Ukrainian bond market

Retail portfolio at new high

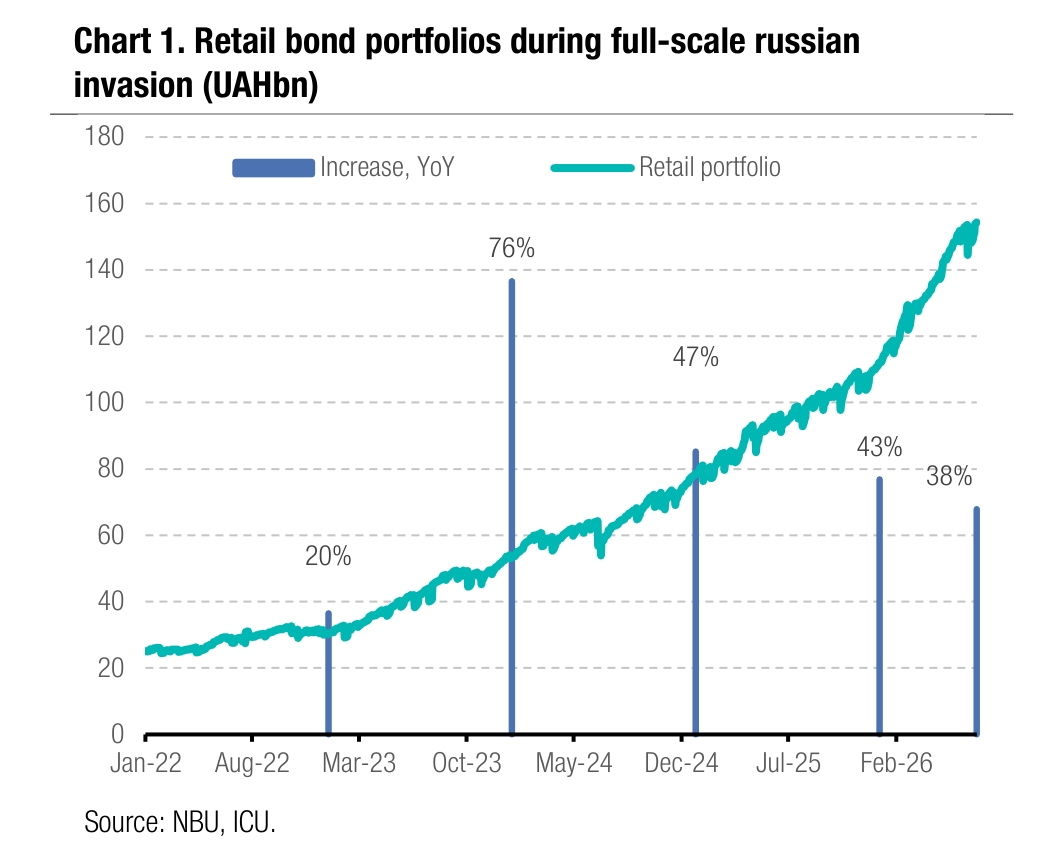

Retail investment in government bonds continues to gain momentum and reaches new highs.

