|  |

|  |

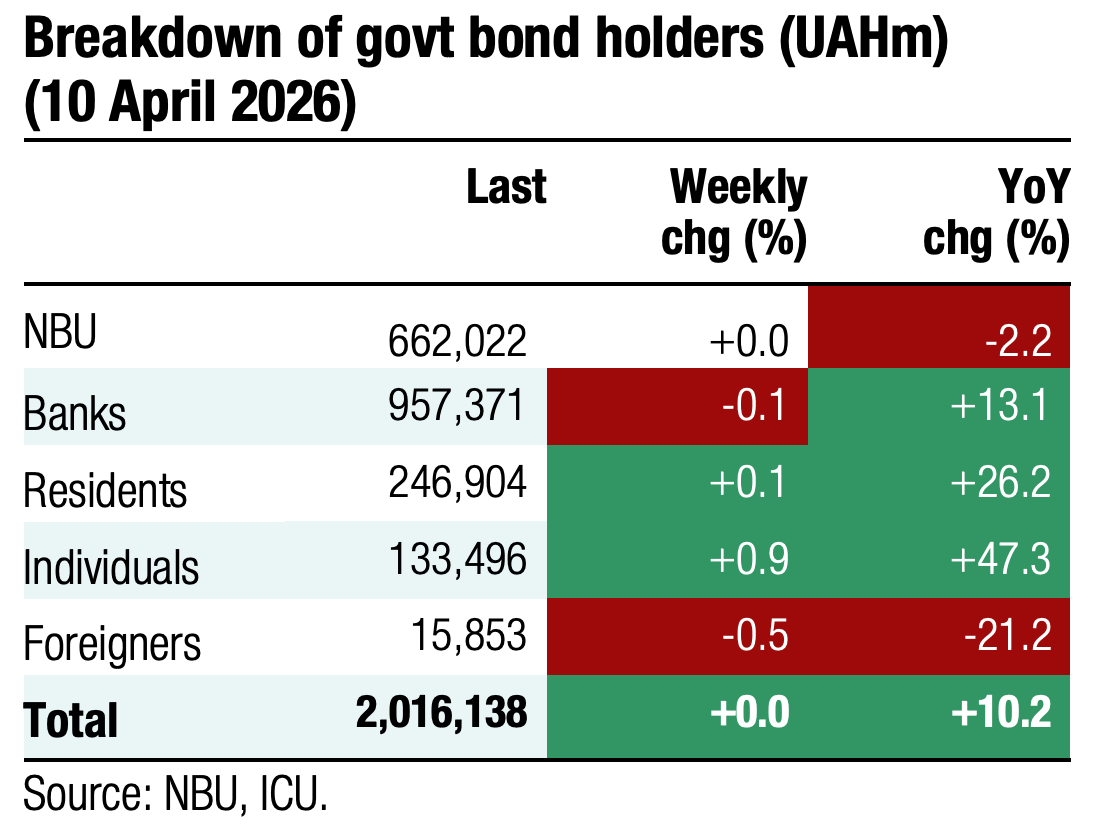

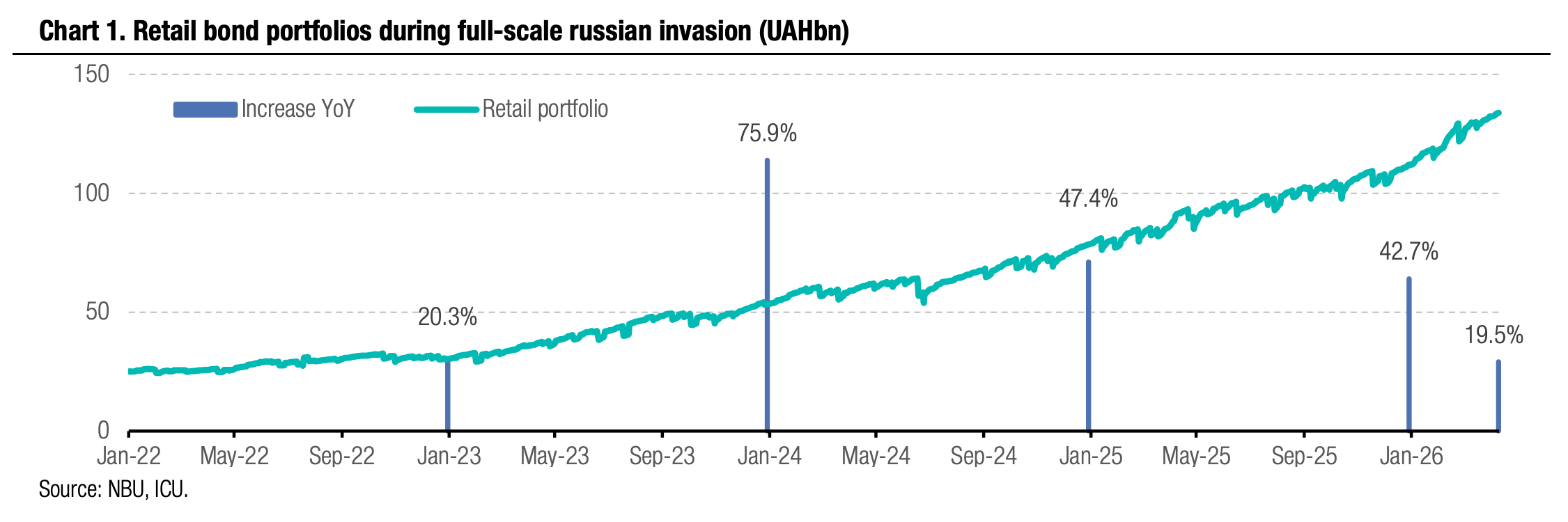

Bonds: Households further increase portfolio of UAH bonds

Household investments in domestic government bonds reached a new high in early April, and the share of UAH instruments exceeded 63%.

Household portfolios are up UAH21.8bn or 19.5% YTD to almost UAH134bn. Growth remains driven by hryvnia-denominated bonds, up by UAH18.5bn YTD, well above the UAH3.3bn increase in FX-denominated securities. The growth of the latter is partly due to FX revaluation effects. All in, the share of UAH instruments in retail portfolios exceeded 63%, up by 4pp YTD. This share continues to grow even though the Ministry of Finance cut yields on UAH bonds substantially YTD: by 120bp for one-year bonds and 165bp for three-year notes.

The share of retail portfolios in total government bonds outstanding reached almost 10% (excluding bonds owned by the NBU).

ICU view: UAH bonds are enjoying growing interest among households, as they offer significantly higher yields than bank deposits. Against the backdrop of tight monetary policy and moderate exchange rate flexibility, UAH bonds remain an attractive investment instrument in the Ukrainian financial market. We expect a further increase in both retail bond portfolios and the share of the hryvnia-denominated instruments. At the same time, we expect the Ministry of Finance will continue to reduce outstanding FX-denominated bonds, so the availability of this instrument will continue to decline.

