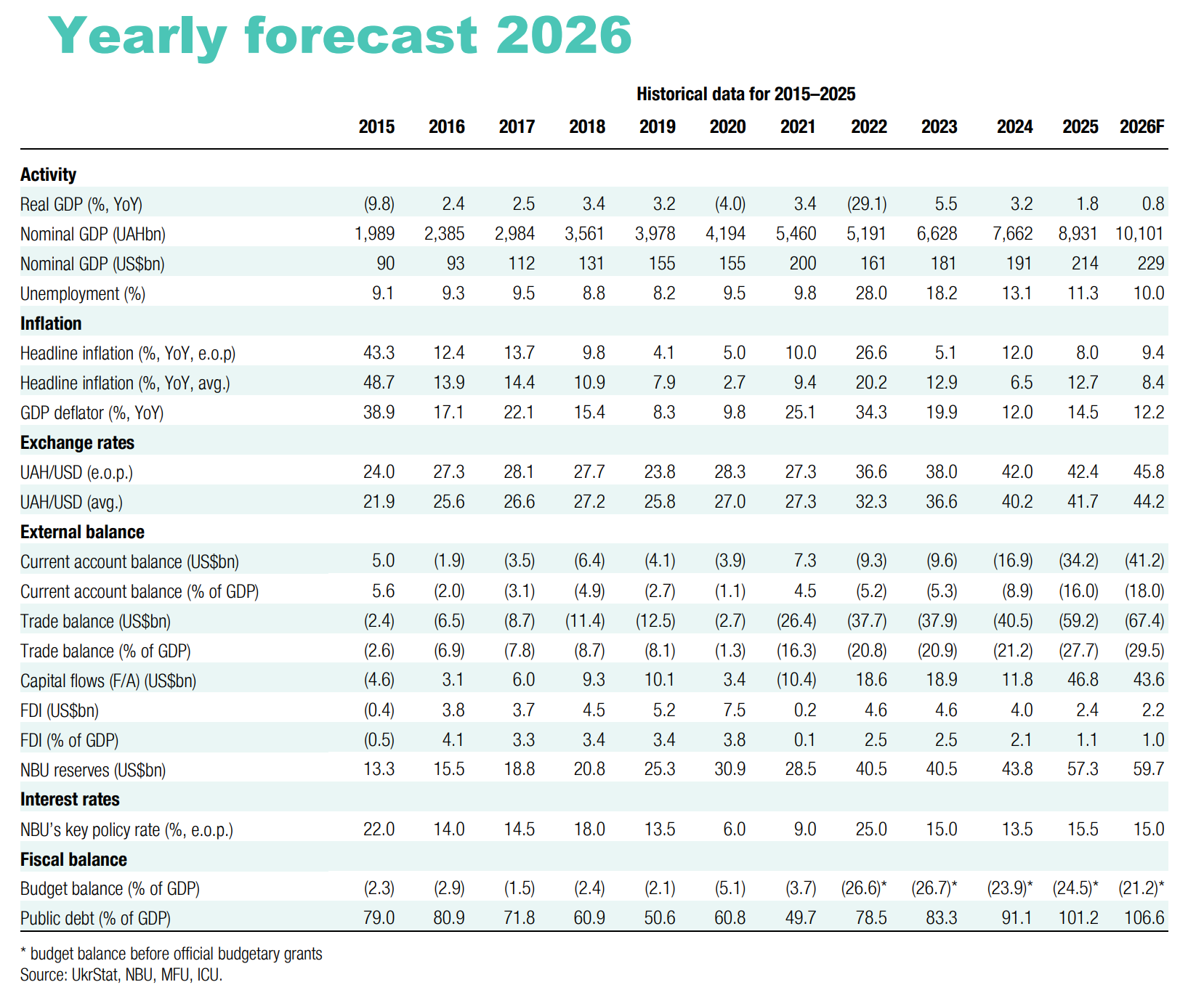

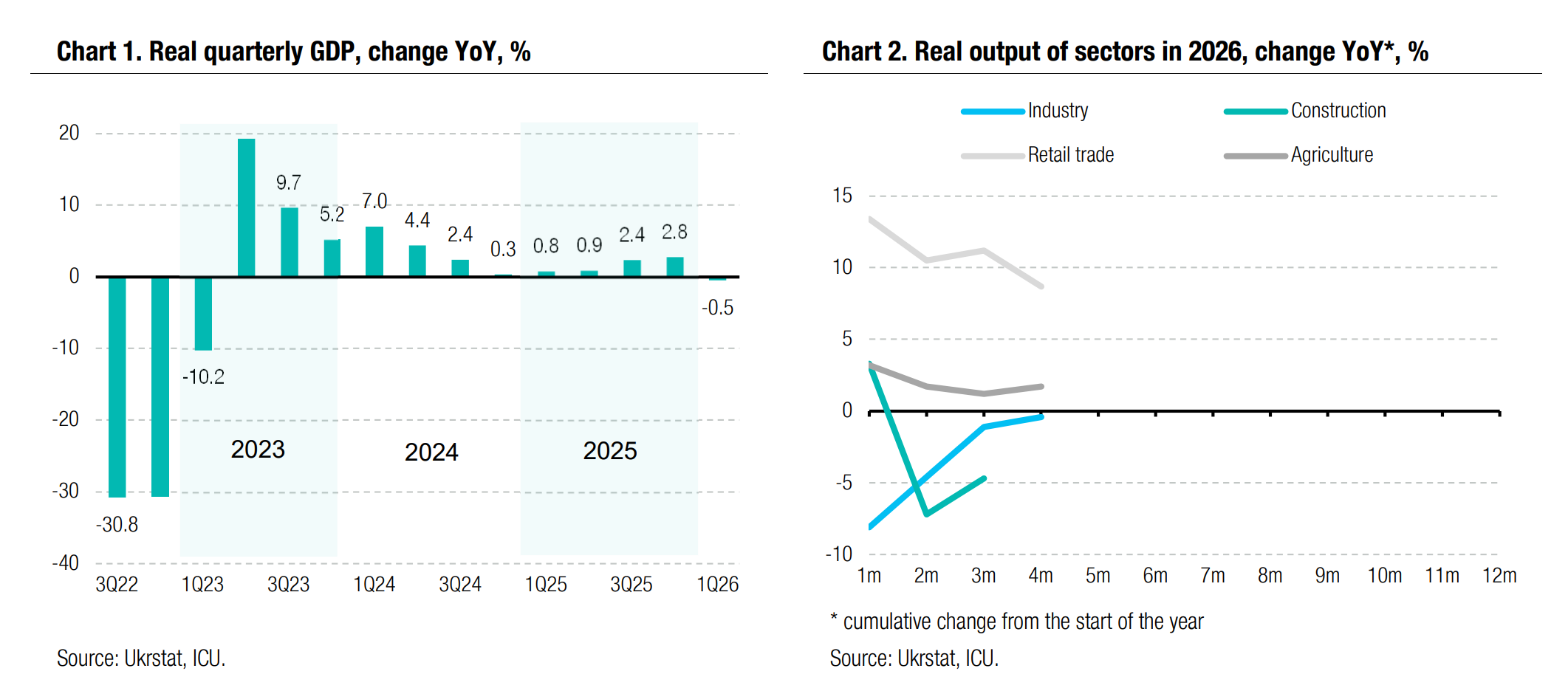

The Ukrainian economy showed unparalleled resilience to massive electricity blackouts at the start of the year, but its growth potential for the coming years remains constrained. Private household demand, once again, proved to be a solid growth pillar complemented with government investments into military projects. Yet, their strength is likely to fade, and we expect GDP growth will be at just below 1% in 2026.