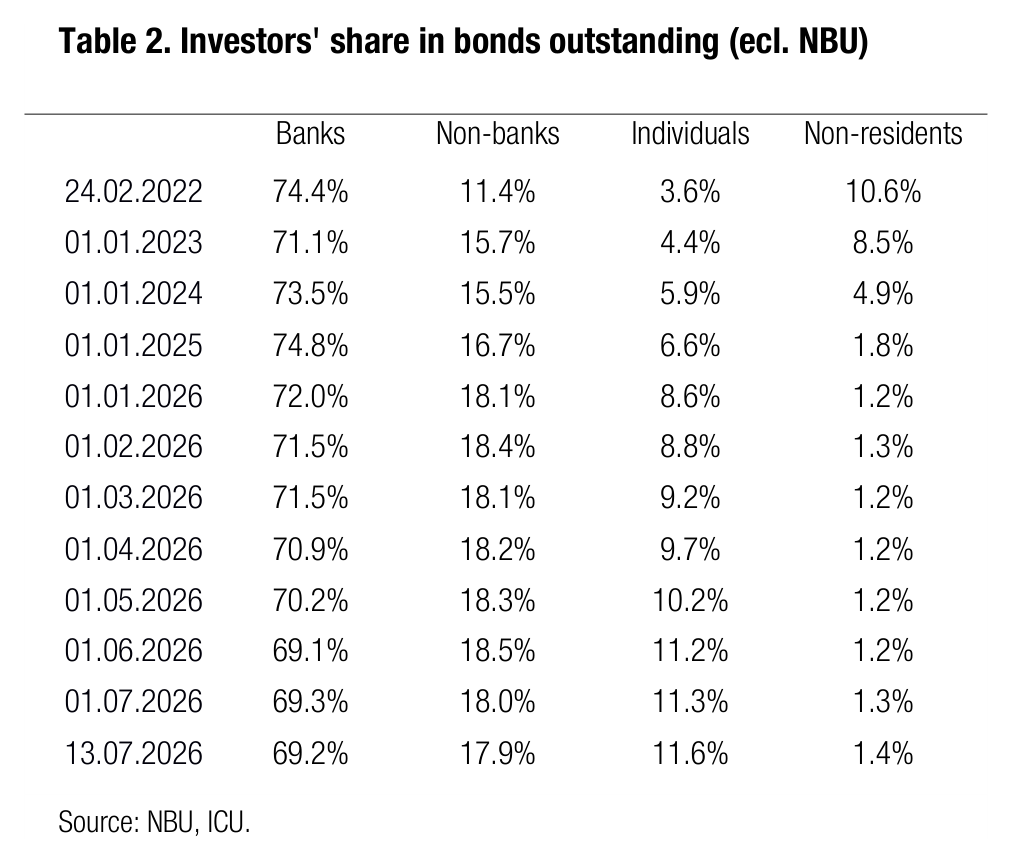

As of today, the size of the retail portfolio exceeded UAH154bn, implying growth of almost 38% YTD and a six-fold increase since the start of the full-scale war. The share of the retail portfolio in the total local government bonds outstanding (excluding bonds owned by the NBU) increased to 11.6%. The share of UAH-denominated bonds in retail portfolios remains above 60%.

ICU view: Despite a sharp devaluation of the hryvnia in June, the share of FX- denominated bonds remained below 40%. The population’s interest in UAH bonds is driven by high interest rates and favourable taxation rules. Stabilisation of the hryvnia in the range of UAH44.5-45.0/US$ may weaken the household's devaluation expectations and drive even further increase in the share of UAH instruments in the coming weeks.

