Ukrainian bond market

MoF exchanges reserve bonds

Last week, the Ministry of Finance successfully exchanged reserve bonds due in July; remaining redemptions during the month are insignificant.

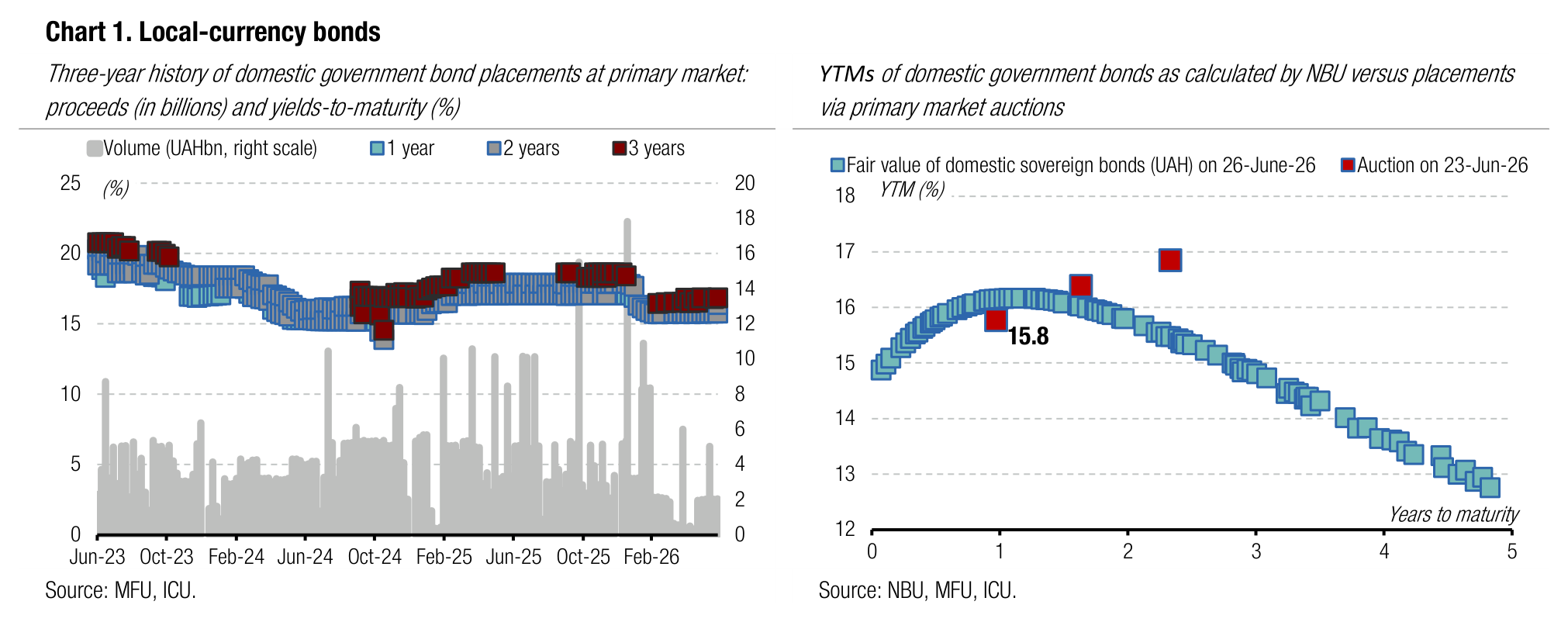

The MoF held an exchange auction last Wednesday and offered banks the opportunity to exchange reserve bonds maturing on July 22 for a new paper due November 2029. The offer was capped at UAH17bn, and banks submitted 29 bids for just above UAH17.4bn. The yields increased slightly vs. the auction on June 9 when this paper was first offered. The MoF agreed to raise the cut-off rate by 10bp to 13%, and the weighted average yield rose by 11bp to 12.95%.