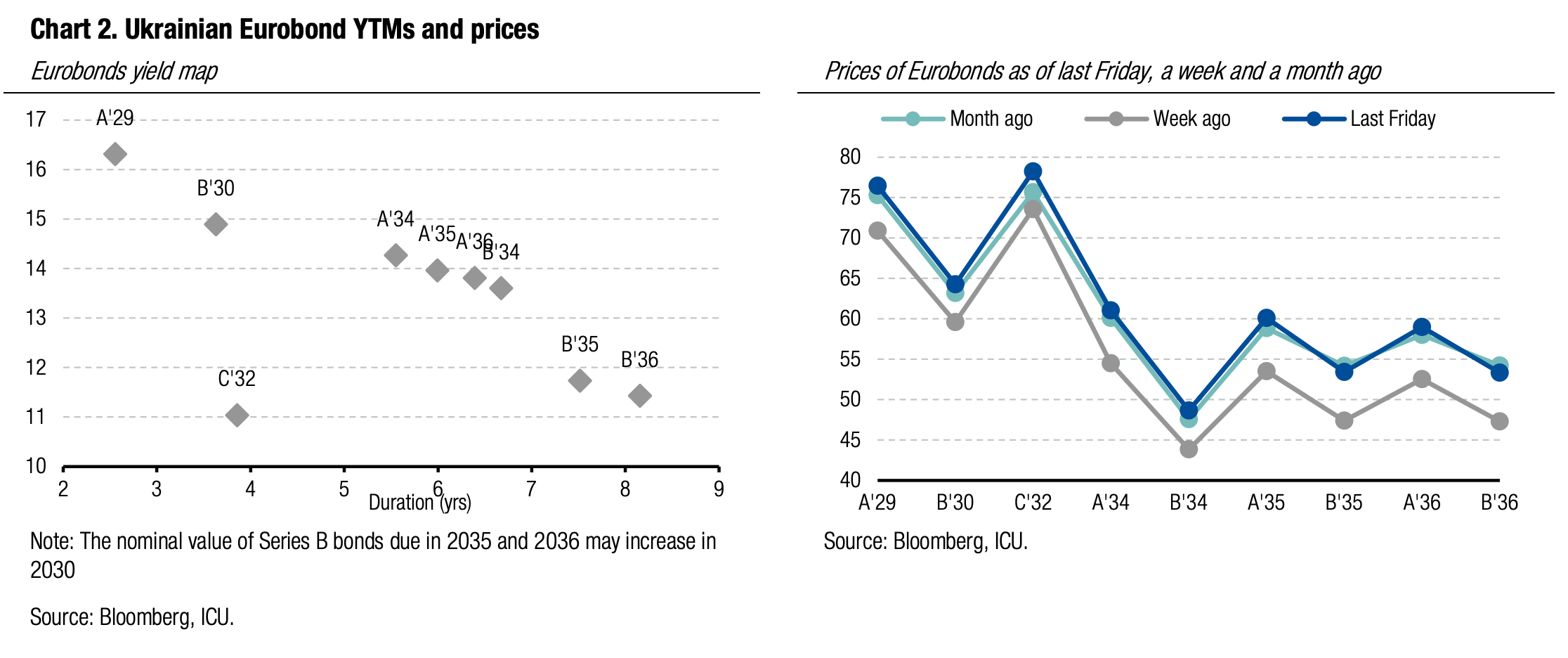

Bonds: De-escalation in Iran gives new reasons for optimism

The ceasefire and peace talks in Iran raised expectations that eventually the issue of the russia war in Ukraine will regain importance for the US leadership. This belief brought a new wave of optimism among global investors.

Following the announcement of a ceasefire in Iran, EM bond prices rose sharply with the EMBI index rising by 1.8% last week. Meanwhile, prices of Ukrainian Eurobonds rose by an average of 7% in anticipation of a resumption of peace talks. Last Friday, the statements of the head of the Presidential Office, K. Budanov, added even more significant positive effect, as he claimed the ceasefire negotiations are moving in the right direction, and it will not take a lot of time to achieve tangible results. On Friday, Ukraine Eurobonds rose by another 3%, taking the three-day increase to 10%.

ICU view: We do not expect a significant breakthrough in the peace talks between Ukraine and russia in the near future and consider the current optimism to be premature. The significant increase in oil and gas prices gives russia additional space to fund the war, so it will continue to attempt to make significant breakthroughs on the front line during the spring and summer.