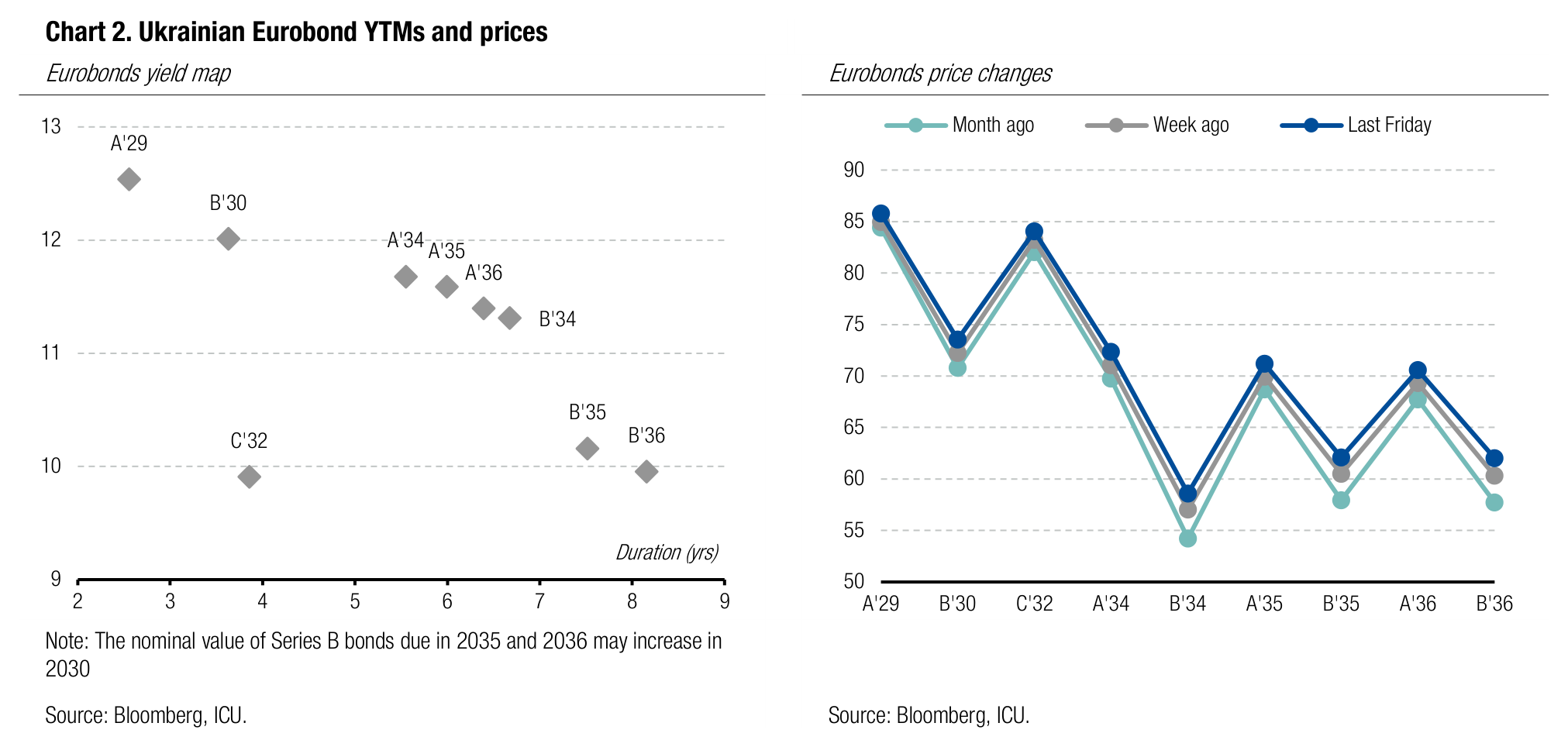

Eurobonds at new highs

Last week, the prices of most Ukrainian Eurobonds rose to new highs.

Last week, investor optimism peaked due to the NATO summit in Ankara, as Ukraine was one of the central topics, and the allies reconfirmed their support in the fight against the aggressor. Therefore, prices of all bonds rose, and, except for two series B bonds due in 2035-36 (whose volume outstanding may increase if GDP exceeds the IMF forecast level in 2028), reached new highs. At the same time, the EMBI index slid by 0.2%.

ICU view: During the NATO summit, the US confirmed they stand together with Europe in their support for Ukraine. That clear message strengthened investor optimism that had built up in the preceding weeks. The increase in Ukraine's defence capabilities undoubtedly brings the prospect of ending the war closer, but this prospect does not seem near at this stage.