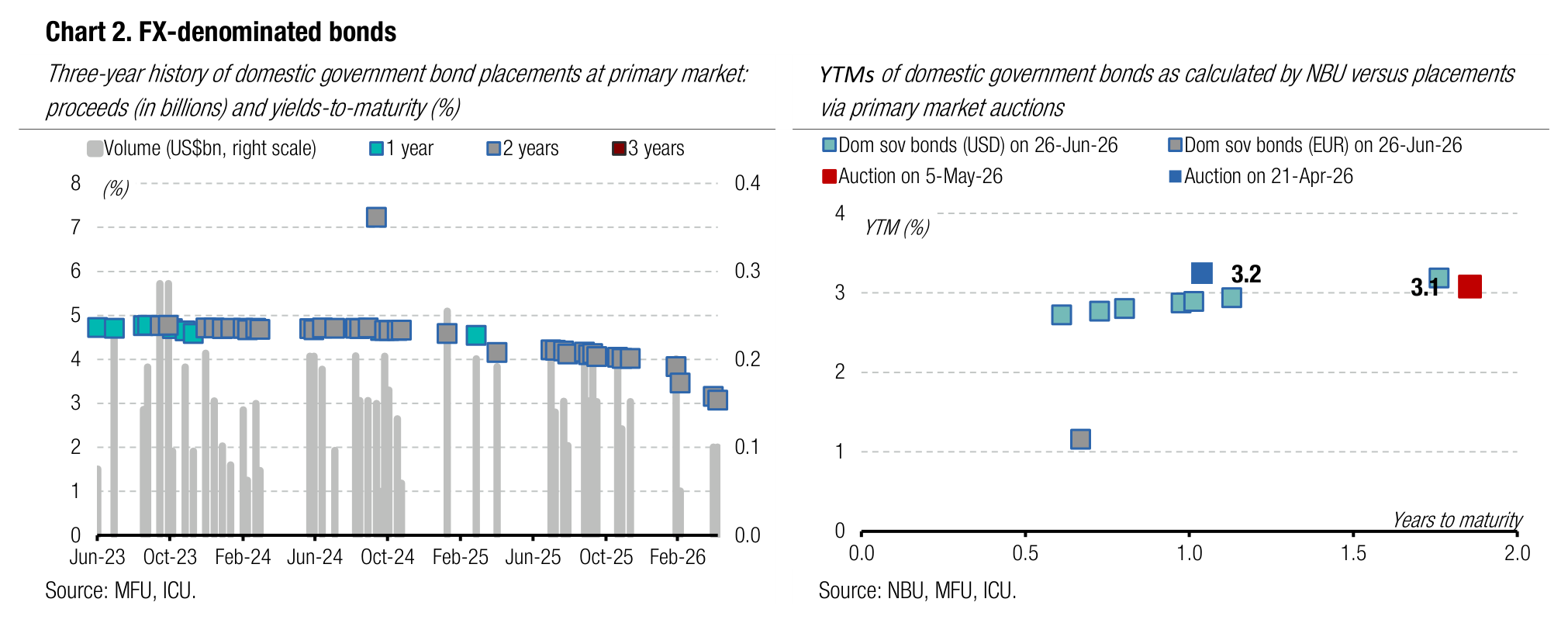

The ministry exchanged the vast majority of reserve bond maturing on July 22. The remaining amount outstanding of nearly UAH3bn is the only MoF UAH-denominated debt due in July. The MoF will face no pressure to borrow in UAH next month. Instead, the MoF will focus on redeeming EUR369m of FX-denominated bonds, and thus will offer EUR200mn worth of EUR bonds tomorrow.

ICU view: With last week's exchange, the MoF can use July borrowings in UAH for budget needs rather than for redemptions. We also expect a new reserve UAH bond offering in July to exchange the securities due in August.

