|  |

|  |

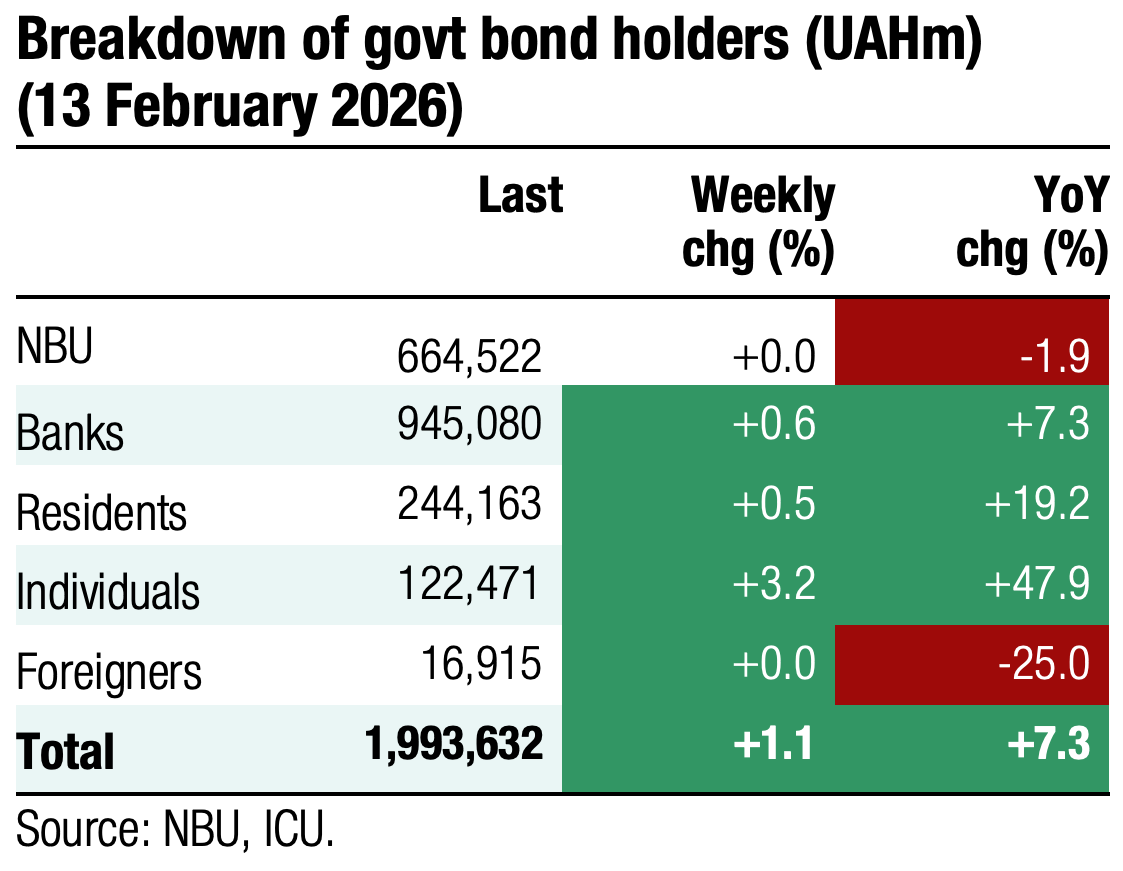

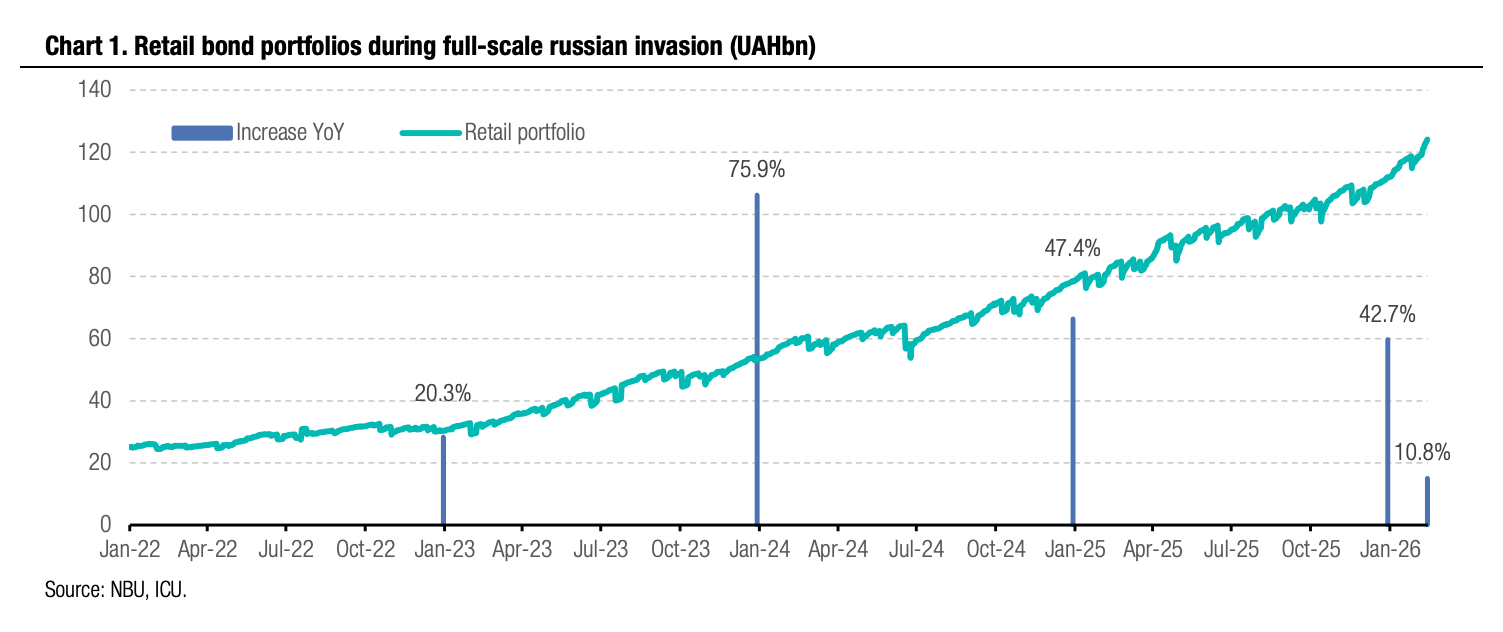

Bonds: Retail portfolio on upward trend

Retail portfolio reached UAH124bn (US$2.9bn) last week, driven by UAH instruments.

As of this morning, the volume of government bonds owned by households amounted to UAH124bn, which is UAH12bn or almost 11% higher than at the beginning of the year and implies an almost 5x increase since the start of the full-scale invasion. Investments into UAH bonds drove the increase as they were up by UAH8.3bn YTD. The size of FX-denominated paper was up by UAH3.8bn YTD, partly due to the hryvnia devaluation effect. Therefore, the share of UAH instruments in retails portfolio reached almost 60%, up 1pp YTD.

Retail portfolios’ share in the total volume of government bonds outstanding (excluding securities owned by the NBU) increased to 9.3% from 8.6% at the beginning of this year.

ICU view: Government bonds, especially UAH bonds, are attracting increasing interest of households as their yields significantly exceed the bank deposit rate. Expectations of further rate cuts by the NBU enhance the interest of retail investors towards investments in UAH bonds.

