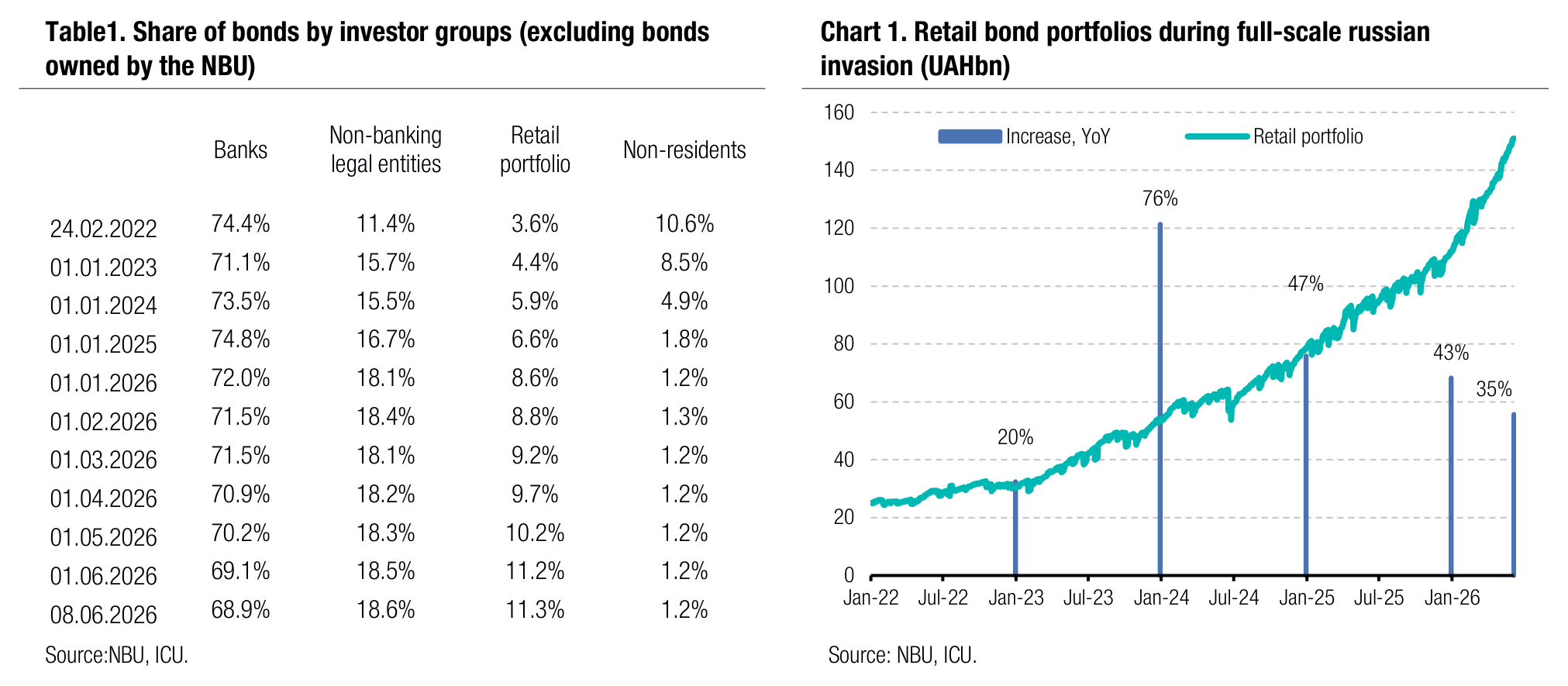

Ukrainian bond market

Retail portfolio of government debt tops UAH150bn

The population continues to increase their investments in domestic government bonds and their portfolios reached a new all-time high.

In May, the retail portfolio of government bonds grew by over 8%, and then increased further by 1.5% in the first week of June, topping a new record of UAH151bn (US$3.4bn). In total, retail investments in government bonds were up 35% YTD and sixfold since the beginning of the full-scale war.

In May, growth in retail holdings of government debt primarily came on the back of FX- denominated bonds as their size increased by almost 11% in hryvnia equivalent (the result was a mix of both new purchases and the FX revaluation effect). UAH-denominated bonds lagged with growth 6.7%. Yet, by early June, households’ focus was again back to UAH bonds. The share of UAH bonds in the total retail portfolio remained unchanged MoM at above 62%, which is +3pp YTD, but -1pp since the beginning of April.

