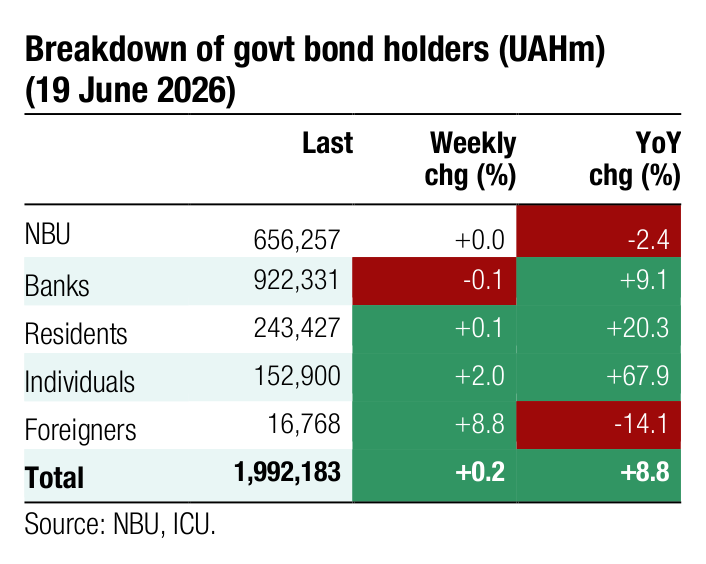

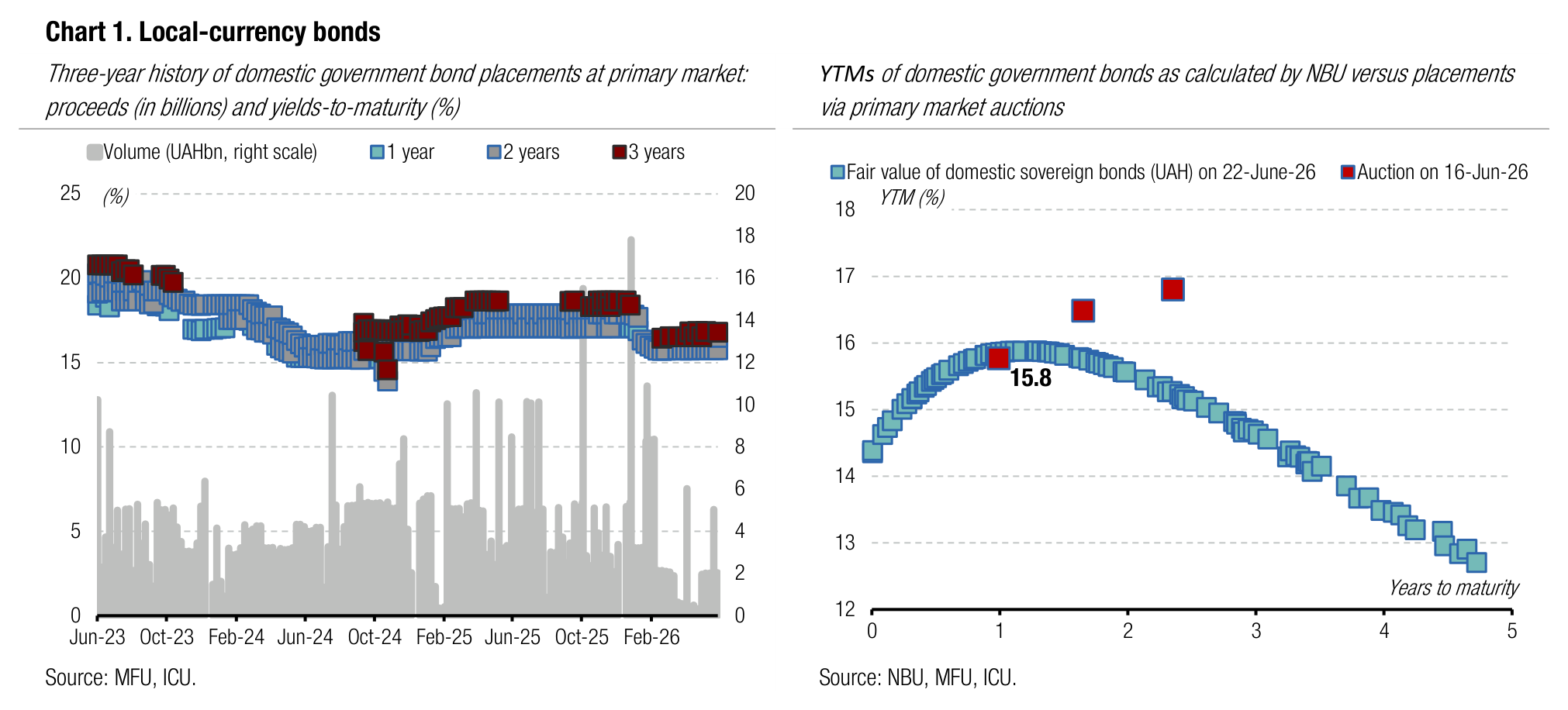

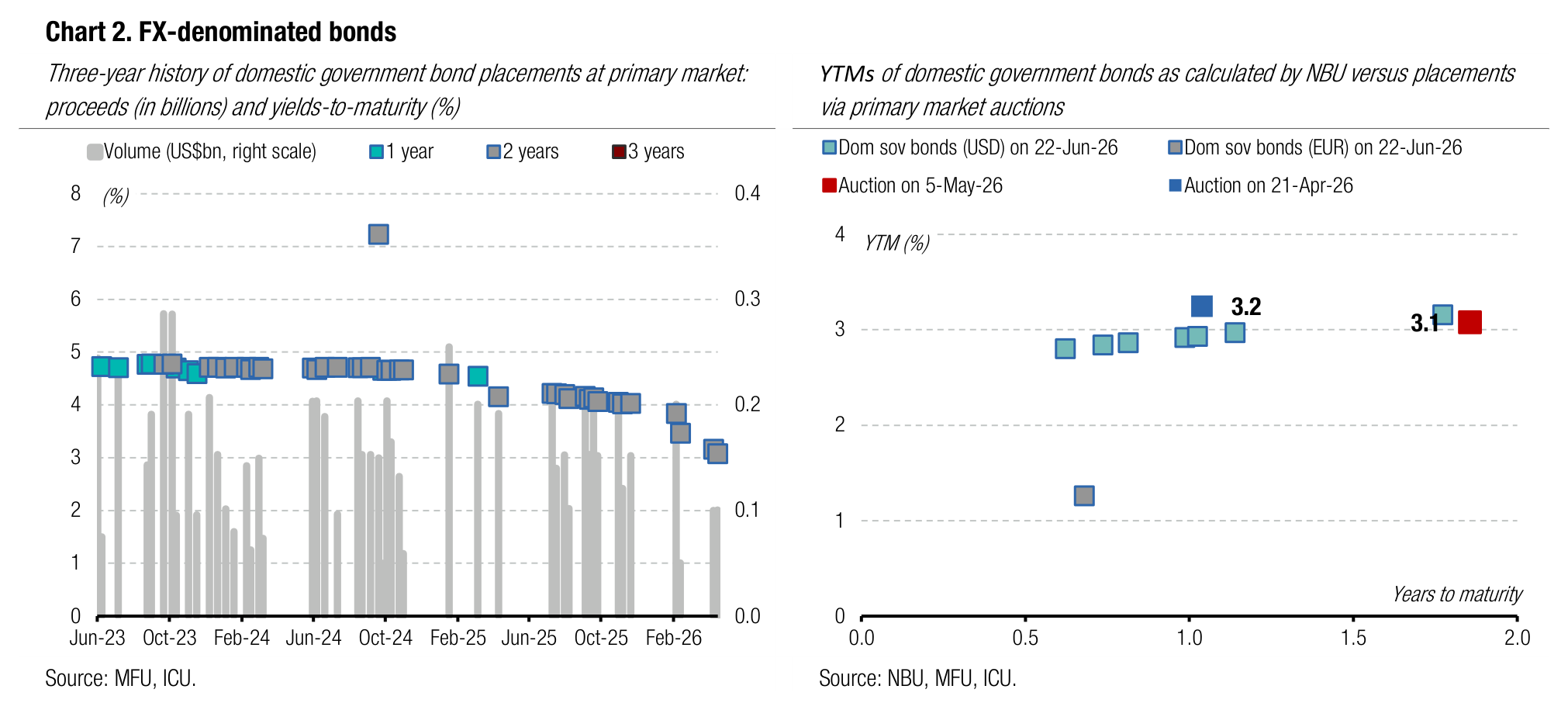

Ukrainian bond market

Interest in short-term bonds up

The secondary bond market is currently dominated by trading in bonds with the remaining maturities of up to one year, although some longer bonds enjoy strong interest as well.