Foreign exchange market

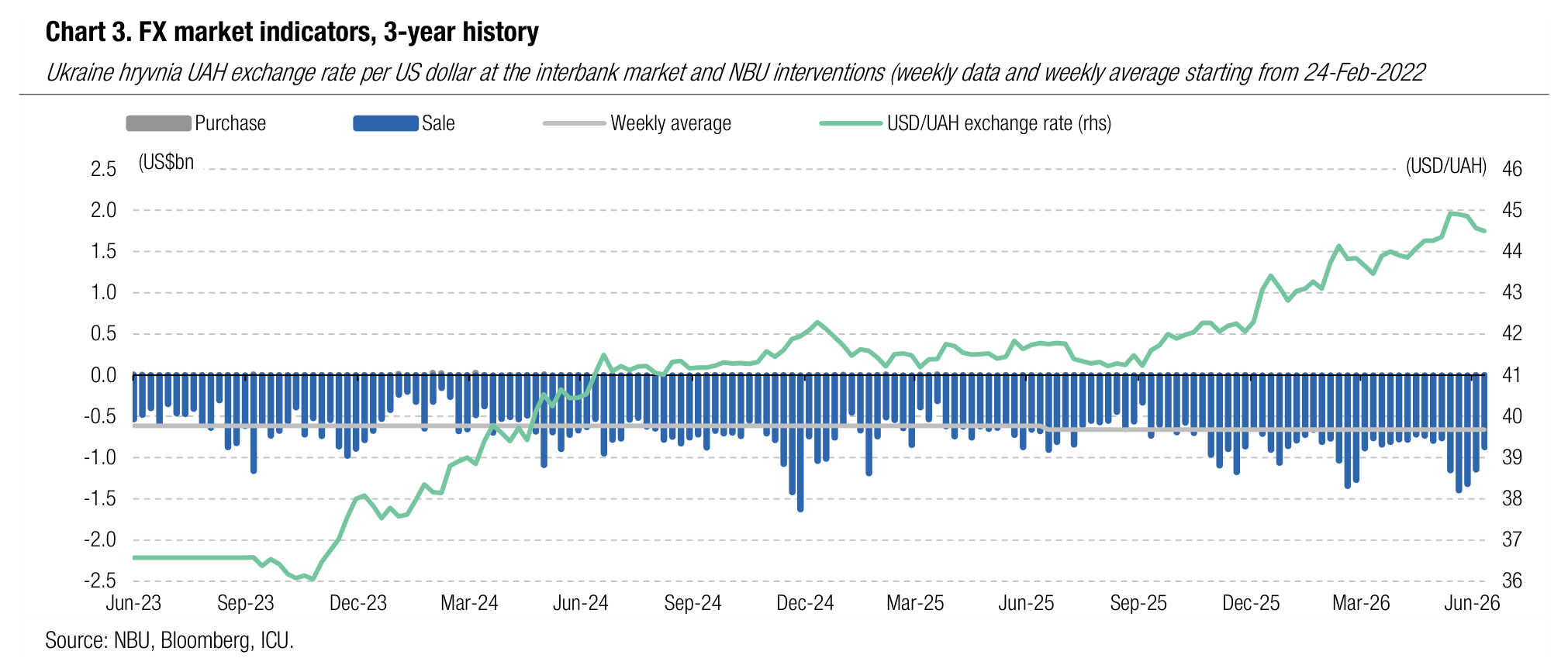

NBU stabilises hryvnia

The National Bank allowed the hryvnia to fluctuate only slightly last week, with rate staying just above UAH44.5/US$.

The FX shortage narrowed by a third last week to US$552m. Net foreign-currency purchases in the interbank FX market fell by 42% on a significant reduction in demand from legal entities. At the same time, households increased purchases of foreign currency after the hryvnia strengthened in the proceeding weeks. The National Bank reduced interventions to US$871m, slightly below this year's weekly average.

ICU view: The imbalances in local FX market are narrowing but they are still elevated and far from the level that is comfortable for the NBU. The National Bank may tactically strengthen the hryvnia even further during the summer to weaken depreciation expectations and improve the market supply-demand pattern. Yet, in the medium term, the continued weakening of the hryvnia is the only rational scenario for the NBU.

