p>

Ukrainian bond market

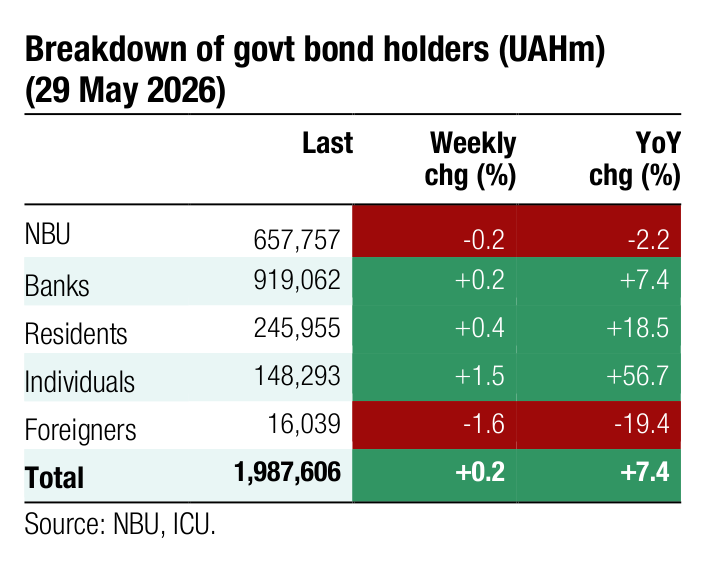

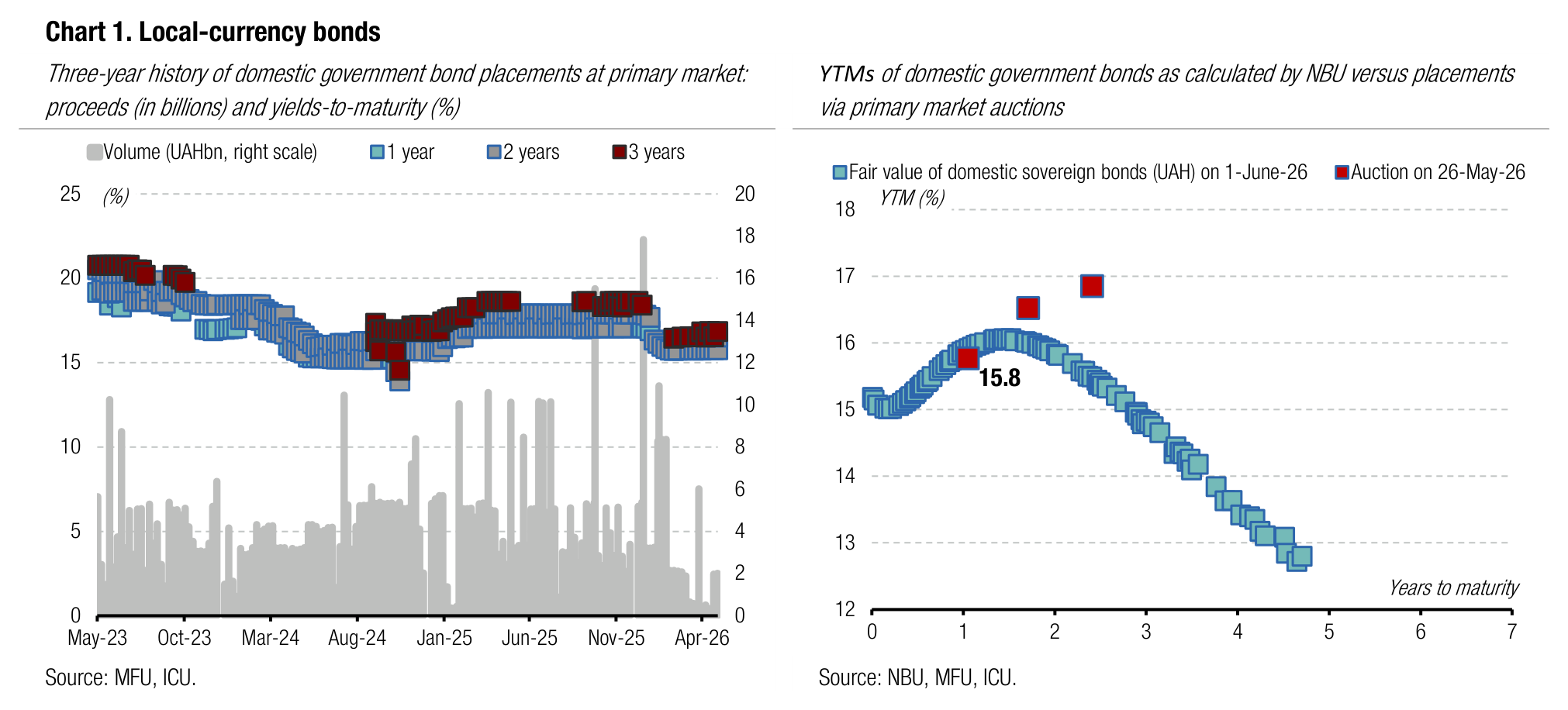

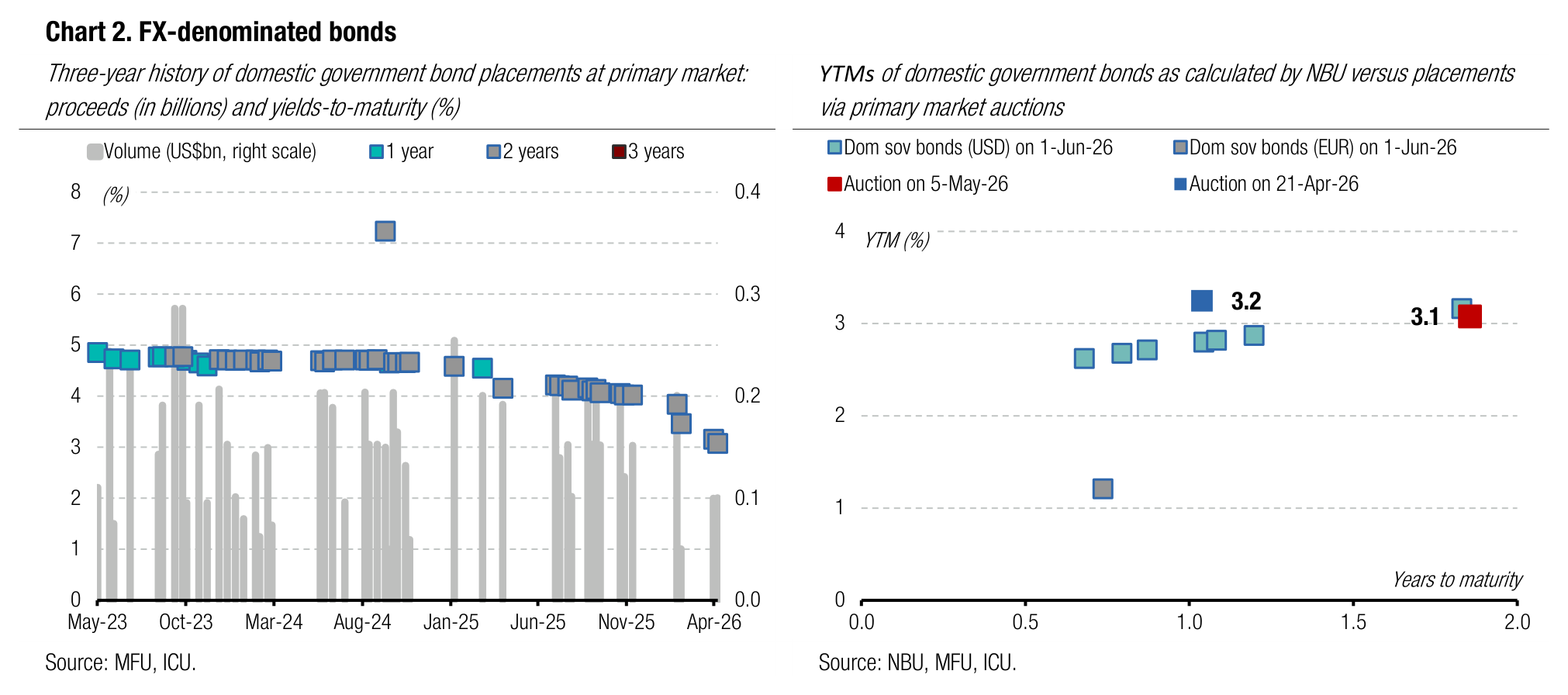

MoF slows down net borrowings

In May, the Ministry of Finance reduced domestic borrowings, and the domestic debt rollover ratio continued to trend down.

Last month, the MoF redeemed UAH31bn of UAH bonds, including UAH3.9bn of bonds due next week that were earlier exchanged for 2028 bills. There were no redemptions of FX- denominated bonds in May. At the same time, the ministry sold only UAH11.6bn of UAH bonds at primary auctions, including bonds issued for the exchange, and UA$100m of FX- denominated securities. Thus, the debt rollover in all currencies was just 51% in May.

All in all, net redemption of domestic debt in May was similar to April – slightly above UAH15bn for all currencies. In total, net borrowings stood at UAH13bn in 5M26.

In 5M26, domestic debt rollover decreased to 107% from 119% in 4M26. The rollover rate was 111% for hryvnia debt (132% in 4M26), 70% for debt in USD (55% in 4M26), and remained at 154% in EUR in the absence of both borrowings and repayments in this currency.

ICU view: The Ministry of Finance borrows domestically at a leisurely pace. It, thus, keeps reducing net borrowings that were relatively high at the beginning of the year due to a temporary decline in foreign aid inflows. Last week, the EU Council approved a EUR2.8bn tranche of the Ukraine Support Loan that will further strengthen the MoF's position and reduce the need for domestic borrowing. Therefore, we expect the Ministry of Finance to maintain the current rollover rate in June to reach 100% in 1H26. The MoF's further domestic debt market stance will depend on whether the budget is revised later this year to increase budget expenditures.