Last week, investor interest in bonds with maturities below one year increased significantly and they made up 52% of the total secondary bond market turnover. This is up 15 pp from the previous week and more than up 2x vs the first week of June. UAH bills due in the next six months contributed 35% to total trading. The paper due March 2027 enjoyed the largest number of deals—6,183 for UAH2.5bn—13% of the total turnover.

ICU view: Last week, bond market participants were awaiting the NBU's decision on the key policy rate; some of them assumed a rate hike. Therefore, short-term instruments were the key investor focus. As the NBU left the key rate unchanged (see comment below ), at least until July, there will be no pressure on UAH bond yields in the near term, and they should remain at current levels.

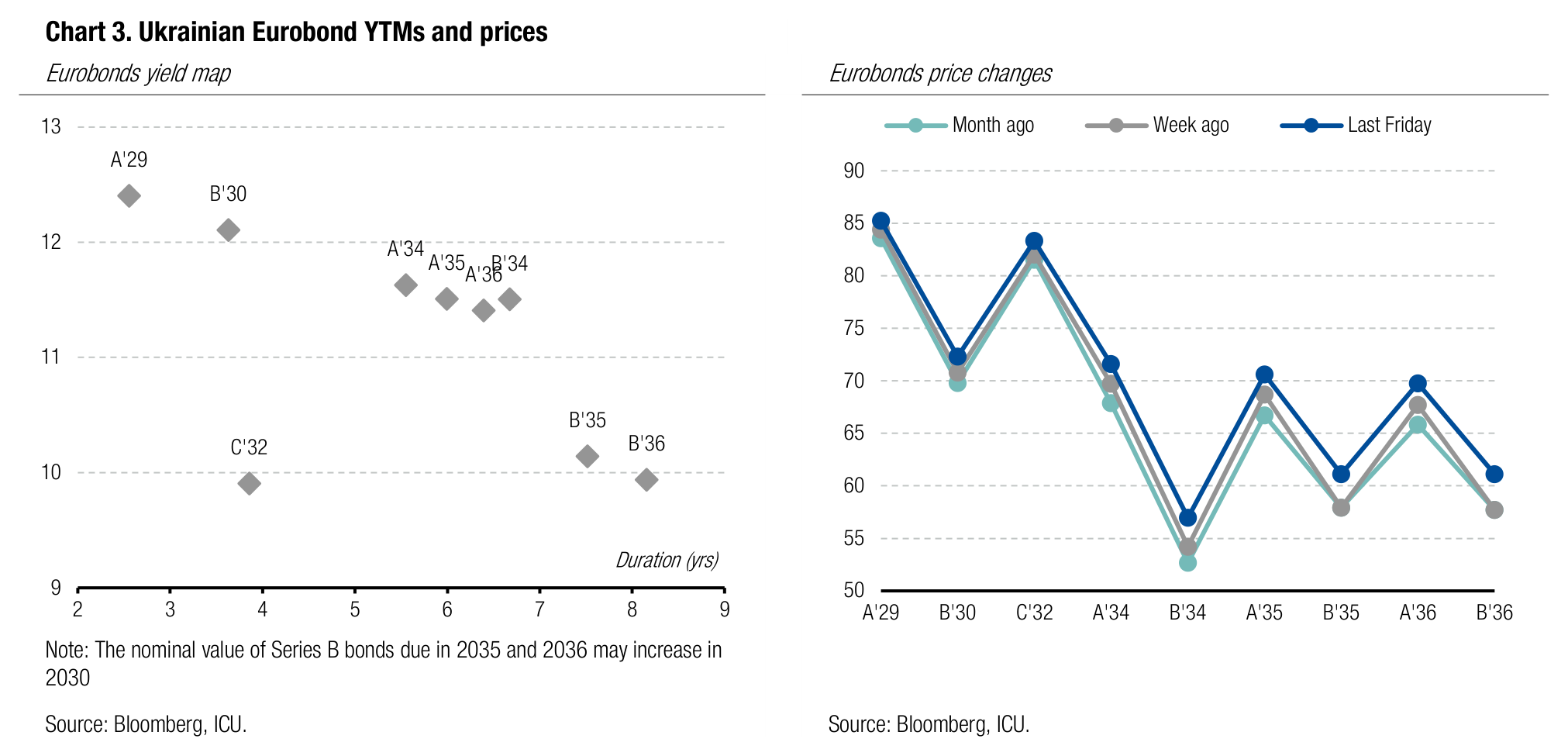

Eurobond rally unabated

Ukrainian Eurobonds continued their rally last week against the backdrop of positive war and economy-related news.

Last Monday, Eurobond prices rose in response to the first staff-level review of the IMF EFF program. Subsequently, they remained broadly stable, but with a slight uptick on the back of a series of positive news and events, including Ukraine-related messages at the G7 summit, the meeting of the Contact Group on Ukraine's defence, the meeting of the European Council, and bilateral meetings.

Overall, in less than a week (a short one due to a day off in the US on Friday), Eurobond prices rose by an average of 3%, while the EMBI index was only up 0.4%. Most Ukrainian Eurobonds reached new highs last week, with the only exception being Series B bonds maturing in 2035-36.

ICU view: The past week was full of positive news about the continuation of financial and military support for Ukraine. Investors maintained positive sentiment that was reinforced by the staff-level agreement on the IMF program review.

