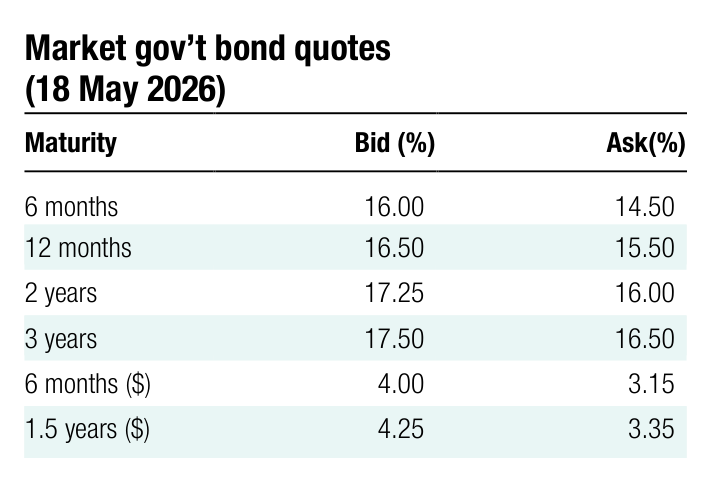

Ukrainian bond market

Investment strategies diverge in bond market

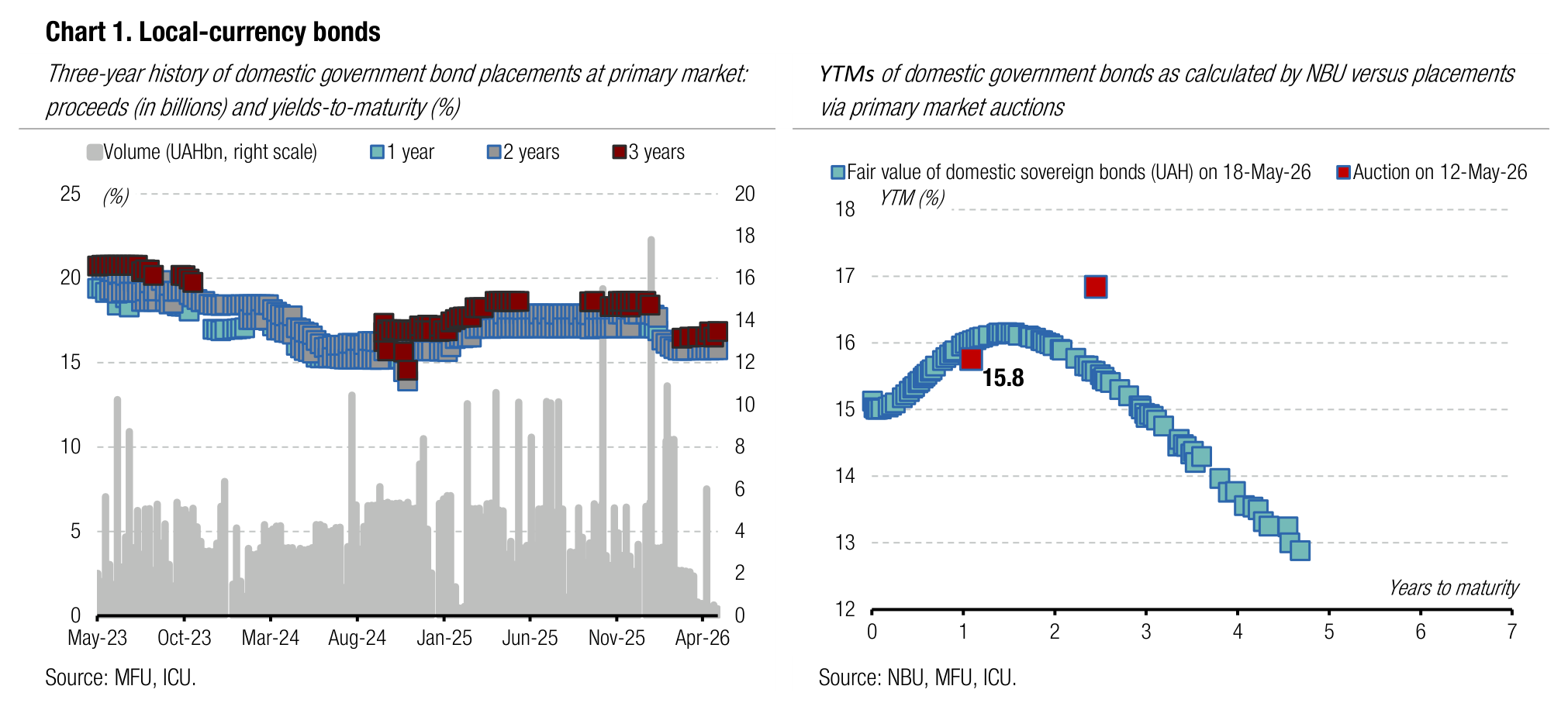

Over the last few weeks, interest in bonds with a maturity below 12 months declined and shifted to shorter-maturity bonds.

Last week, trading in UAH bonds was nearly evenly split between bonds with maturities below and above 12 months. This contrasts with earlier weeks YTD and months when the share of bonds due in over one year averaged 62%, reaching 77% in certain weeks.

The share of securities with maturities below six months was 25% and that of bonds maturing in 6-12 months at 27%, well above 20% in March and April. The share of three-year notes was up to 26% from below 20% in April. The share of two-year bonds decreased last week to 16% from 40-63% in early April.

ICU view: The most recent NBU macro forecast assumes the key policy rate will remain unchanged over the next 12 months, but build-up in inflation risks could prompt the NBU to raise it. Therefore, difference in investor expectations led to diverging approaches to investment. Some investors expect rates to rise, so they invest in securities with the shortest maturity available so they can later reinvest proceeds in longer bonds at higher rates. Yet, some investors continue to seek to lock in current yields for a longer period, expecting a short-lived key rate increase, with insignificant or no reaction from the MoF to NBU's decision.