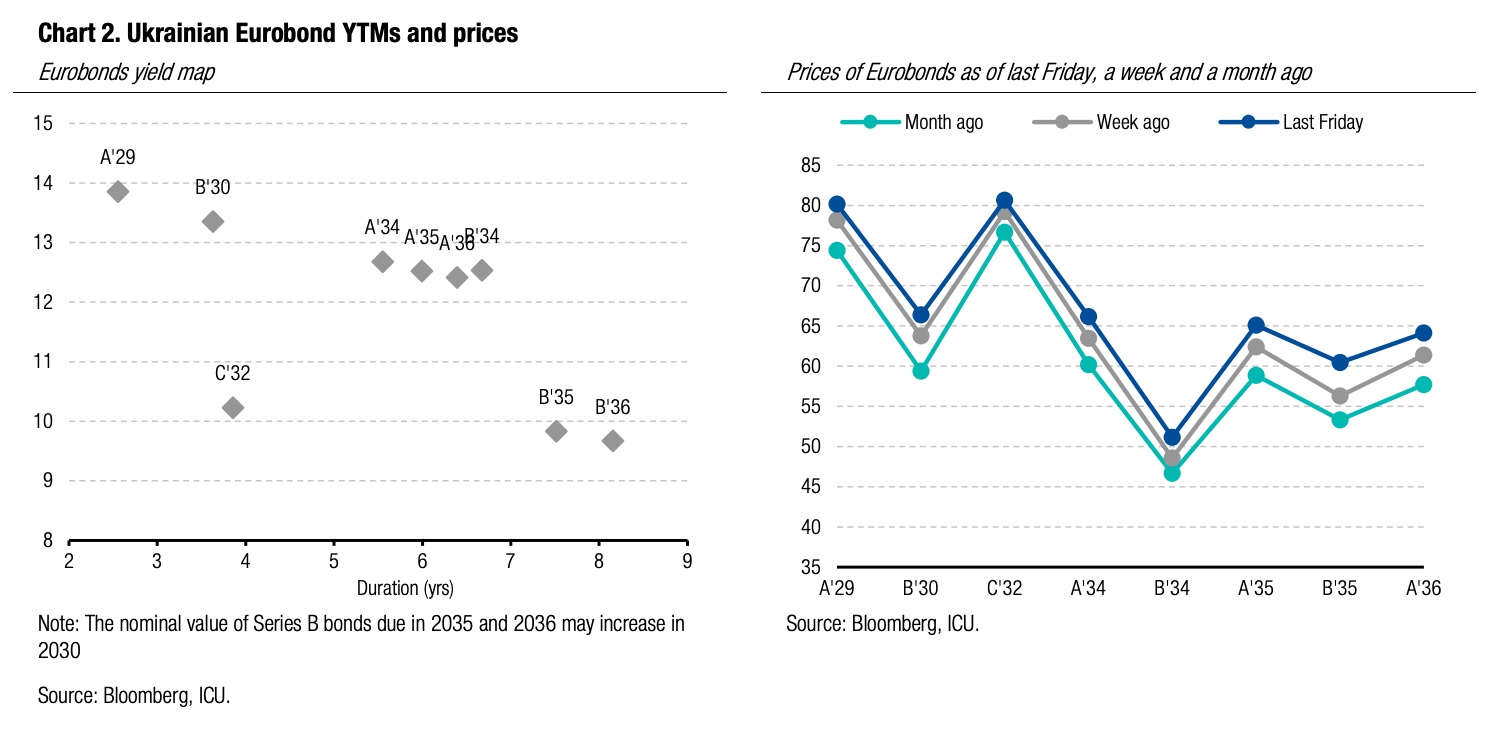

Bonds: Eurobond investors find new reasons for optimism

Ukraine Eurobond prices continued to rise last week, as investors sought reasons for optimism even in the absence of new substantial facts regarding peace talks.

Eurobond prices moved in line with the EMBI index for most of last week, rising by an average of 2%. But at the end of the week, a new wave of investor optimism emerged and price increase averaged almost 5%. Series B bonds, which are most sensitive to news of peace progress, enjoyed the largest gains.

The key factor that could have driven investor optimism was the news that Ukraine may hold referendum on territories of Donetsk region, as well as news from the Munich Security Conference, in particular, about a new stage of peace talks this week.

ICU view: Despite a series of new media publications on the progress of peace talks between Ukraine and russia, the past week did not bring any new fundamental facts. Therefore, last week’s price increase was more a reflection of investors' drive to find positives in facts that have been known for quite some time.