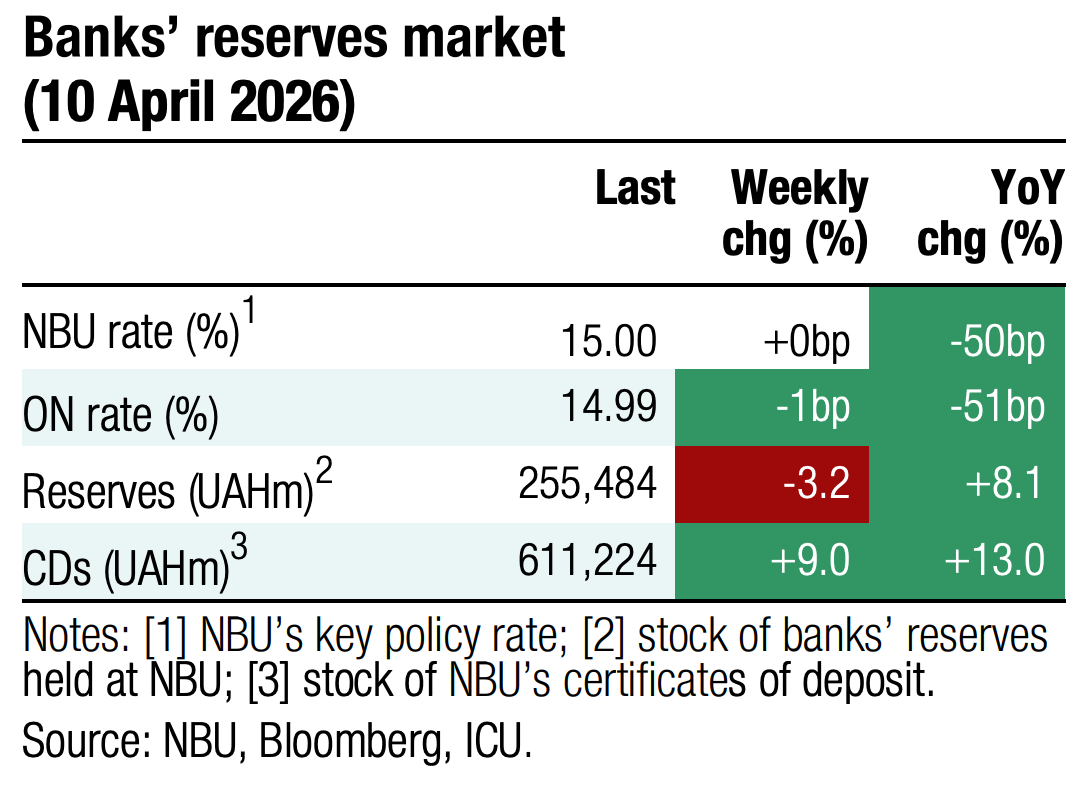

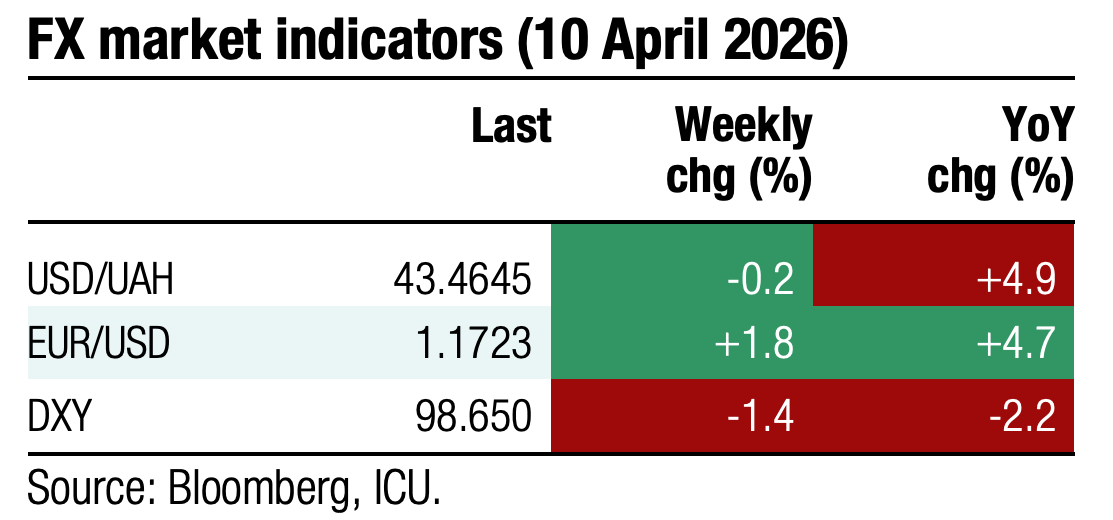

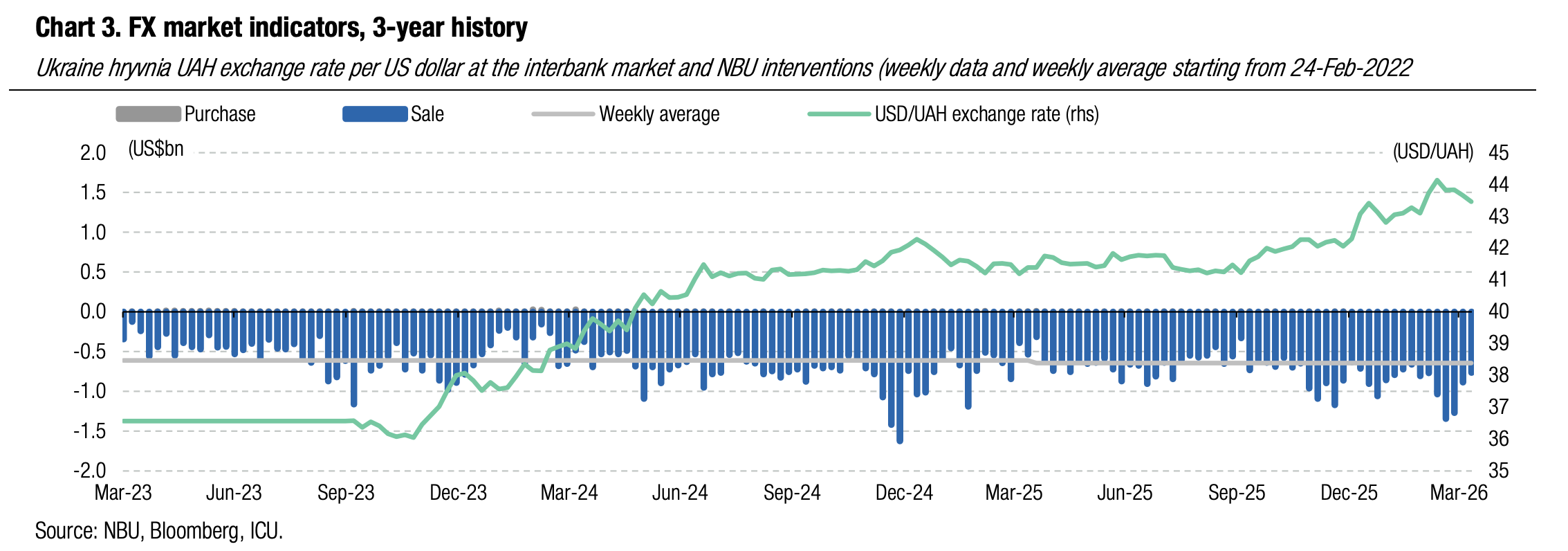

FX: NBU reduces interventions further

The National Bank reduced interventions below the YTD average weekly and maintained the hryvnia exchange rate close to UAH43.5/US$ throughout the week.

Last week, the NBU allowed the hryvnia to fluctuate in a very narrow range, mostly below UAH43.5/US$, and the hryvnia even strengthened marginally during the week. To keep the exchange rate stable, the NBU intervened to the tune of US$766m, below this year's average weekly volume.

The stabilisation of the hryvnia exchange rate came on the back of lower FX market shortage that stood at US$528m as demand narrowed by 7% while supply fell by 12% (in four business days).

ICU view: Last week, the NBU once again proved it is prepared to maintain elevated FX market interventions to keep the hryvnia exchange rate below UAH44/US$. We assume that the NBU will keep the exchange rate close to its current level in the coming weeks to lessen exchange rate stability concerns among households and businesses.

