|  |

|  |

Bonds: MoF maintains rollover high

In February, the Ministry of Finance’s borrowings significantly exceeded repayments.

In February, the Ministry of Finance redeemed UAH28.6bn of UAH bonds, including bonds redeemed through a swap auction, and US$450m of FX paper. Meanwhile, the ministry sold UAH51bn and US$200m of new bonds at primary auctions. Thus, in February, the rollover of UAH debt rose to 178%, while the rollover for USD-denominated debt was only 44%. In addition, the MoF sold EUR91m of bonds with no redemptions in this currency YTD.

In total, for the 2M26, the domestic debt rollover was 141%, including 162% in hryvnia and 44% in US dollars. In euros, all EUR91 million are net borrowings.

ICU view: The State Budget Law and the recently approved IMF program provide for net repayments of domestic debt (rollover rate below 100%) for this year. Despite this plan, the Ministry of Finance started the year with very active borrowing. For now, elevated borrowings may be a hedge against a possible delay in financing from the EU. Even so, we expect that in the end, the ministry will target a 100% rollover for the full year.

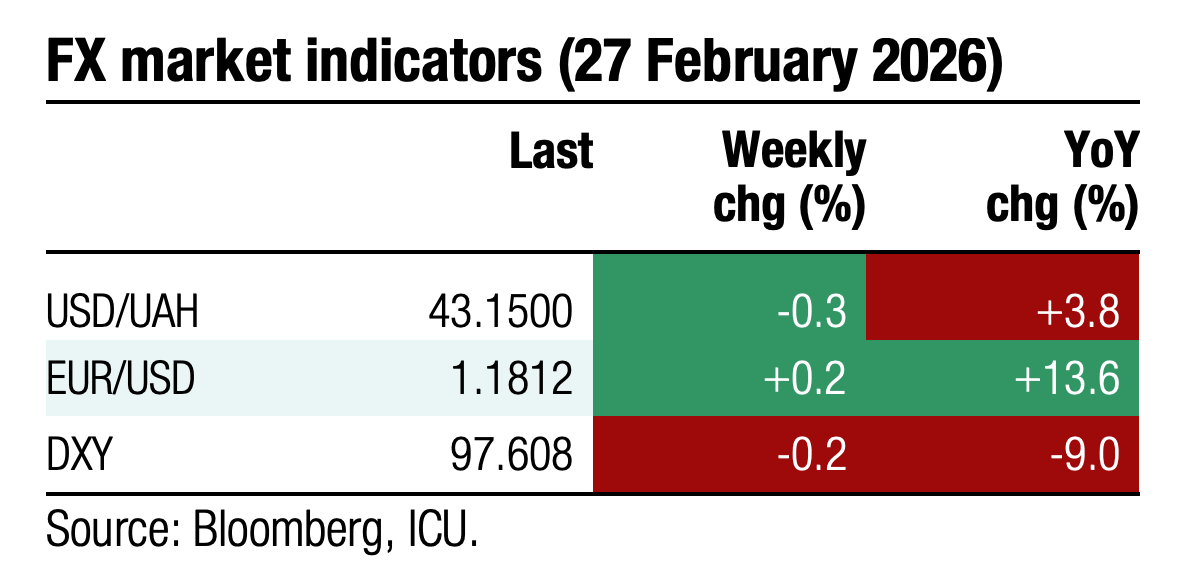

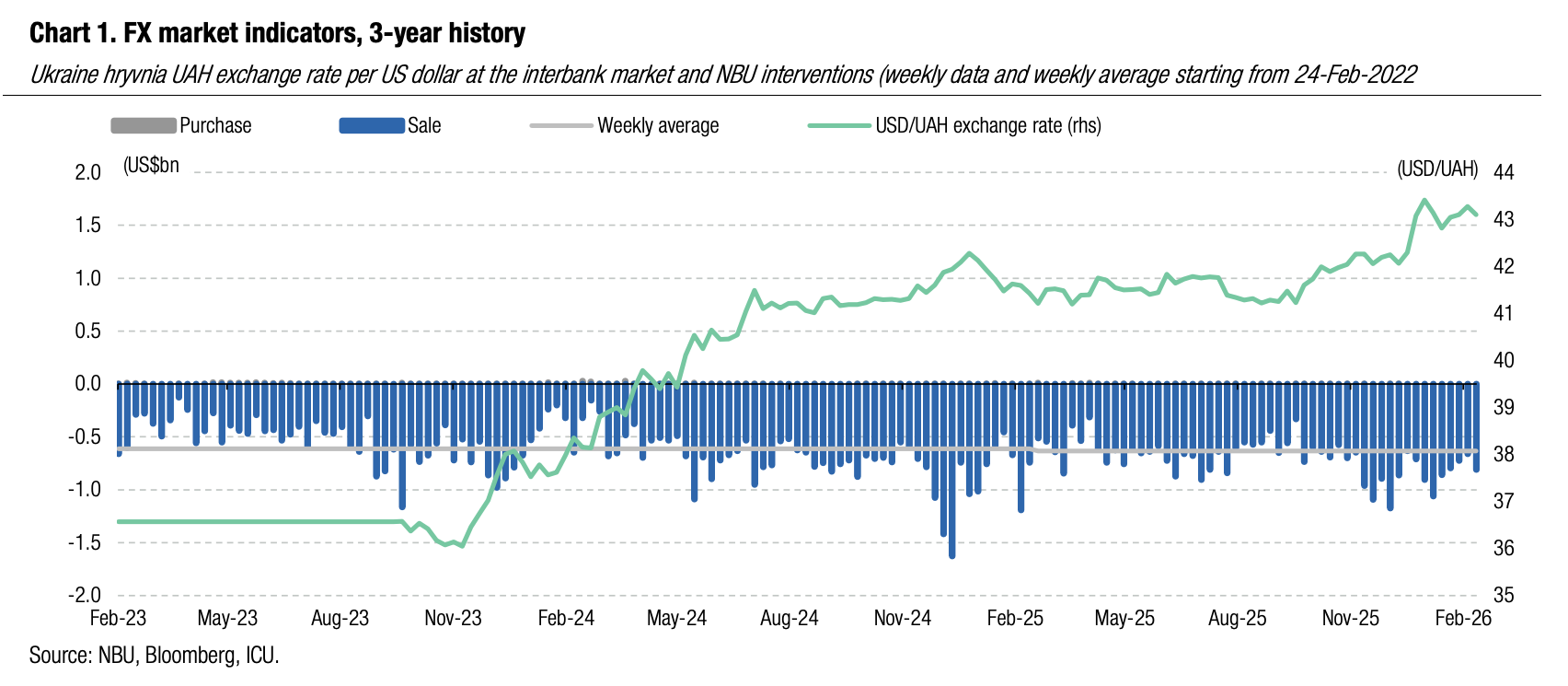

FX: NBU restrains hryvnia fluctuations despite higher FX deficit

Last week, the NBU strengthened the hryvnia while increasing interventions on a wider foreign currency deficit in the market.

The hard currency shortage in the market over four business days last week was US$541m, up 41% WoW. Demand for foreign currency in the interbank FX market rose by 49% to US$471m, while the retail segment deficit remained almost unchanged. To meet increased demand, the NBU had to increase interventions by almost a quarter WoW to US$810m.

On higher interventions, the National Bank even strengthened the hryvnia by 0.4% to UAH43.10/US$. In February, the USD/UAH official exchange rate weakened by 0.7%, and by 1.8% YTD.

ICU view: The National Bank clearly demonstrated last week that it has no appetite for weakening the hryvnia and that the hryvnia's drift to UAH43/US$ is only a matter of time. The new IMF program includes sufficient funding that fully enables the NBU to control the FX market and exchange rate in the foreseeable future. Still, the IMF clearly insists on greater exchange rate flexibility (see comment below). Therefore, we maintain expectations for the hryvnia to depreciate to UAH45/US$ by the end of the year.