Other groups of investors kept their portfolios broadly unchanged: banks’ holdings of debt were down by 2.6% in May and by 2.0% YTD. Non-bank legal entities kept their portfolios stable in May, and non-residents increased their investments by 2.8%. As a result, the share of the retail investors in the total volume of government bonds outstanding reached 11.3% (excluding government bonds owned by the NBU).

ICU view: FX-denominated government bonds that help hedge FX risks were in high demand among retail investors last month amid the gradual weakening of the hryvnia. However, their share in the total retail portfolio remained below 40%, as UAH bonds retain their strong appeal among households due to high interest rates and the absence of taxation of coupon payments.

Table1. Share of bonds by investor groups (excluding bonds owned by the NBU)

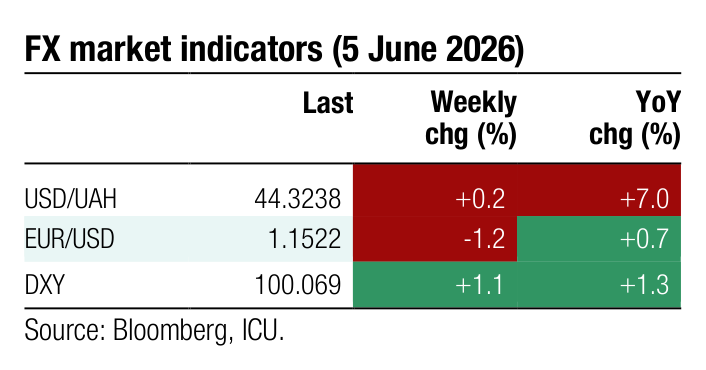

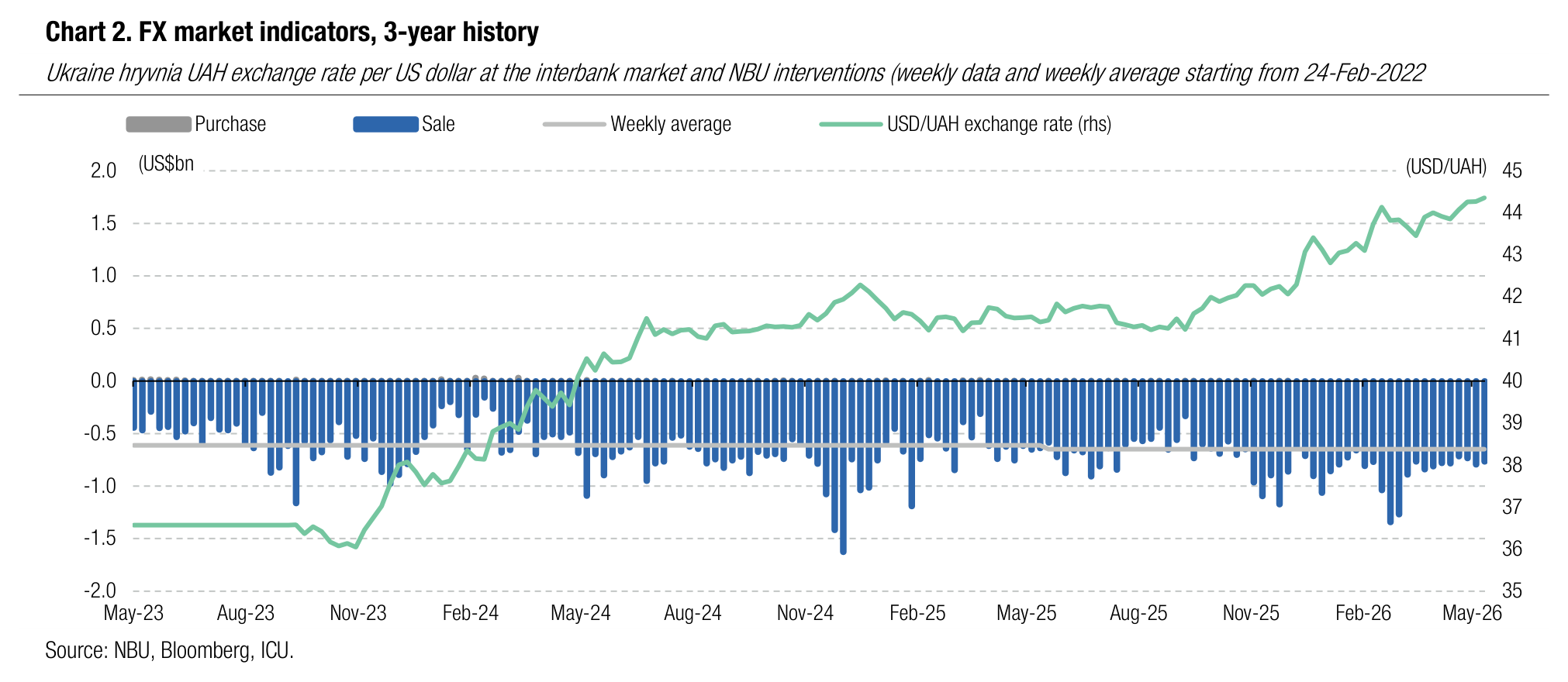

Foreign exchange market

NBU continues to weaken hryvnia slowly

In the first week of June, the National Bank continued to gradually weaken the hryvnia.

Last week, the NBU continued to weaken the hryvnia in small steps, taking the rate to UAH44.38/US$ on Thursday and ended the week by setting the official hryvnia exchange rate at UAH44.36/US$. The hryvnia weakened by 0.2% during the week and by 4.7% YTD.

NBU interventions totalled US$766m last week, roughly stable over the previous five weeks. Nonetheless, the FX market deficit was up 20% WoW to US$552m (in four business days).

ICU view: The NBU continues to weaken the hryvnia slowly as it continues to drift to new all-time highs from week to week. Yet, we expect the pace will remain gradual and the rate will reach UAH45.8/US$ towards the end of the year.

Economics

Macro risks up; more foreign financial aid unlocked

The Ukrainian economy showed unparalleled resilience to massive electricity blackouts at the start of the year, but its growth potential for the coming years remains constrained. Key points of our new macro review , published last Wednesday, are given below.