Economics

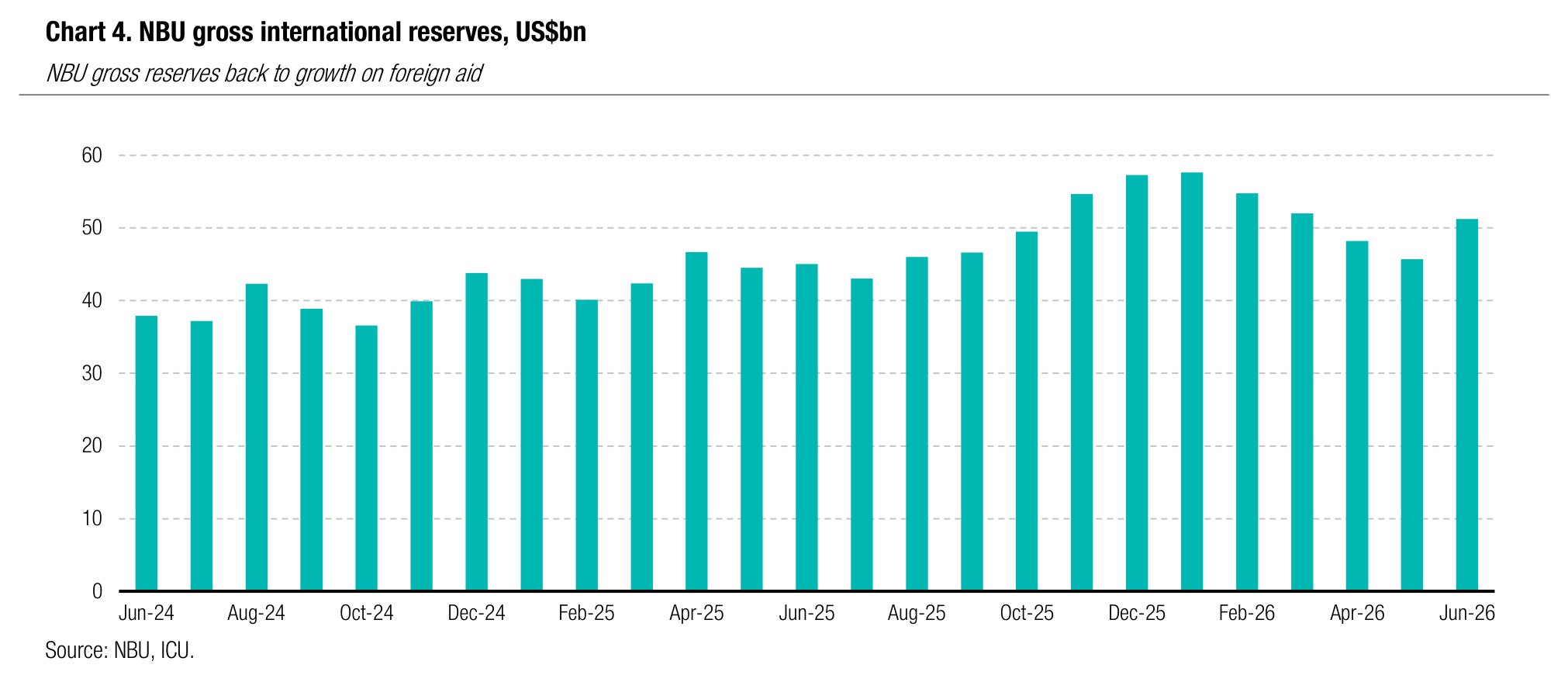

NBU reserves recover on new foreign aid

Gross international reserves of the NBU spiked 12.1% in June to US$51.3bn on hefty inflows of foreign aid. The reserves were equivalent to 5.2 months of future imports, according to the NBU estimates.

Growth in reserves came on the back of substantial inflows of foreign aid that included $6.8bn tranches of Ukraine Facility and a USL loan from the EU, and a US$4.5bn facility from the World Bank. Additionally, Ukraine received US$4.4bn of the EU financing earmarked for drone purchases, but that facility was not included into NBU reserves given its limited utilization scope. The reserve outflows were driven by NBU FX interventions that amounted to US$5.1bn and US$0.4bn of outlays on the servicing of external debt.

ICU view: The renewed inflows of foreign financial aid reversed the declining trend of NBU gross international reserves. We expect that foreign aid inflows in 2H26 will remain substantial so that the NBU is able to maintain its sizeable FX market sale interventions. The NBU gross reserves will remain volatile in 2H26 due to uneven inflows of external financing, but they should end 2026 at just below US$60bn.