Foreign exchange market

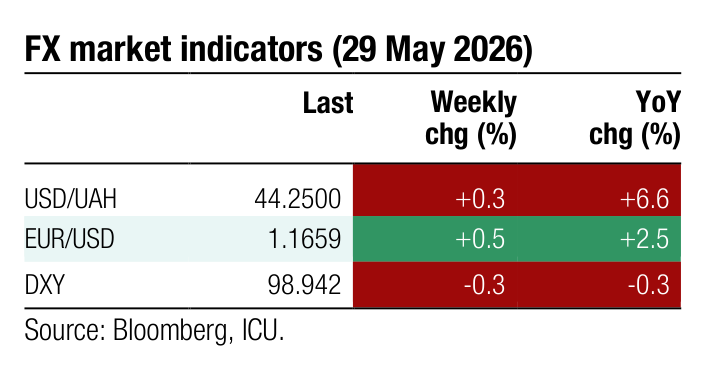

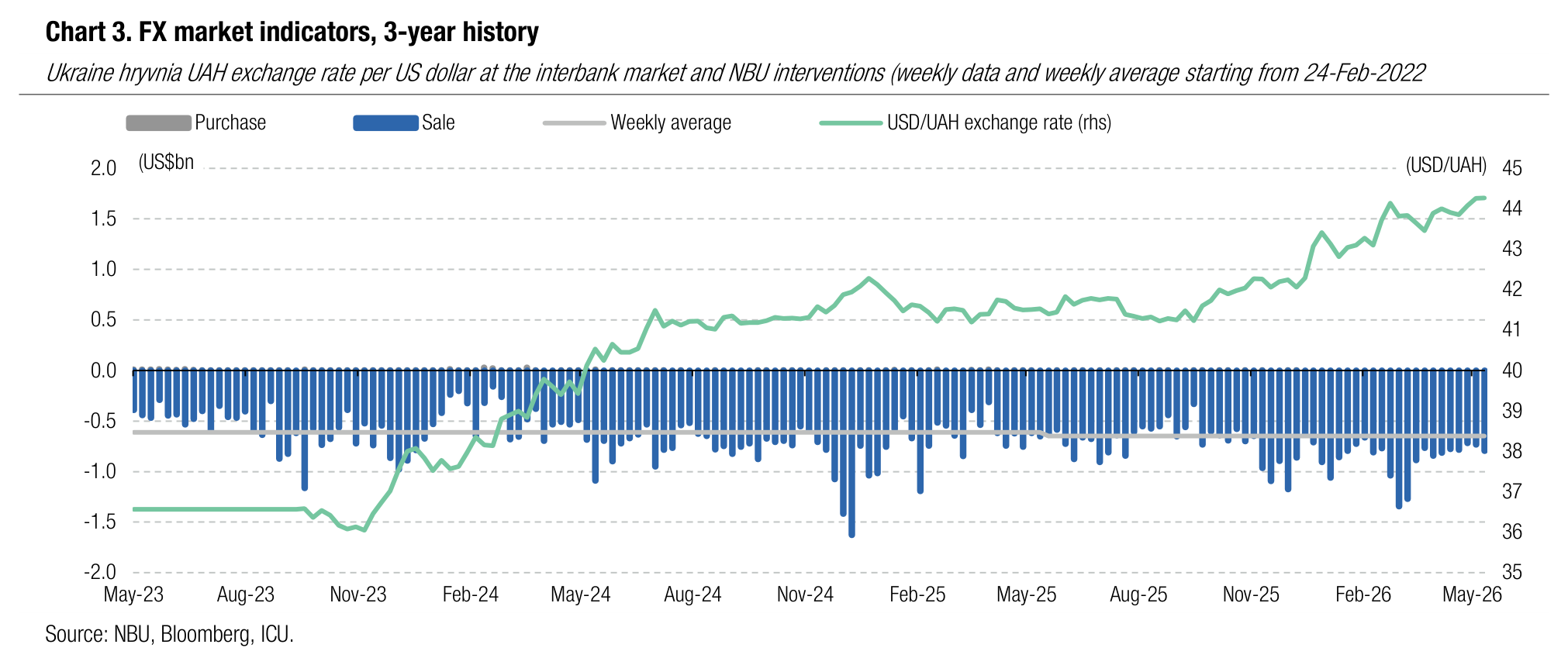

NBU stabilises hryvnia

The NBU did not allow the hryvnia to weaken significantly last week and kept it slightly below UAH44.3/US$.

The National Bank made some efforts to stabilise the hryvnia exchange rate at new levels and prevented it from weakening further beyond UAH44.3/US$. The official exchange rate fluctuated last week between UAH44.24/US$ and UAH44.3/US$ and was unchanged WoW.

The NBU increased interventions by 8% WoW to US$796m, against an insignificant, only 1%, increase WoW in the hard currency deficit in the FX market. In total, the NBU spent US$18.3bn for FX sale interventions YTD, a quarter more than in 5m25.

ICU view: The NBU continues to weaken the hryvnia gradually and allowed US dollar to move above the March highs in the second half of May. Yet, the NBU hit the brakes once hryvnia rate approached the highs from March. We expect in June the hryvnia will fluctuate near current levels, possibly without further weakening, at least in the coming weeks.