Private household demand, once again, proved to be a solid growth pillar complemented with government investments into military projects. Yet, their strength is likely to fade, and we expect GDP growth will be at just below 1% in 2026.

The Middle East crisis took center stage on the global arena since March and had a quick impact on consumer prices via primary and secondary effects. The firm disinflationary trend sharply reversed, and we now expect CPI in the range of 9-10% at the end of the year. This is significant deterioration compared with our previous forecast of below 7%. We think the current NBU monetary policy stance is tight enough to counter a temporary increase in inflationary pressures and the chances of a key policy rate increase in 2026 are still below 50%.

The Ministry of Finance continues to reap the benefits of lower cost of domestic borrowings after it aggressively cut rates before the outbreak of the Iran war. The story of external accounts remains unchanged – we continue to see the ample current account deficit as a significant mid-term risk but that is fully manageable in 2026 and 2027 thanks to sufficient external funding. The approval of the Ukraine Support Loan by the EU came as a huge relief, as if fully enables the MinFin to cover the fiscal deficit and the NBU to maintain its reserves at a safe level of US$55-60bn. We have little doubt the authorities will do their best to take the reform actions envisaged by the IMF program and the EU loan conditionalities.

A substantial increase in FX market deficit YTD is very worrisome, and it makes the NBU much more inclined to switch to a somewhat faster pace of hryvnia depreciation. In light of this, we revise our end-2026 exchange rate forecast to UAH45.8/US$.

The 2026 fiscal gap is now fully covered with external funding, and the MinFin is likely to reduce the stock of domestic debt for the first time since the start of the full-scale invasion. Like in previous reports, we assume no major change in the safety risks in the mid-term – no peace deal and no major territory gains by the enemy.