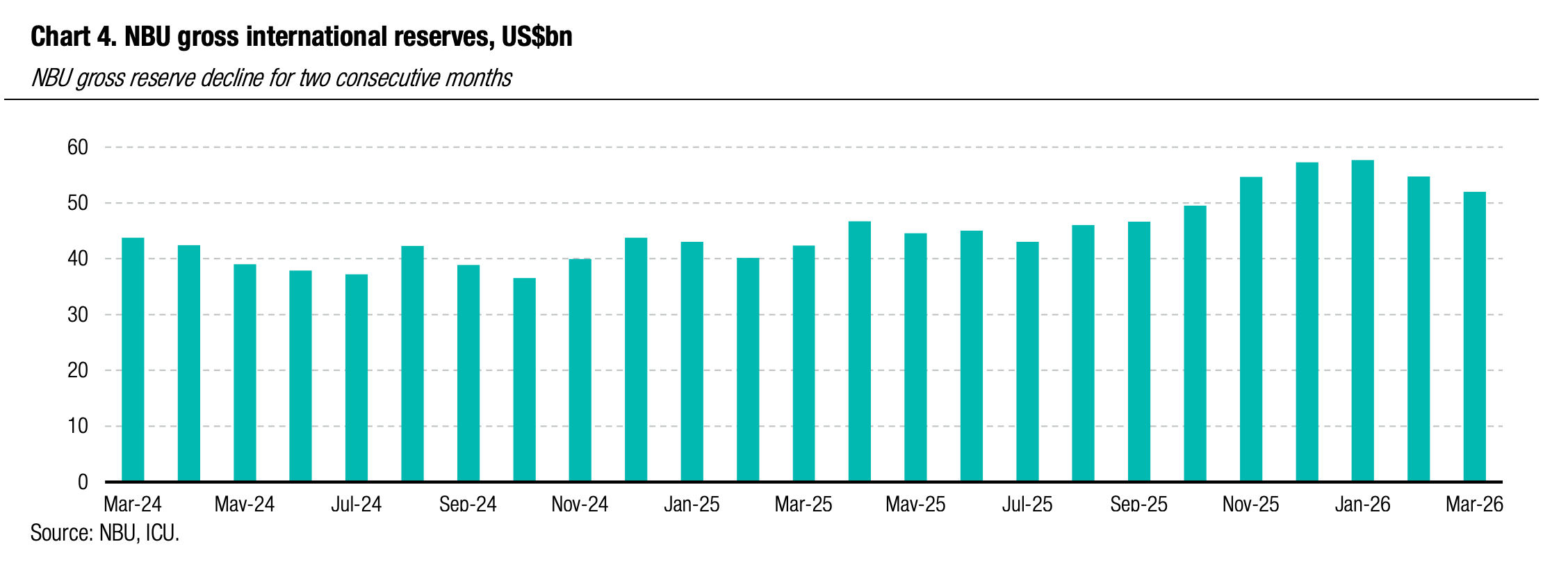

Economics: NBU reserves down 10% from January peak

Gross international reserves of the NBU declined 5% in March to US$52bn and 9.8% from the January peak of $57.7bn. Reserves stood at 5.5-month equivalent of future imports, according to the NBU estimates.

The decline in reserves reflects a substantial deceleration in inflow of foreign financial aid against the backdrop of elevated FX interventions of the central bank. In March, the NBU reserves were replenished with a US$1.5bn loan from the IMF and US$1.5bn tranche of the ERA facility. Meanwhile, the NBU sold net $4.8bn in the FX interbank market to alleviate excessive pressure on the hryvnia. On top of that, c. US$0.4bn was spend on external debt servicing; the net FX revaluation effect of the NBU reserves was negative at c. US$0.7bn.

ICU view: NBU interventions remain elevated as the global energy crisis is taking its toll on Ukraine’s external position. YTD, the central bank spent US$12.6bn to maintain stability in the FX market, a 27% increase vs. the same period of 2025. Meanwhile, inflows of foreign financial aid remain relatively small, at just US$6.8bn in 1Q26, a tiny fraction of US$51.4bn of total loans and grants envisaged within the current IMF cooperation program. We expect financial aid from the EU to be unlocked following parliamentary elections in Hungary and the fresh inflows will keep the NBU reserves at above US$50bn through end-2026. We remain of the view that the NBU will have sufficient firepower to keep the FX market under its full control, albeit the huge imbalances of external accounts imply the need for a managed gradual hryvnia depreciation.