Economics

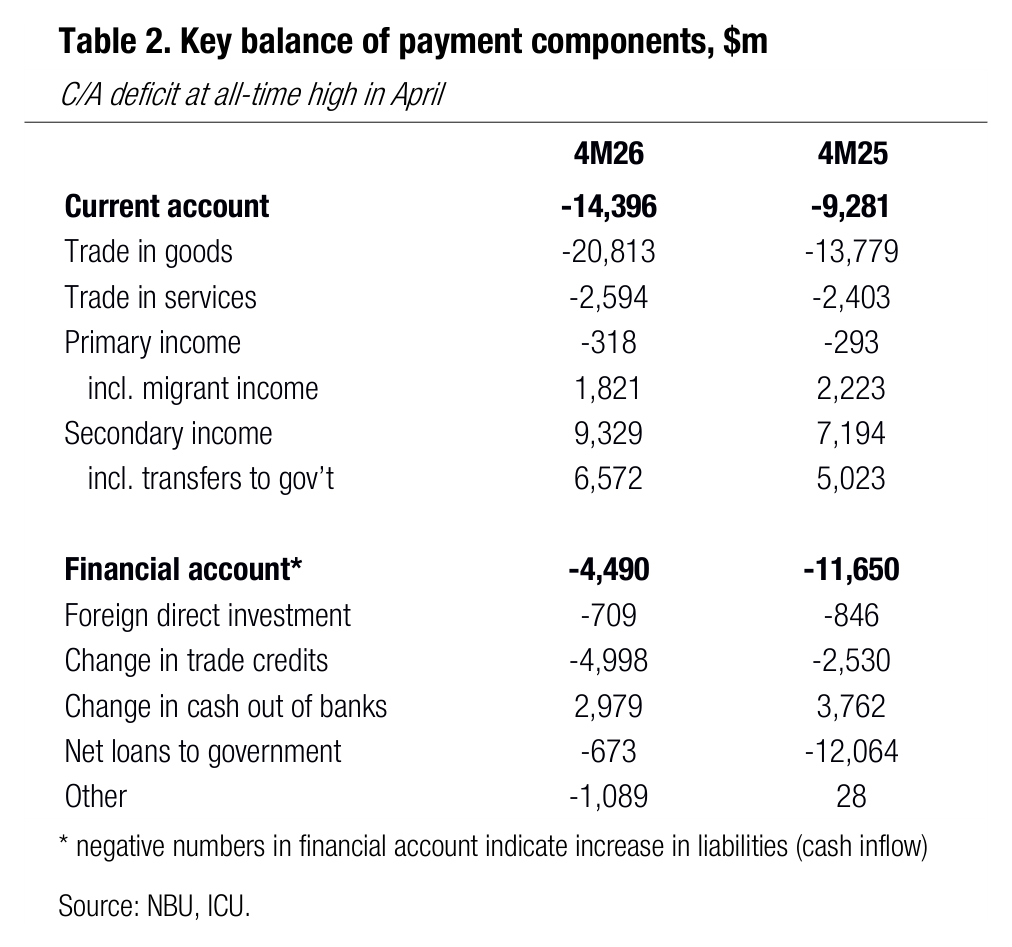

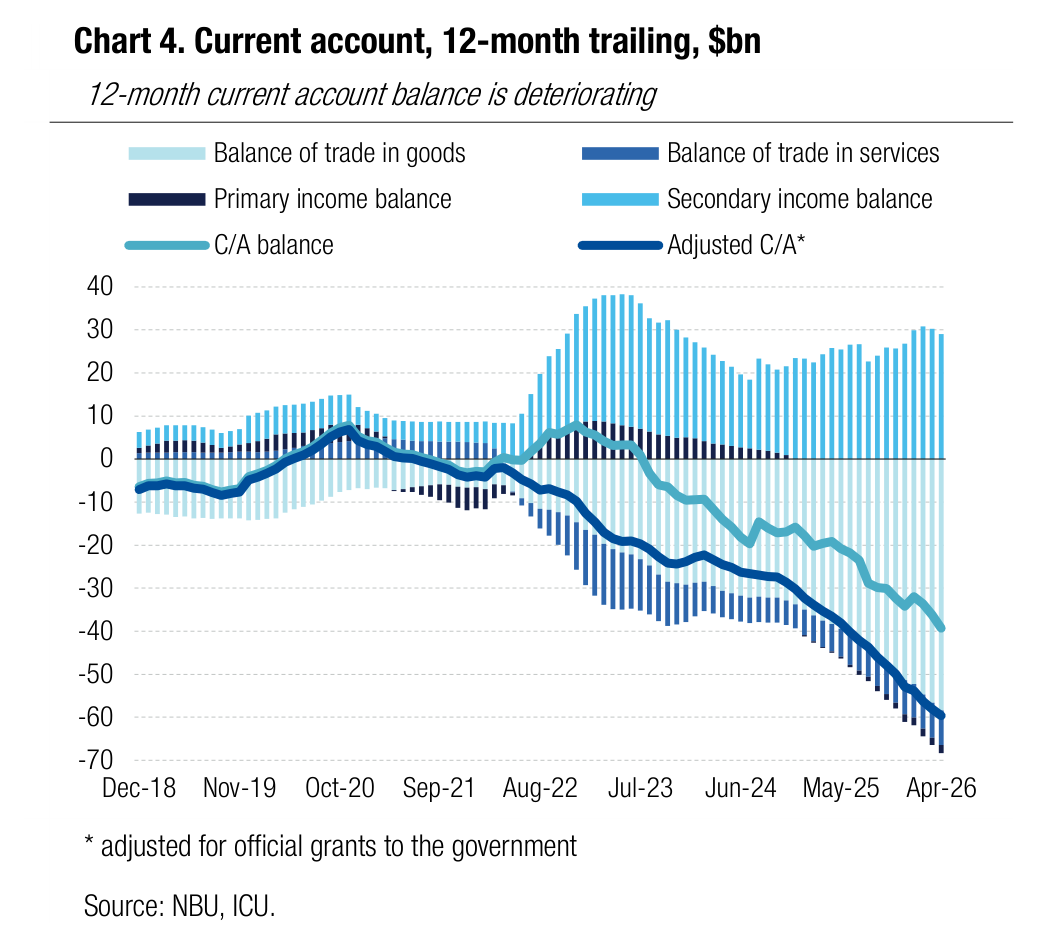

Current account deficit all-time high in April

Ukraine’s current account (C/A) deficit reached US$4.9bn in April and US$14.4bn 4M26 (vs US$9.3bn in 4M25) as the foreign trade-in-goods gap remains ample.

The trade-in-goods deficit far exceeds last year’s numbers as imports surged 29% while exports were only up by 4% in 4M26. Meanwhile, the deficit of trade in services is little changed from 4M25 with the gap largely shaped by expenditures of Ukrainian refugees abroad that are classified as import of tourism. Migrant incomes (a component of primary income) continue to decline and were down by a fifth in yearly terms. The secondary income surplus is helped by the inflow of ERA facility that is classified as a grant.

The financial account balance was positive even though the inflows of concessional loans to the government were largely symbolic at less than US$0.7bn. The reduction in trade credits remains the major source of FX inflows via the financial account. The outflow of FX cash out of the banking system, the largest channel for capital outflow via the financial account, was down 1/5 YoY.

Net capital inflows via the financial account fell significantly short of the C/A deficit, implying pressure on NBU reserves that were down 16% in 4M26 to US$48.2bn.

ICU view: Approval of the Ukraine Support Loan by the EU implies Ukraine is set to receive enough external funding in 2026 to offset the imbalance of external accounts. An all-time-high current account deficit (excluding budgetary grants) doesn’t pose any immediate threats to macroeconomic stability, but this risk will loom over the economy going forward.