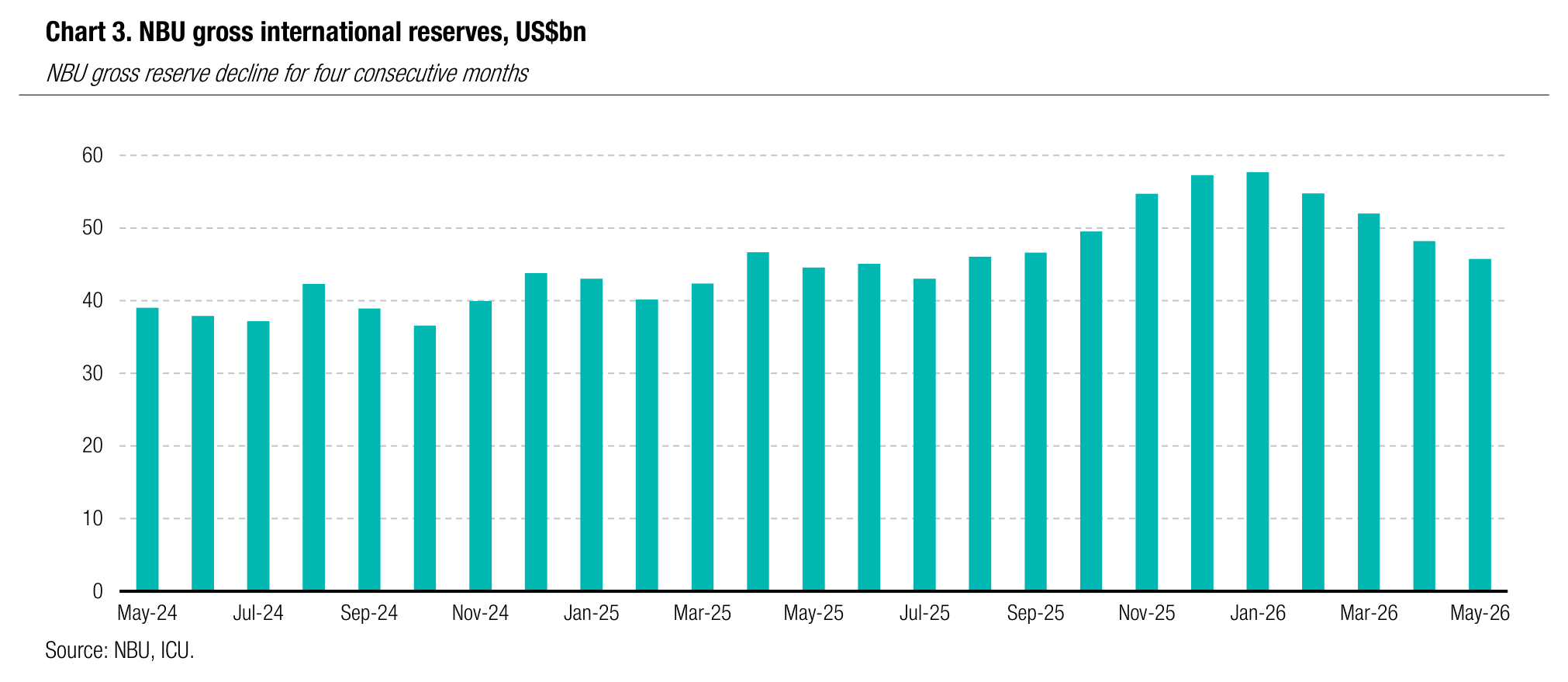

NBU reserves decline further in May

Gross international reserves of the NBU declined 5.1% in May and 20.2% YTD to US$45.7bn. The reserves stood at a 4.7-month equivalent of future imports according to the NBU estimates.

The decline in reserves continues as the inflows of foreign financial aid remain subdued. In May, Ukraine received just US$0.5bn in loans from the WB and no financing from other partners. Meanwhile, the NBU FX sales interventions were significant at US$3.1bn and another US$0.4bn was spent on servicing of FX debt. The net FX revaluation effect of reserves was positive at US$0.44bn.

ICU view: NBU reserves keep declining, but the recently approved USL loan from the EU is a silver lining. The inflows of foreign financial aid should resume in June, and we expect NBU reserves will return to above US$50bn during the summer. We expect reserves will then stay in the range of US$50-60bn at least until mid-2027, enabling the NBU to keep the FX market and hryvnia exchange rate under its full control.