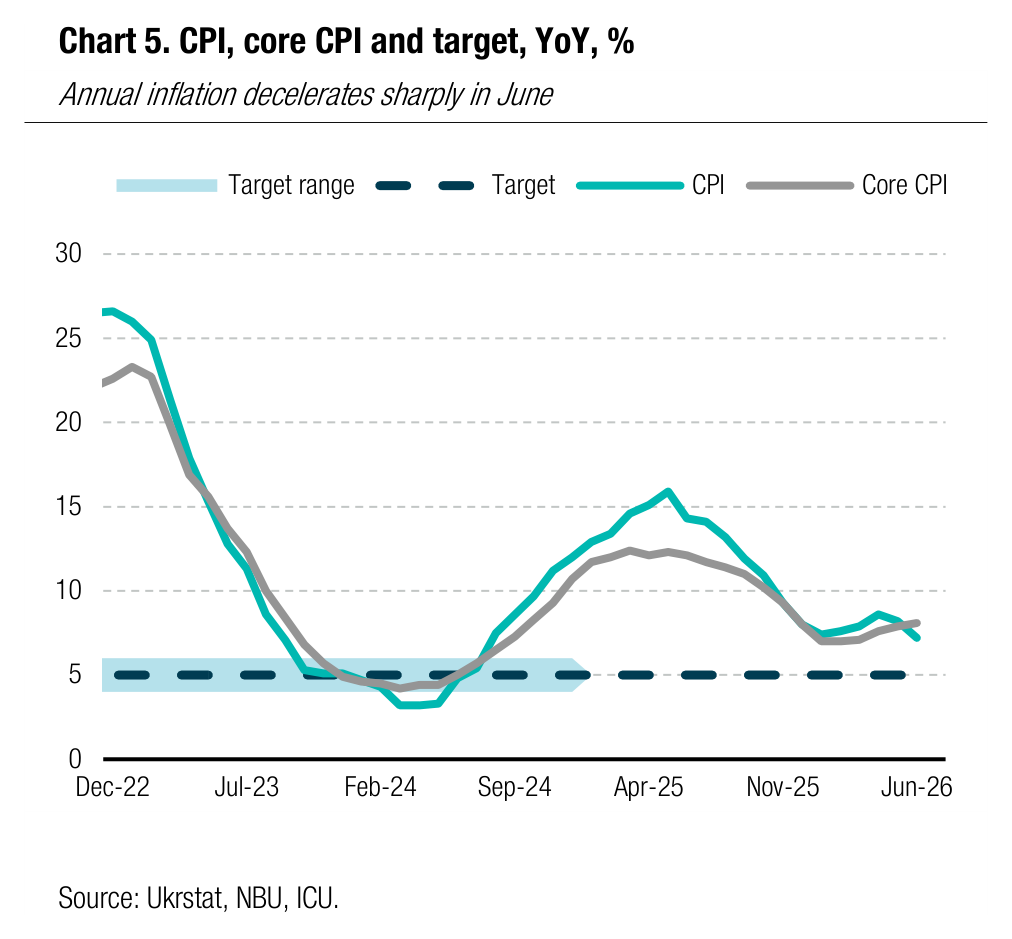

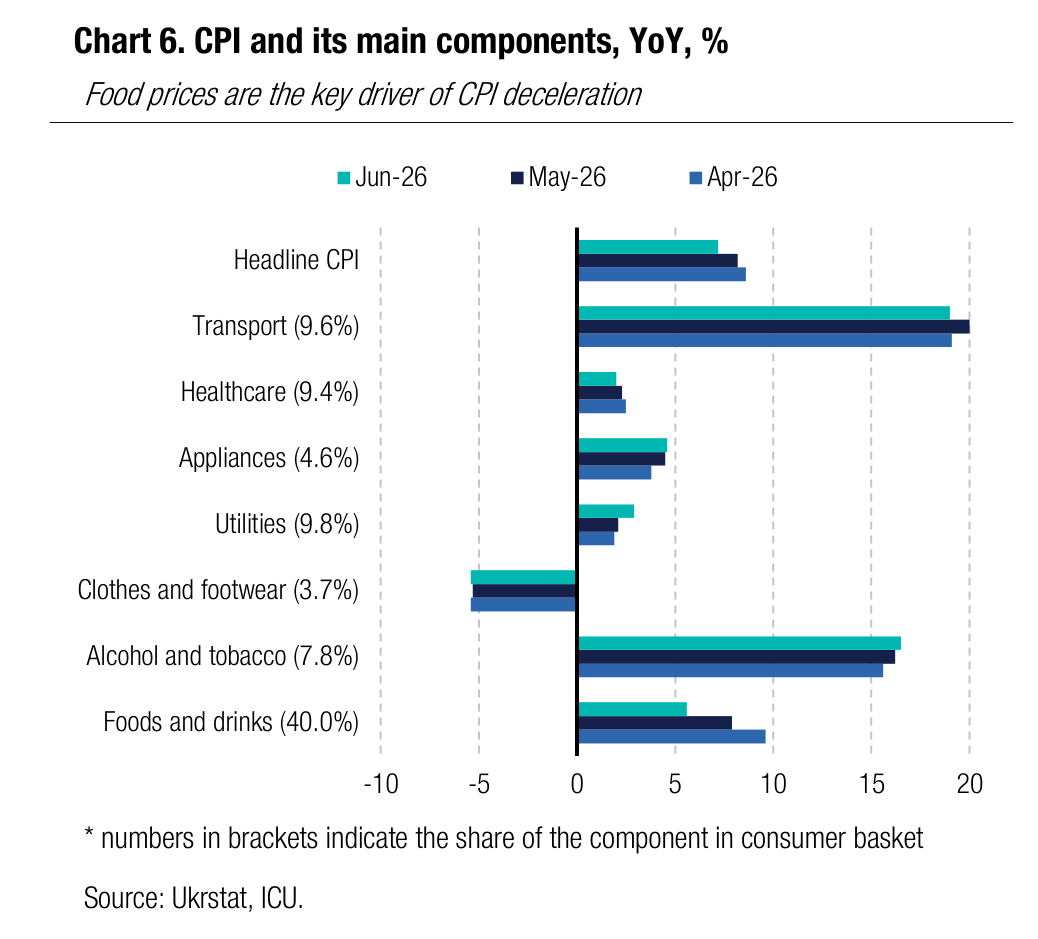

Inflation decelerates sharply in June

Annual CPI decelerated to 7.2% in June from 8.2% in May. Core inflation was marginally up to 8.1% YoY.

The monthly decline in consumer prices of 0.1% was a surprise that was primarily driven by a 0.8% MoM decline in food prices. In annual terms, food prices decelerated to 5.3% from 7.5% in May. Yet, the trend was mixed across other consumer basket components. The annual price increase for transportation services decelerated marginally to 19% (vs. 20% in May) as a partial normalization in the global energy market had a very limited impact on the motor fuel prices (-1.6% MoM). Prices for hotels and restaurants, a consumer basket component that is very sensitive to cost pressures, also slowed a bit to 13.6% (vs. 13.8% in May). Price growth for most other components picked up, including for the housing utilities, alcohol & tobacco, telecommunication, education, and housing amenities.

ICU view: The seasonal decline in the price of food staples in June was stronger than expected and that may imply less potential for price decreases in July and August. The continued acceleration of annual prices for many important goods and services, as well as a higher core CPI, signal that inflationary pressures remain elevated. Second- round effects of surging fuel prices have spilled into CPI in May-June, and they are unlikely to be reversed even if energy prices continue to trend down (that is a strong assumption in itself given the renewed tensions between the US and Iran). We also think that gradual hryvnia depreciation is set to continue adding some pressure to inflation. Annual inflation will remain volatile through 1H26, and we expect it may exceed 9% at the end of 2026 before a firm decelerating trend sets up in early 2027. The NBU is, thus, bound to keep the key policy rate at the current level of 15.0% at least until 1Q27.