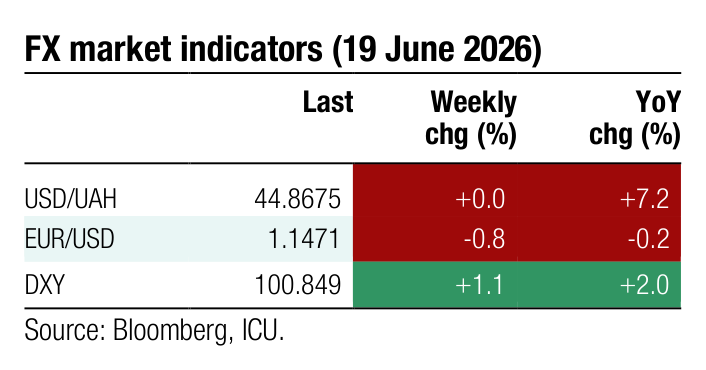

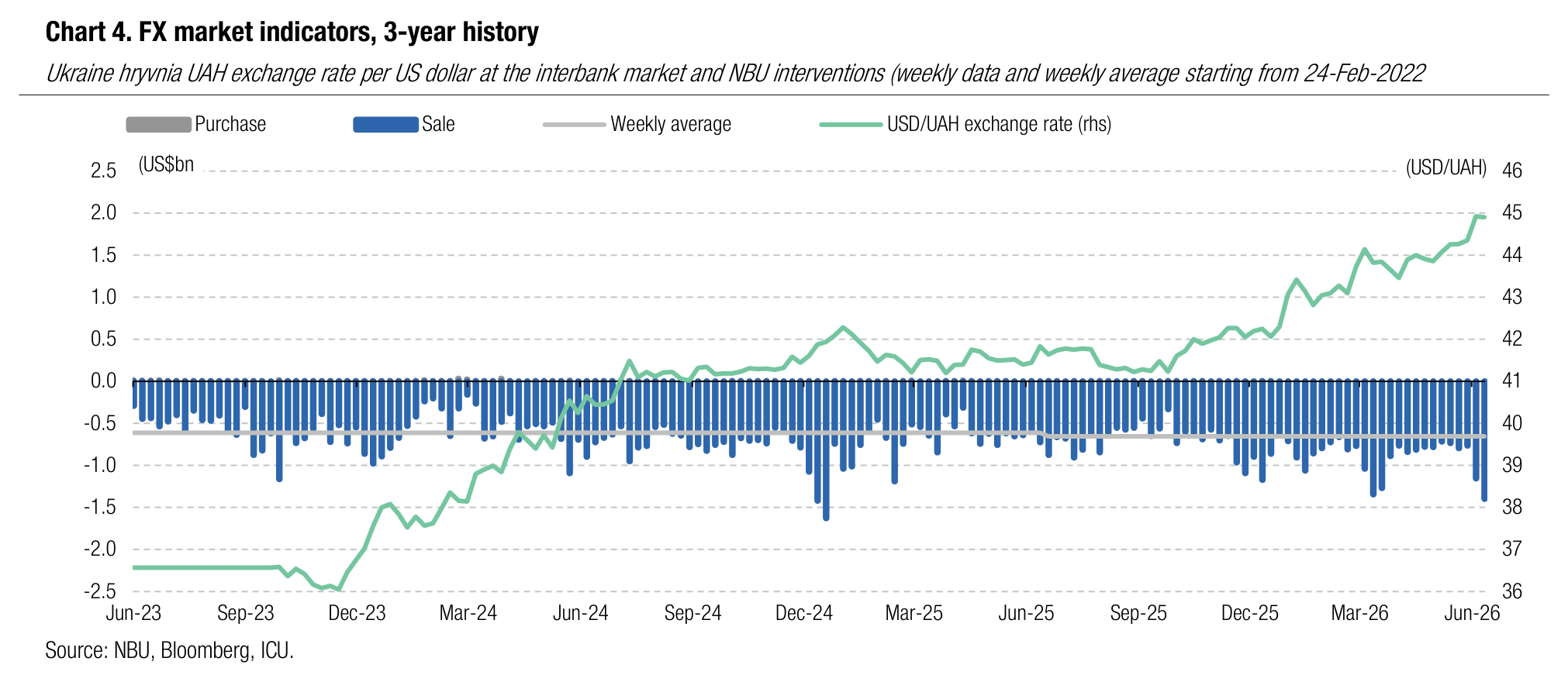

Foreign exchange market

NBU stabilises hryvnia

After a sharp devaluation of the hryvnia in the first half of June, the NBU did its best last week to stabilise the exchange rate and prevent new lows.

Last week, the NBU's interventions reached almost US$1.4bn, one of the largest historical weekly volumes. In the past, last week’s interventions size was exceeded only three times: at the end of May 2022 (over US$1.4bn), and in the last two weeks of 2024 (over US$1.4bn and US$1.6bn). The outsized interventions stabilised the hryvnia near 44.9 UAH/$.

The FX deficit increased by 27% WoW in the FX market, and that was driven by both a decrease in foreign currency supply and an increase in demand.

ICU view: Negative FX market expectations continued to build last week. The NBU noted that the imbalances resulted primarily from a seasonal decline in hard currency supply. Yet, we believe the key driver of wider imbalances was the NBU’s stance with regard to FX policies. The market did not expect a significant hryvnia depreciation, and many exporters simply decided to put their sell instructions on hold. In response, the NBU was forced to significantly increase interventions to ease depreciation expectations and encourage more supply in the coming weeks. We expect the central bank will keep the US dollar rate below UAH45/US$ in the coming weeks, and we maintain our year-end exchange rate forecast at UAH45.8/US$.

Economics

NBU holds rate, signals hike risk

The key rate remains at 15%, while NBU rhetoric now points to a higher risk of monetary tightening.

The decision was in line with our previous forecast. The NBU Board kept the key policy rate at 15%, saying current monetary conditions remain sufficiently tight, demand for hryvnia savings instruments is strong, and near-term risks related to external financing and energy prices have eased. Headline inflation slowed to 8.2% YoY in May, while core inflation edged up to 7.9% YoY. Both indicators were above the NBU’s April forecast path, mainly due to stronger second-round effects from higher energy prices.

ICU view: The recent change in the NBU’s rhetoric suggests an increasing possibility of a rate hike this year. The 30 July rate review is a likely date for such a decision if the new forecast confirms stronger underlying inflation pressure, higher fiscal risks, or more persistent FX market imbalance. We currently see a prolonged period of the key rate unchanged at 15% as the base-case scenario, but assign a 40% probability to a rate hike in 2026.