Ceasefire episode boosts investor optimism

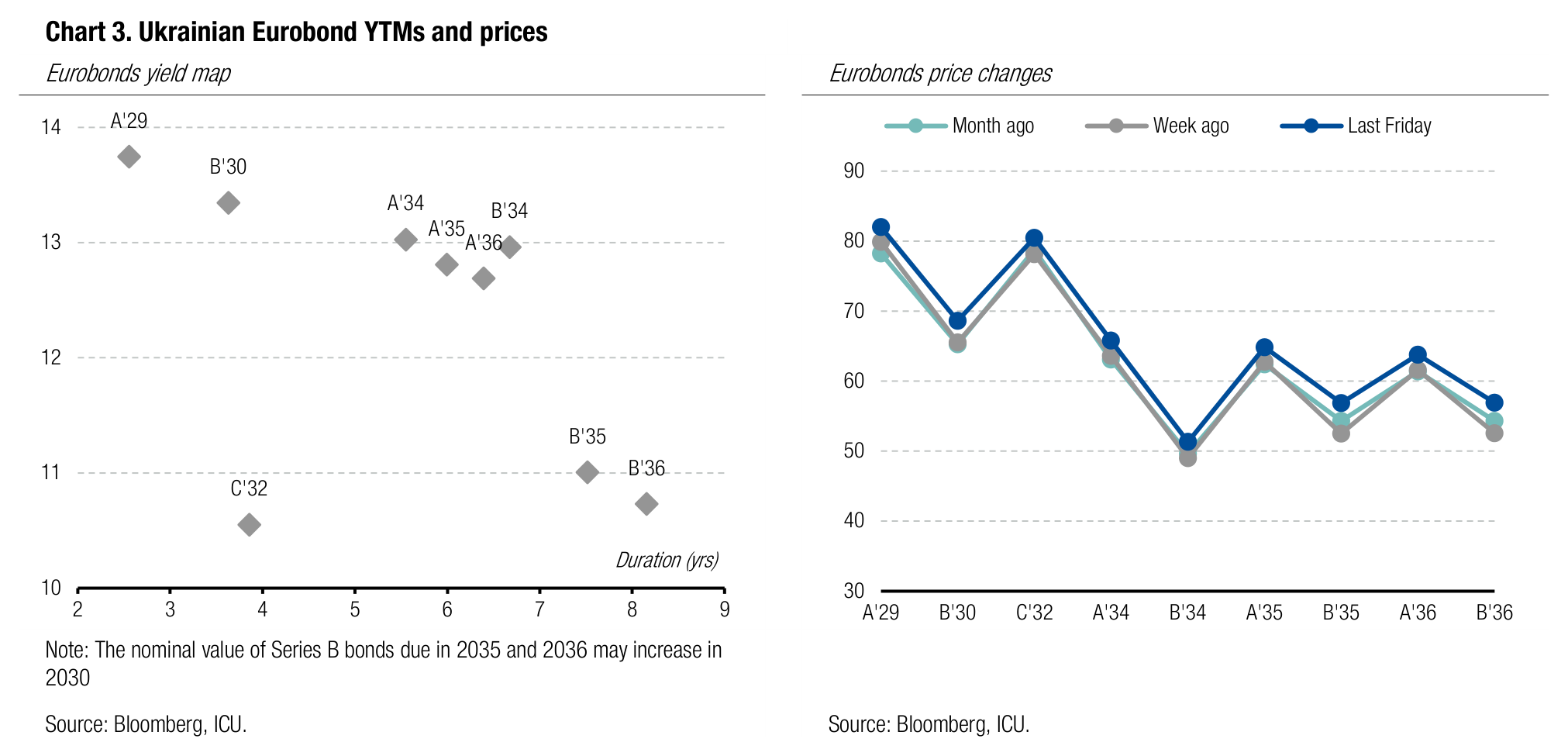

Last week, Ukrainian Eurobond prices rose significantly on expectations that the short-term ceasefire could be extended and grow into a renewed negotiation process.

In early May, Ukraine proposed a ceasefire from May 6 to commemorate the end of the World War II, but russia rejected the initiative. A few days later, the US president proposed a ceasefire for May 9-11, to which both Ukraine and russia agreed. The proposal also included a large-scale prisoner exchange. That had an outsized positive impact on bondholders' sentiment, especially after Ukraine did not rule out extending the ceasefire beyond the 11th. Later, putin's repeated statements about his readiness to negotiate and meet with the President of Ukraine to finalise the agreement significantly boosted investor sentiment even further.

Against the backdrop of a slight decline in the EMBI index till Thursday, Ukraine Eurobond prices rose by 4-11% with an average increase of over 6%. However, after the EMBI index declined by 0.7% last Friday and 1.3% over the past week, investor sentiment worsened, and for the full week the price increase moderated to 3-8% depending on paper, less than 5% on average.

ICU view: russia agreed to the ceasefire proposed by the US, solely to hold mass events to celebrate the 9th of May safely, and subsequently returned to massive shelling and its usual aggressive rhetoric regarding the Donbas. That leaves little hope for any kind of breakthrough in the negotiation process in the near future, moving bonds back under the impact from global sentiment to developing countries.