Economics: IMF approves new EFF program for Ukraine

The IMF executive board approved a new four-year EFF loan for Ukraine for US$8.1bn, with US$1.5bn to be disbursed immediately.

The baseline scenario of the new program assumes the war will end in 2026, while the adverse scenario sees continuation of fighting that is being transformed into a frozen conflict in 2028. The key takeaway from the program memorandum is that Ukraine is expected to receive sufficient funding over the length of the program to maintain macroeconomic stability. The external funding package totals US$136.5bn, including US$101.2bn from the EU. The funding size is somewhat higher at US$146.3bn in a downside scenario. Given generous external funding, the IMF expects NBU reserves will increase to US$65.5bn at end-2026 and even further to US$73.4bn in 2027. The fiscal deficit will remain elevated at 19.3% of GDP in 2026 and 17.8% of GDP in 2027, but foreign aid will nearly fully cover the gap over the next two years. The program’s structural benchmarks focus on tax measures and structural reforms, some of them being socially sensitive.

ICU view: The parameters of the new program and a hefty external financing package imply the government and the NBU will be fully equipped to maintain macroeconomic stability in the foreseeable future. The central bank will have sufficient firepower to keep the FX market and hryvnia exchange rate under control. Yet, the IMF is crystal clear it expects greater flexibility (read depreciation) to avoid build-up of external imbalances and protect foreign exchange reserves. In view of this, we expect the NBU will let the hryvnia weaken to about UAH45/$ by the end of 2026. Our major concern about the IMF projections is an assumed rapid narrowing of external imbalances (net of official funding) starting from 2028. In reality, the gap of external accounts may remain much higher than projected by the IMF implying the need for a more significant and painful ER adjustments beyond 2027.