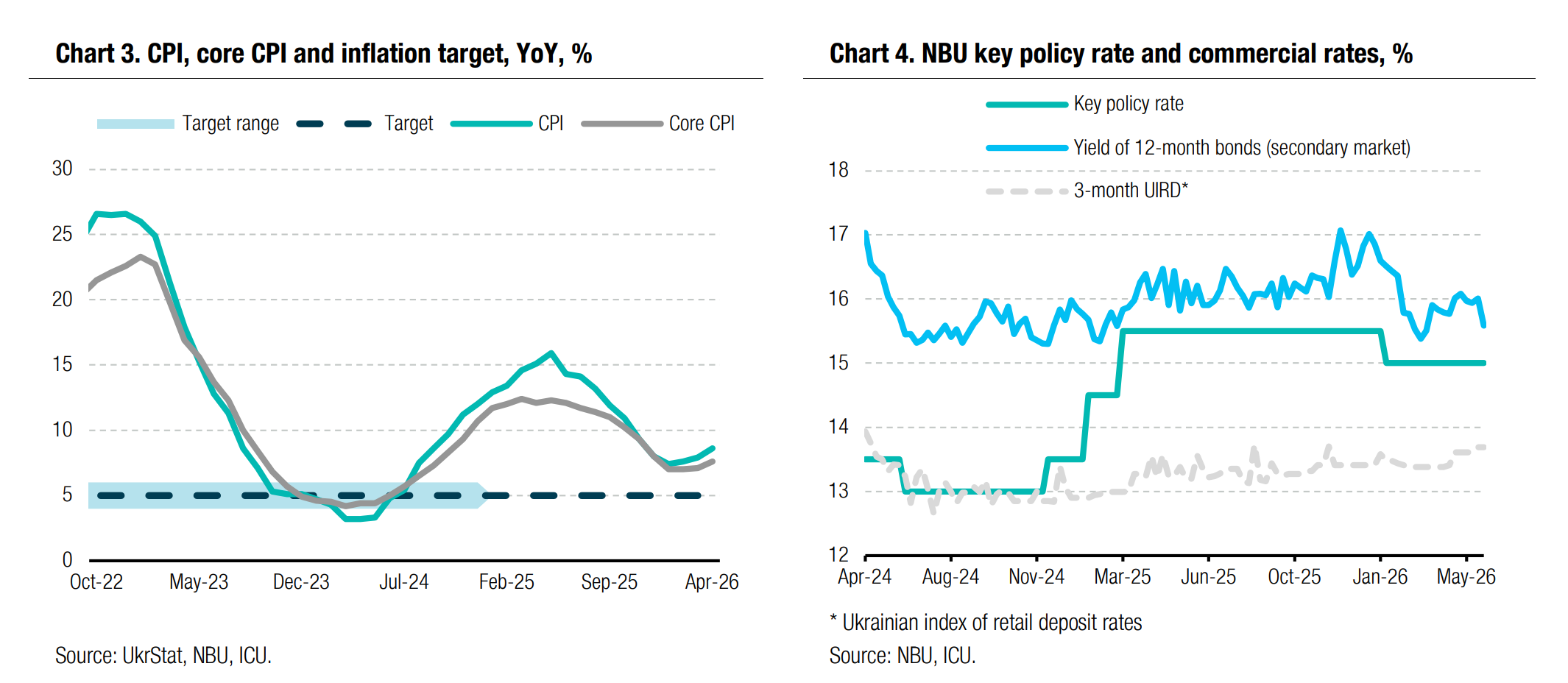

The Middle East crisis took center stage on the global arena since March and had a quick impact on consumer prices via primary and secondary effects. The firm disinflationary trend sharply reversed, and we now expect CPI in the range of 9-10% at the end of the year. This is significant deterioration compared with our previous forecast of below 7%. We think the current NBU monetary policy stance is tight enough to counter a temporary increase in inflationary pressures and the chances of a key policy rate increase in 2026 are still below 50%.