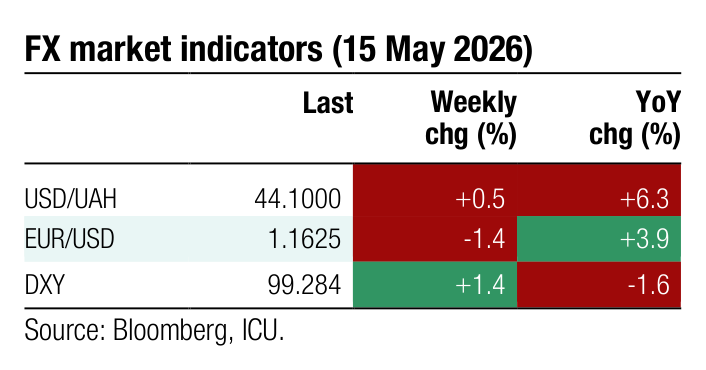

Foreign exchange market

Hryvnia fluctuation upper range limit above UAH44/US$

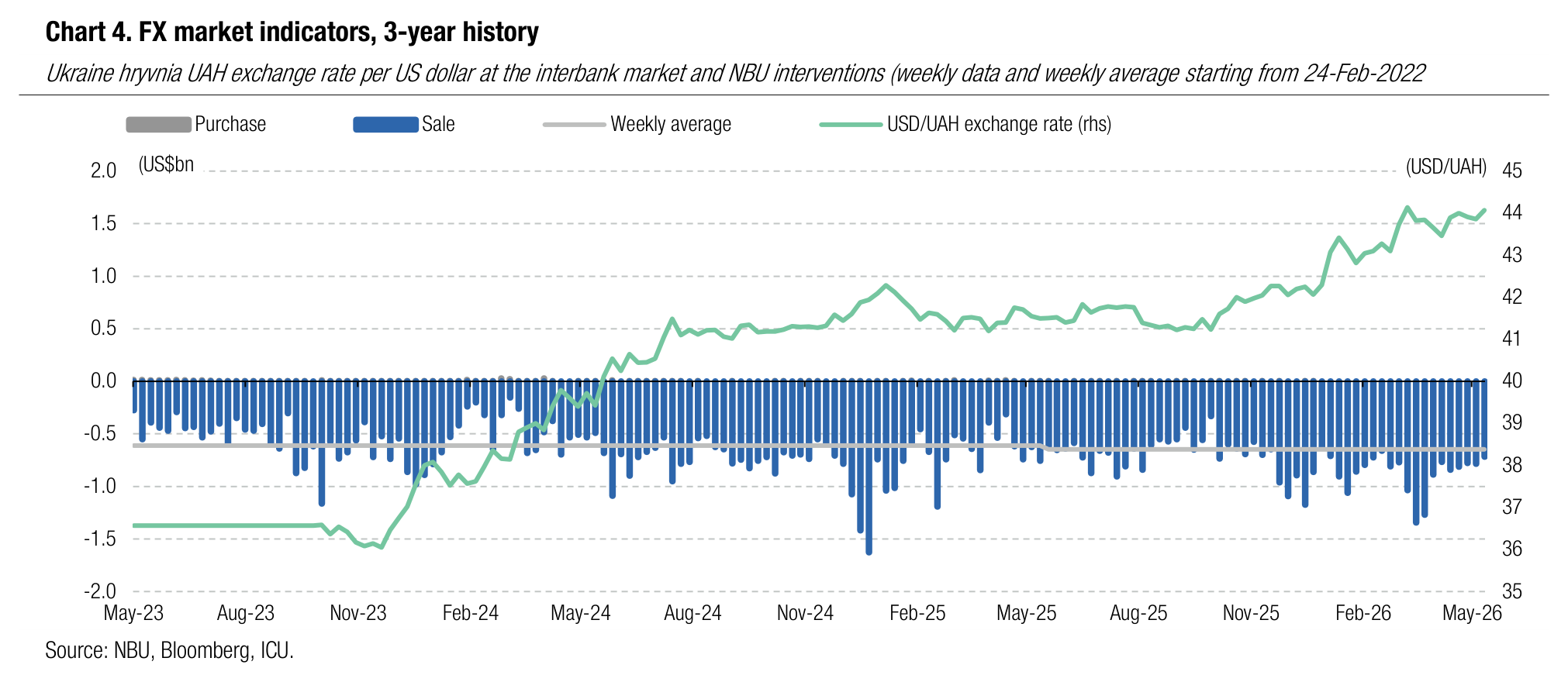

Last week, the NBU allowed low volatility of the USD/UAH exchange rate, but on Friday, the upper range bound crossed UAH44/US$.

From Monday to Thursday, the NBU allowed the exchange rate to fluctuate slightly below UAH44/US$, but on Friday, the National Bank set the official exchange rate at UAH44.07/US$. That’s the third time this year when the official rate exceeded UAH44/US$.

Over the four business days of last week, the foreign currency shortage was relatively small at US$364m, almost quarter less WoW. During these days, NBU spent US$570m on interventions, but the full-week amount totalled US$718m, down by 8% WoW and 16% below this year's average.

ICU view: The NBU raised the fluctuations range last Friday from UAH43.85-43.95/US$ to above UAH44/US for no clear reason. Yet, the rate was still below March highs. Daily interventions were roughly even during the week, and the FX deficit in the market continued to narrow. Last Friday's weakening of the hryvnia demonstrates the NBU's willingness to allow for greater exchange rate volatility, especially ahead of the IMF mission, but without an exact appetite for a faster hryvnia devaluation.