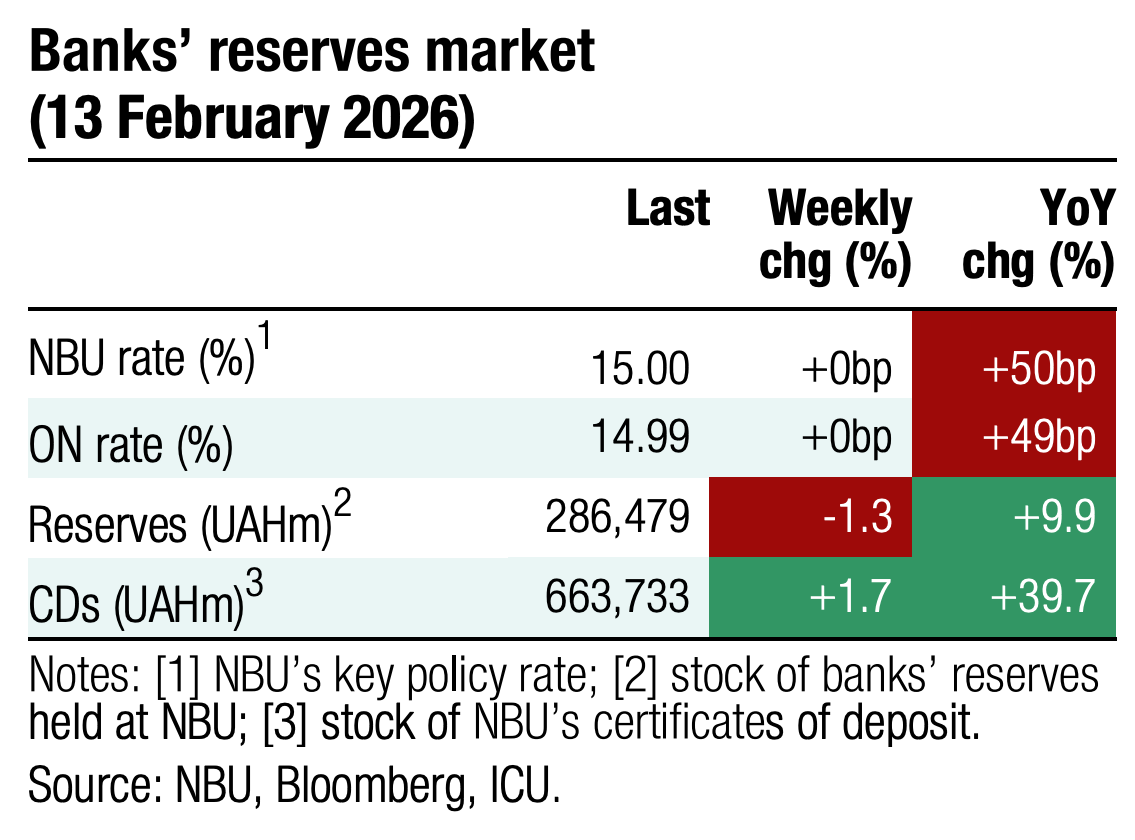

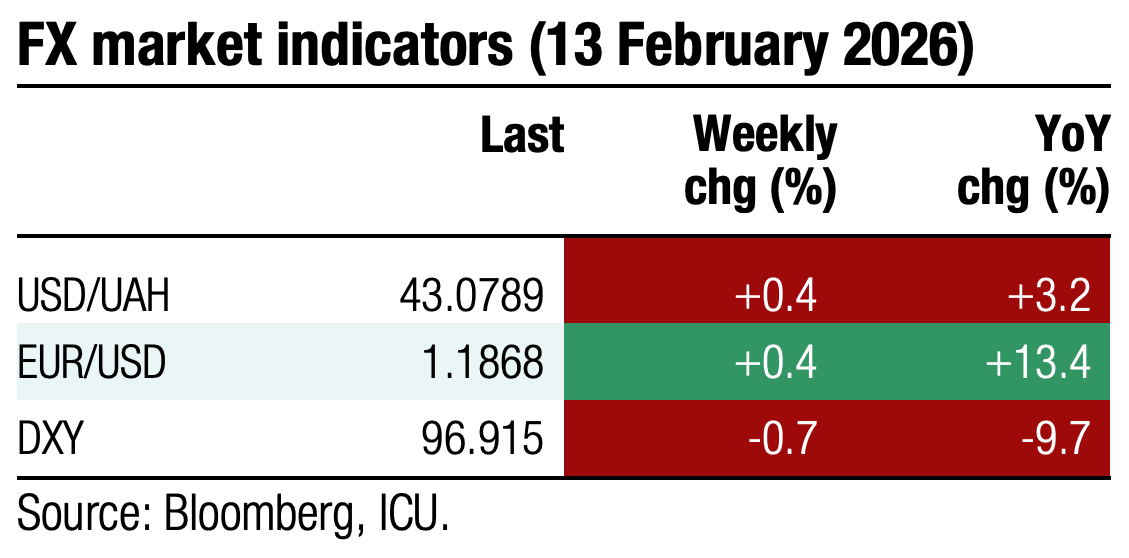

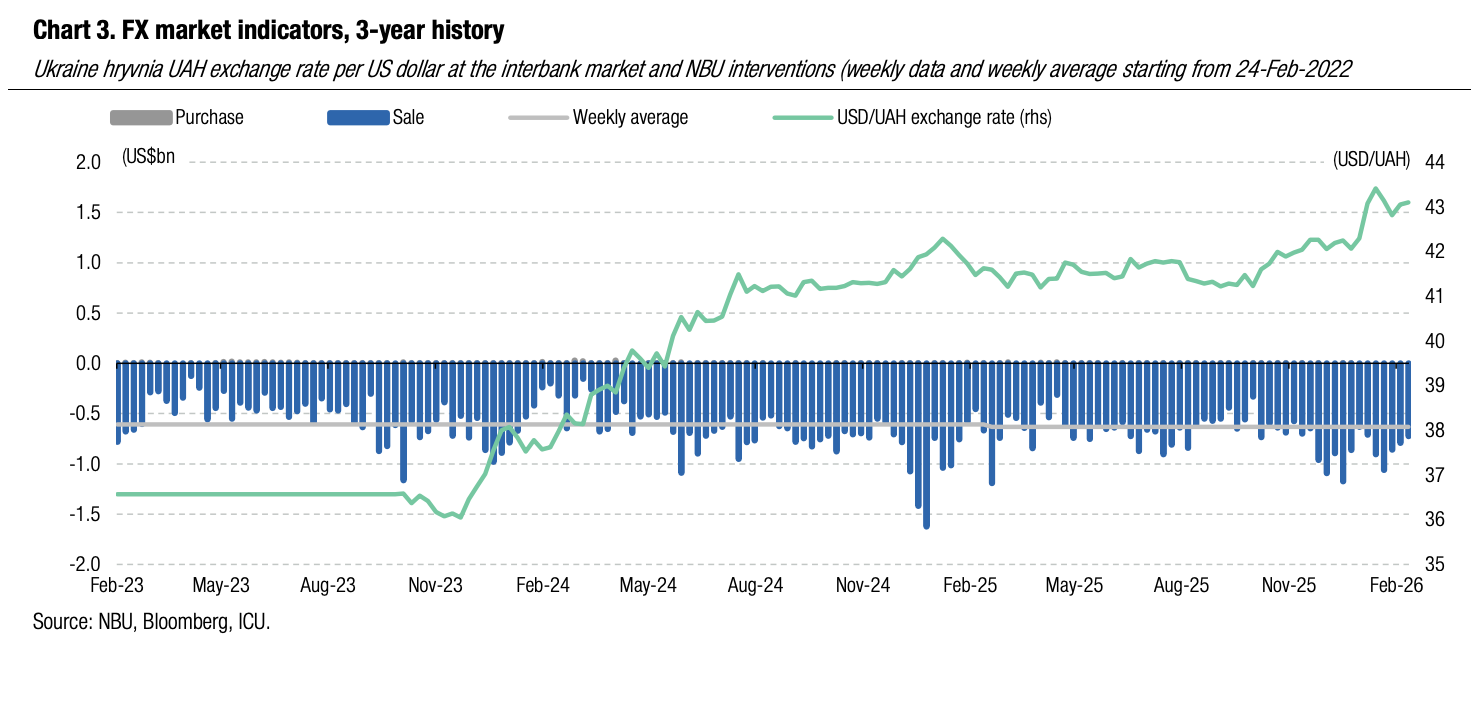

FX: NBU narrows the range of hryvnia fluctuations

NBU FX interventions last week were nearly flat, while the hryvnia exchange rate was kept in a very narrow range.

The hryvnia fluctuated in the range of UAH43-43.1/US$ last week. This implied a significant narrowing of the band from UAH0.35 a week before and UAH0.42-0.72 in the first weeks of the year. FX deficit in the market fell 15% WoW to UA$498m while the NBU reduced interventions by only 9% to US$726m.

ICU view: The NBU continued to actively cover excess demand last week, aiming to narrow the hryvnia volatility. The NBU is likely trying to calm the market to the extent possible after bumpy FX trends in January.