Foreign exchange market

NBU continues to struggle with hard currency shortage

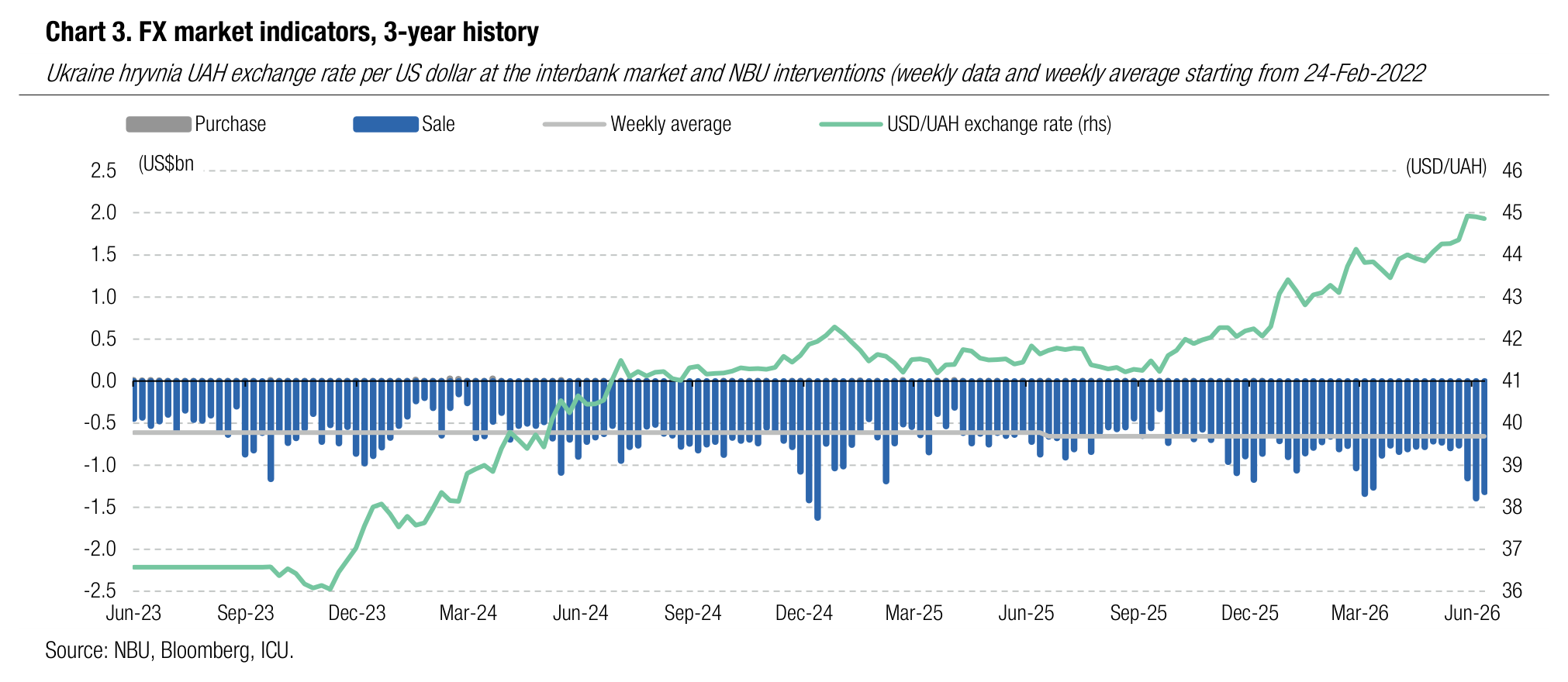

Last week, the National Bank again had to sell a large amount of foreign currency, as the FX market deficit remained very large.

The FX shortage in FX market remained little changed vs the previous week, at over US$0.9bn. Demand and supply from legal entities in the interbank FX market decreased slightly keeping the deficit little changed. Net purchases of hard currency in the retail segment also remained high. All in all, the National Bank sold more than US$1.3bn last week, just 5% below the previous week's interventions.

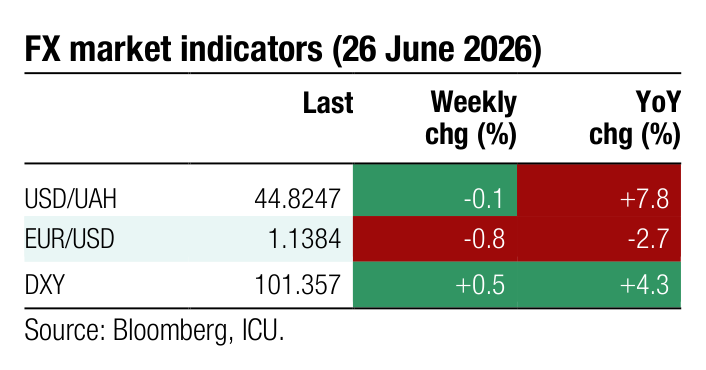

With hefty interventions the NBU was able to keep the hryvnia exchange rate below UAH45/US$ and, by the end of the week, even slightly strengthen it to UAH44.86/US$. Thus, the hryvnia weakened against the US dollar by 1.3% in June and 5.9% YTD.

ICU view: Last week, negative expectations persisted in the FX market, and sellers continued to delay the sale of the hard currency. The NBU keeps interventions at an elevated level to protect the hryvnia and lessen devaluation expectations. The NBU clearly shows its intention to keep the US dollar price below UAH45/US$ for some time and even strengthen it occasionally. In general, the NBU may allow increasing exchange rate movements in both directions, as noted in communications at the briefing on the key policy rate.