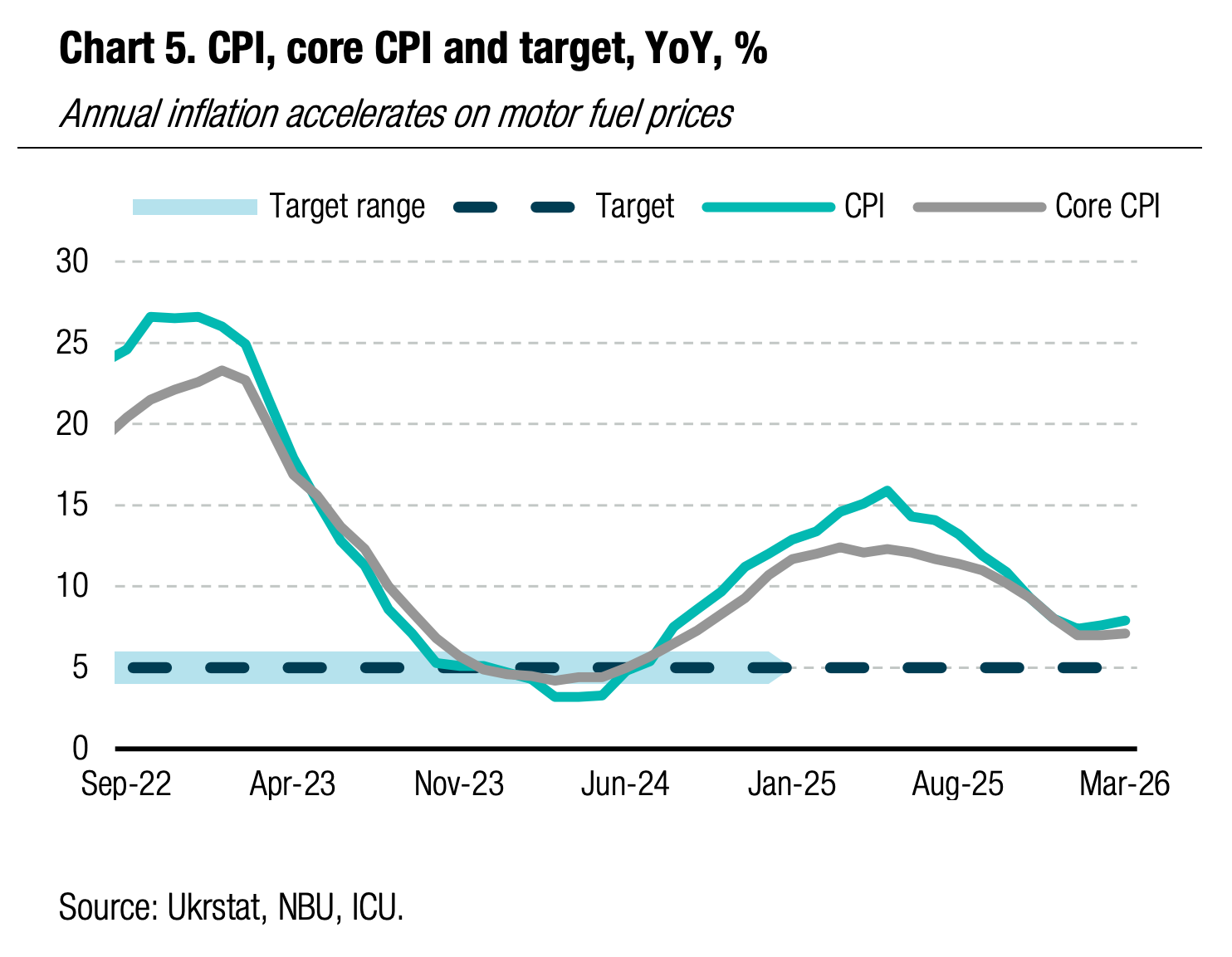

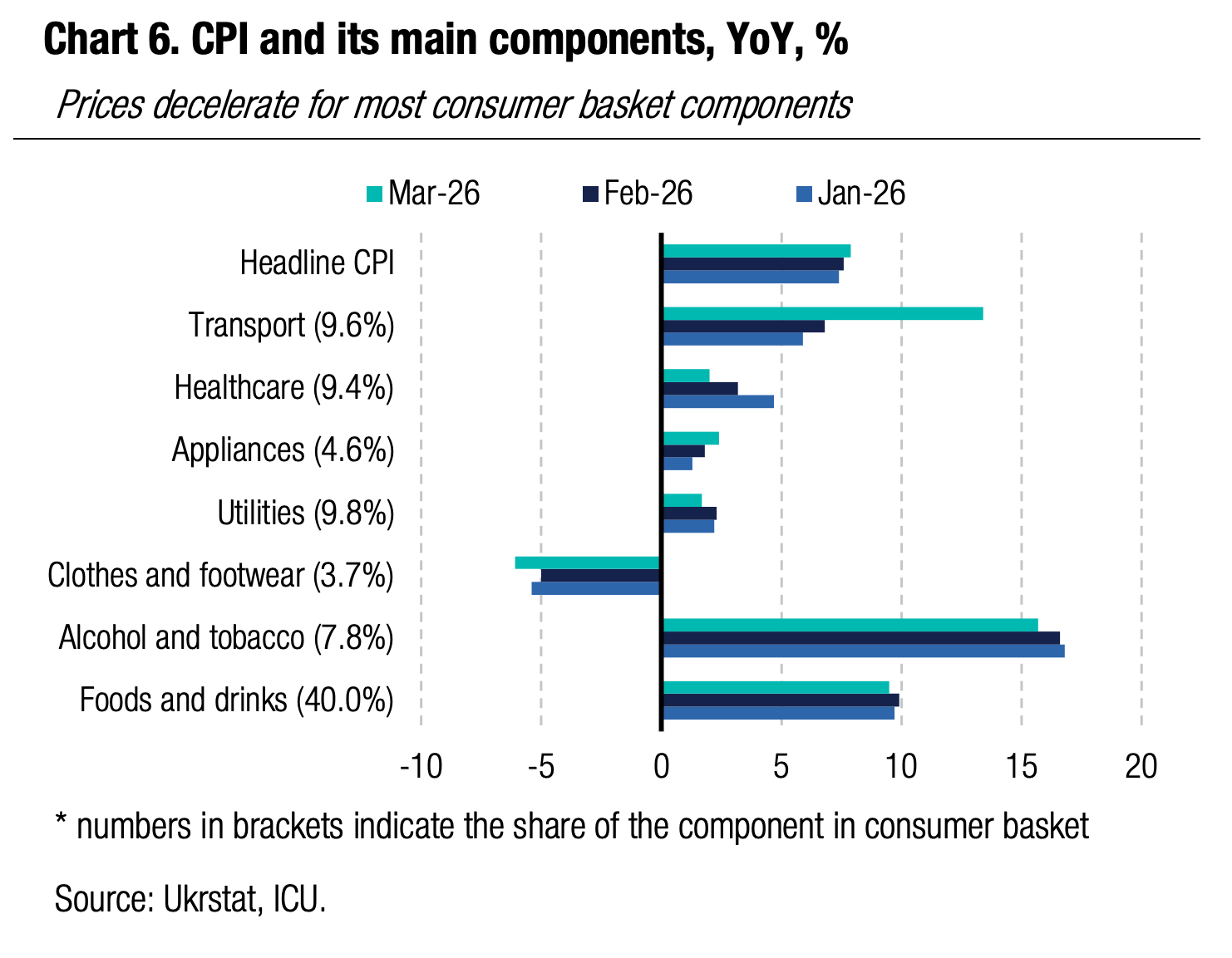

Economics: Inflation accelerates further in March

Annual CPI accelerated to 7.9% in March from 7.6% in February. Core inflation edged up to 7.1% YoY.

The spike in prices of motor fuel and tariffs for the transportation services was the key driver of monthly inflation in March contributing around 0.6pp to a 1.7% monthly tally. Communication services also saw an outsized increase in tariffs (+2.5% MoM and 14.9% YoY) as mobile operator companies continued to pass higher costs of alternative energy onto customers. Noteworthy, the annual inflation for many large and important consumer basket components continued to slow, including food (+9.3% in March vs. +9.7% in February), utilities (+1.7% vs +2.3%), and health services (+2.0% vs. +3.2%).

|  |

ICU view: The effects of the global energy crisis related to the Iran war continue to have an outsized impact on the consumer prices in Ukraine. The first-round effects in March are estimated at 0.5-0.7pp but if the energy crisis resolution is delayed, additional first-round effects and subsequent second-round effects may be much more substantial. At this point, we assume energy prices will reverse in May-June (but will not return to the February level through end-2026), implying annual inflation may be close to 8% at end-2026. We expect the NBU will keep its key policy rate unchanged at 15.0% at end-April, but delays with the crisis resolution beyond 2Q26 may accelerate prices further and bring the rate hike to the NBU agenda.