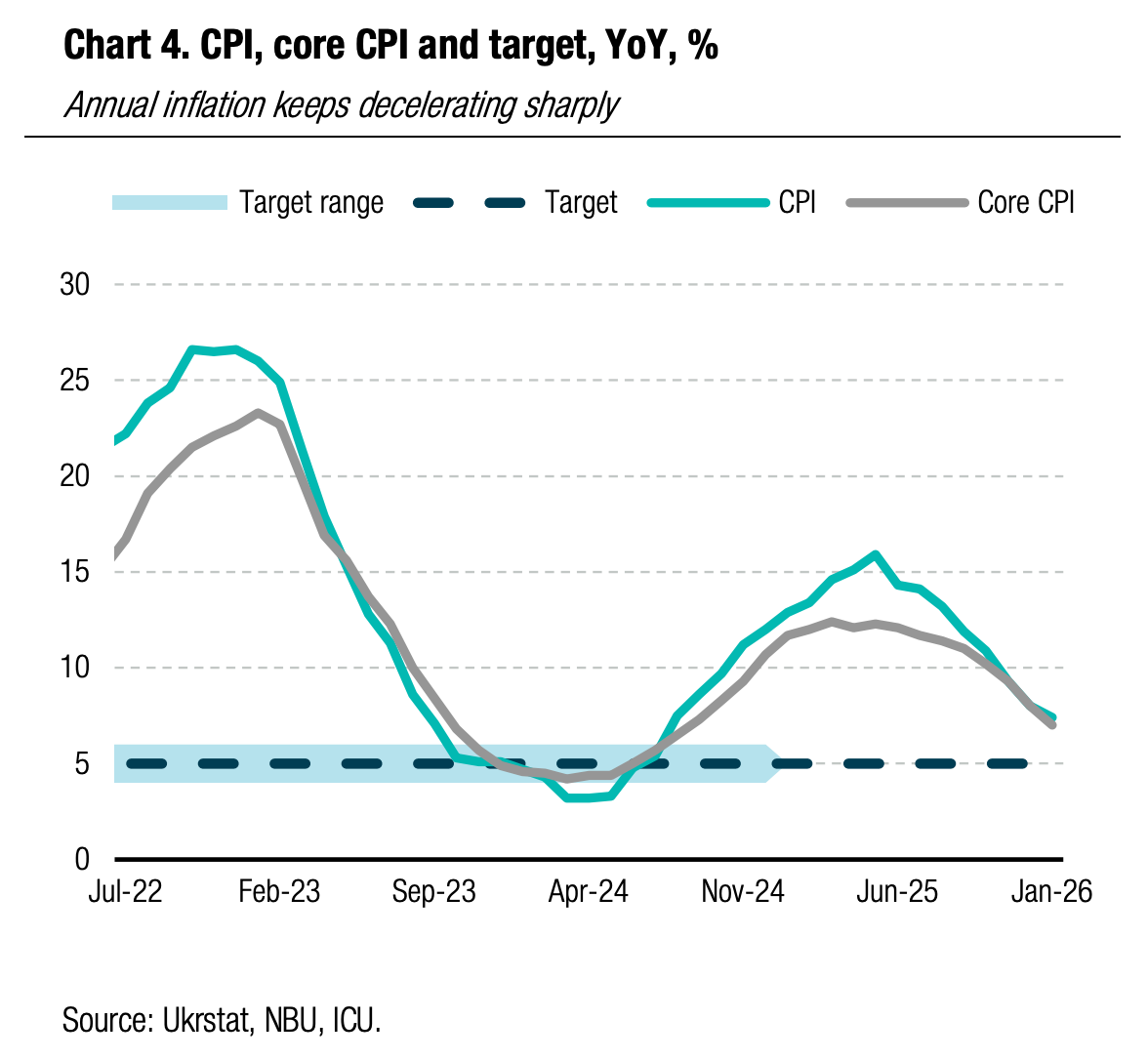

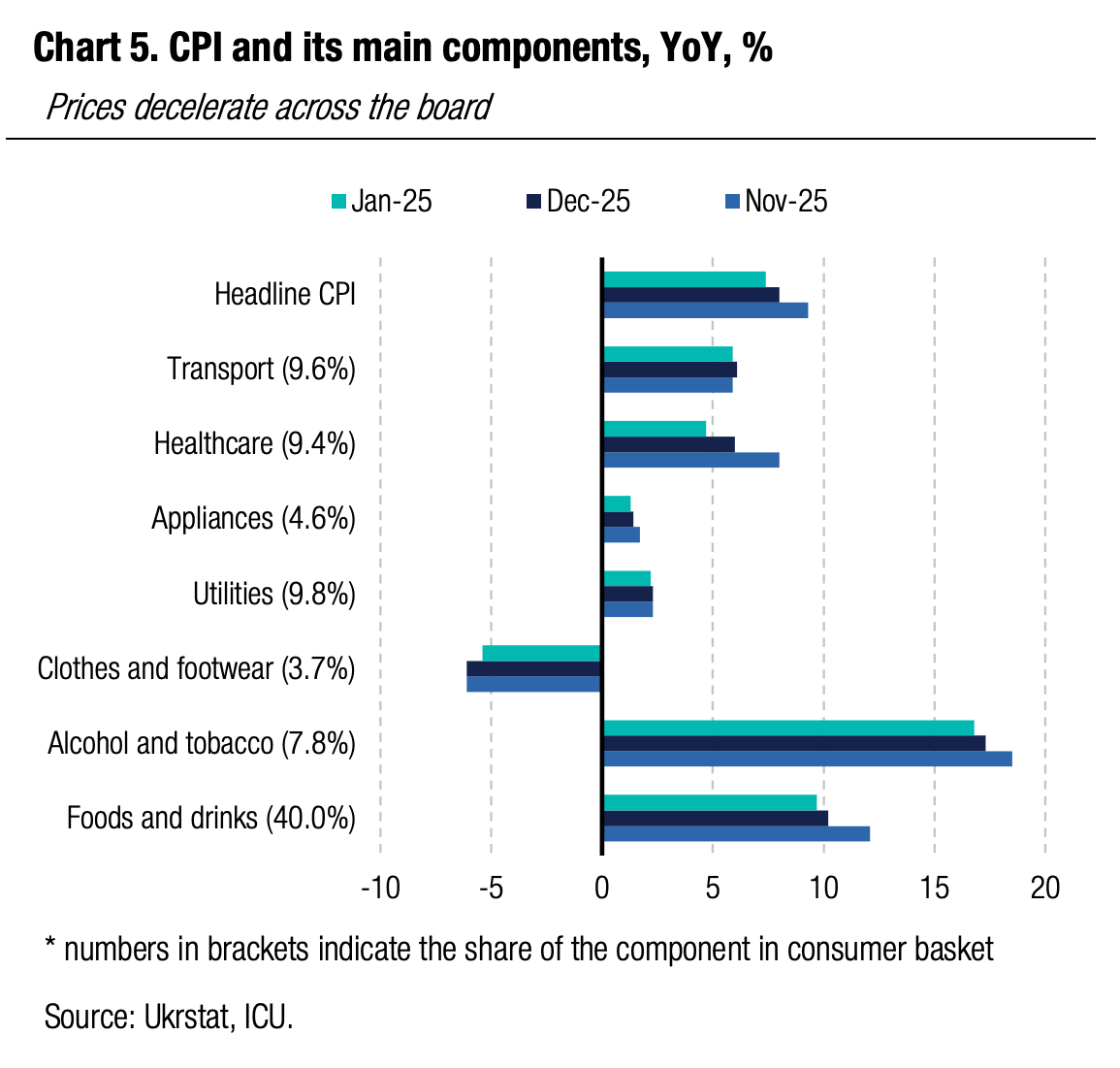

Economics: Disinflation trend robust

Annual headline CPI slowed to 7.4% in January from 8.0% in December.

Disinflation was visible across the majority of consumer basket categories with the steepest deceleration seen for communication services (7.1% YoY vs. 12.0% in December) and health services (4.7% vs. 6.0%). Prices for food, the largest component of the consumer basket, decelerated to 9.5% from 9.8% in December. Core inflation was down to 7.0% from 8.0% in December.

|  |

ICU view: The deceleration in annual consumer prices remains robust, and we expect the trend to continue at least until June before reversing in 2H26 on low base effects. We see end-2026 CPI at 6.3% YoY, below the NBU forecast of 7.5%. The supporting factors behind weakening inflationary pressures are slower growth in household incomes, the sufficiency of last year’s harvest, export constraints for food products (due to russia’s attacks on the port infrastructure), stability of regulated utility tariffs, and a broadly stable exchange rate so far. The extensive blackouts and higher electricity tariffs for businesses add to cost pressures. Yet, producers will be struggling to pass them onto consumers in full at least in the coming months due to weak consumer sentiment. With the above in mind, we believe the NBU will have room for more than two 50bp key rate cuts in 2026 (as projected in its recent Inflation report).