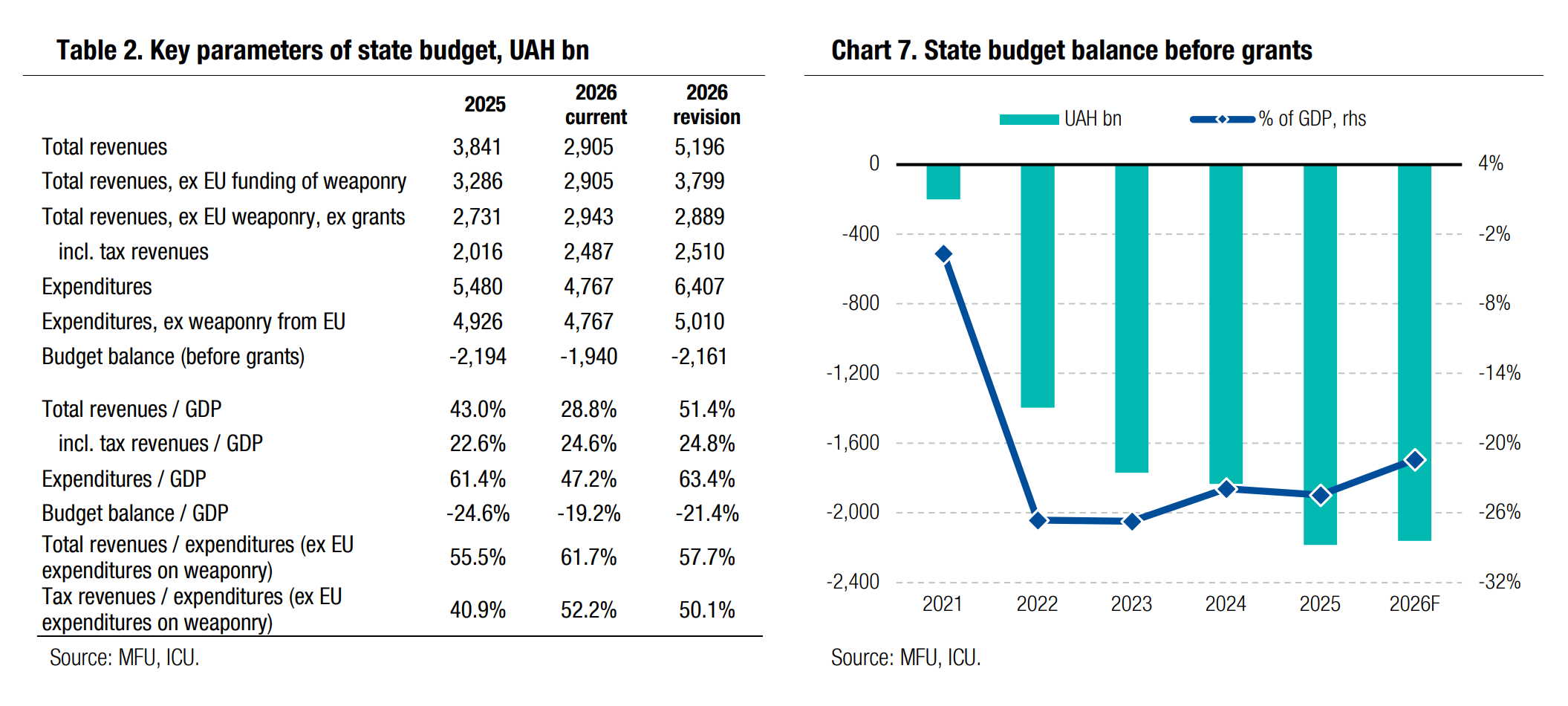

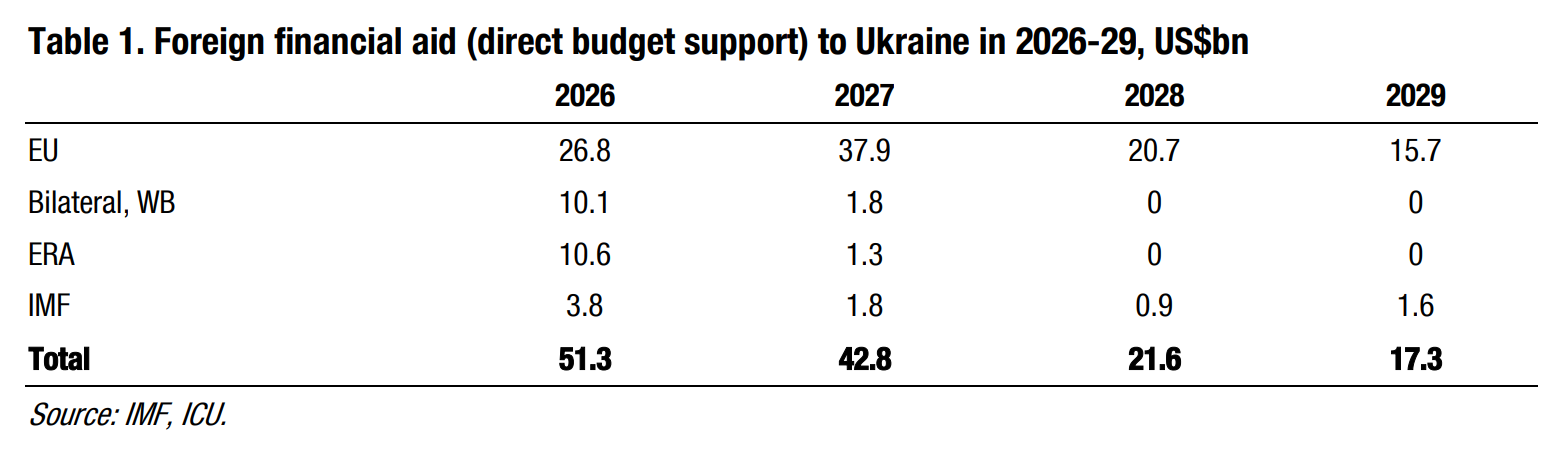

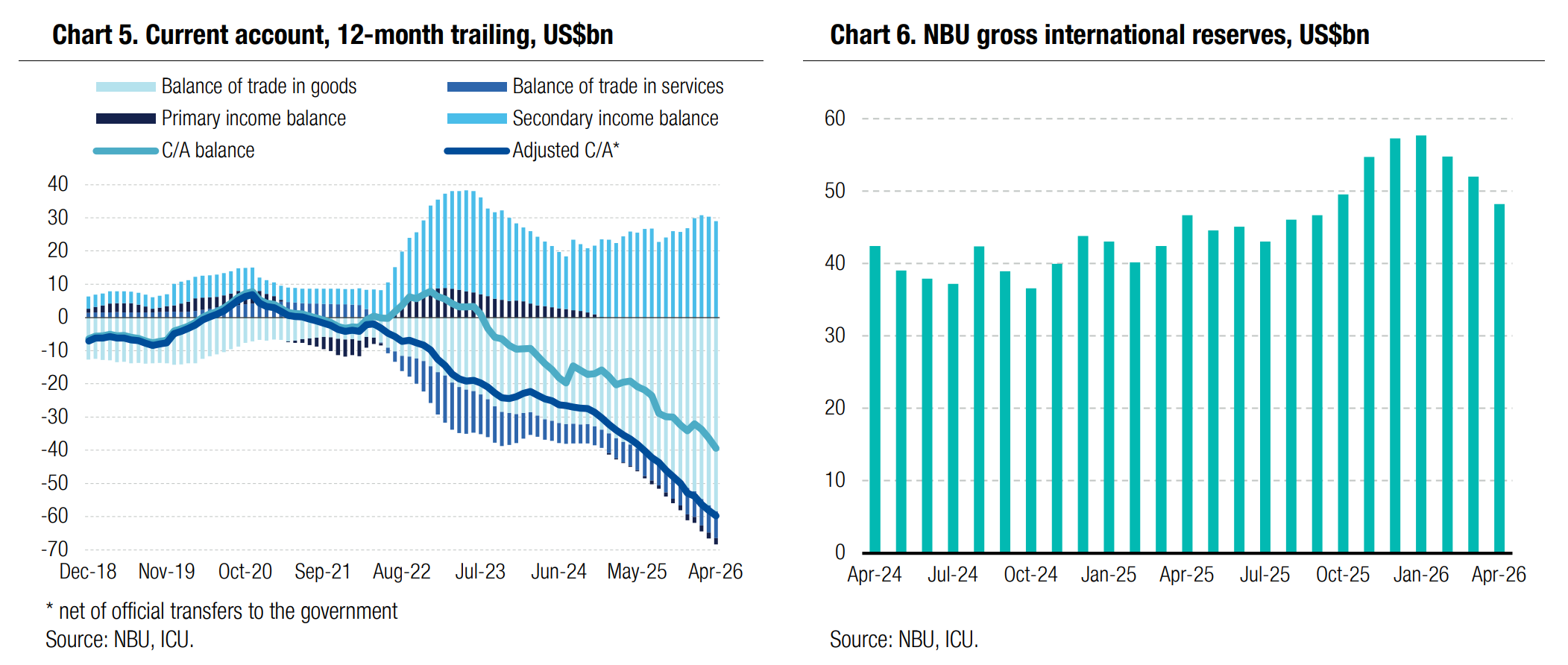

The Ministry of Finance continues to reap the benefits of lower cost of domestic borrowings after it aggressively cut rates before the outbreak of the Iran war. The story of external accounts remains unchanged – we continue to see the ample current account deficit as a significant mid-term risk but that is fully manageable in 2026 and 2027 thanks to sufficient external funding. The approval of the Ukraine Support Loan by the EU came as a huge relief, as if fully enables the MinFin to cover the fiscal deficit and the NBU to maintain its reserves at a safe level of US$55-60bn. We have little doubt the authorities will do their best to take the reform actions envisaged by the IMF program and the EU loan conditionalities.

A substantial increase in FX market deficit YTD is very worrisome, and it makes the NBU much more inclined to switch to a somewhat faster pace of hryvnia depreciation. In light of this, we revise our end-2026 exchange rate forecast to UAH45.8/US$.

The 2026 fiscal gap is now fully covered with external funding, and the MinFin is likely to reduce the stock of domestic debt for the first time since the start of the full-scale invasion. Like in previous reports, we assume no major change in the safety risks in the mid-term – no peace deal and no major territory gains by the enemy.