|  |

|  |

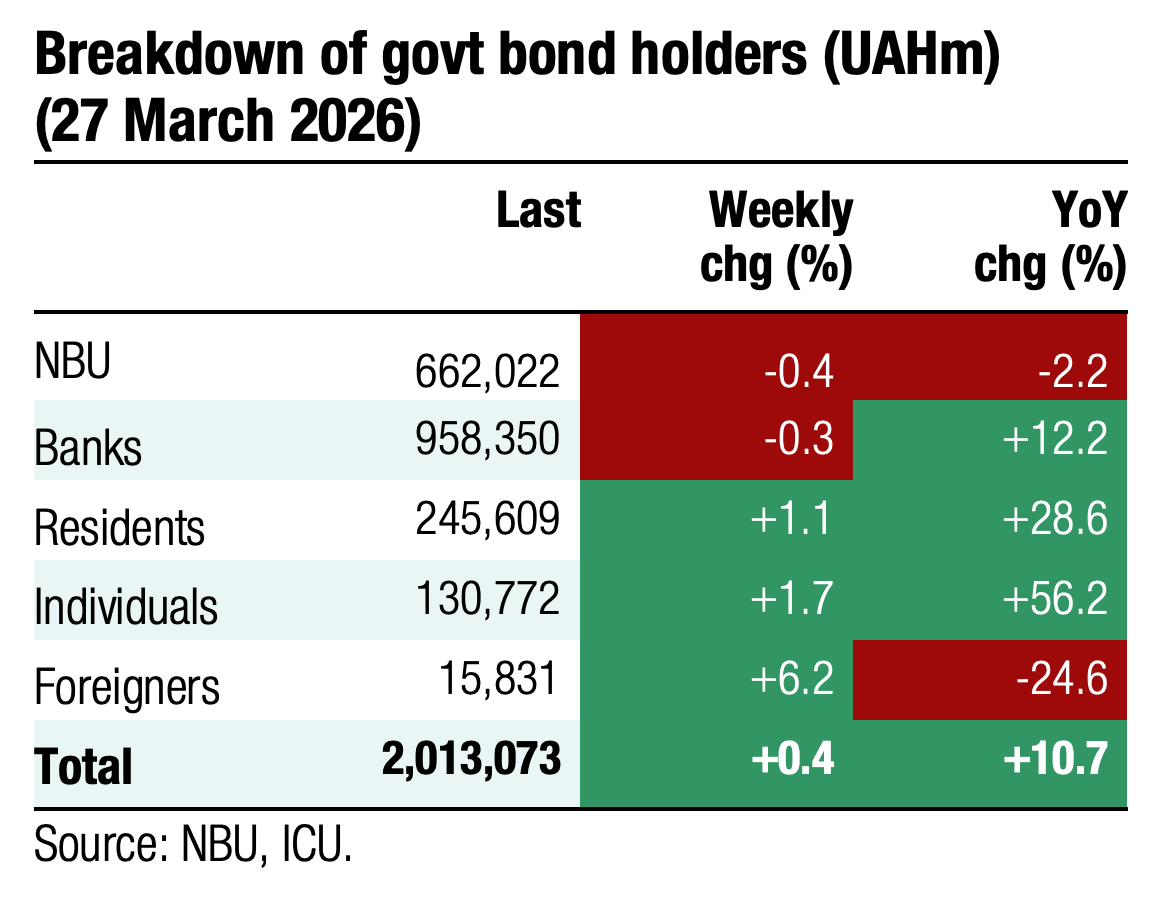

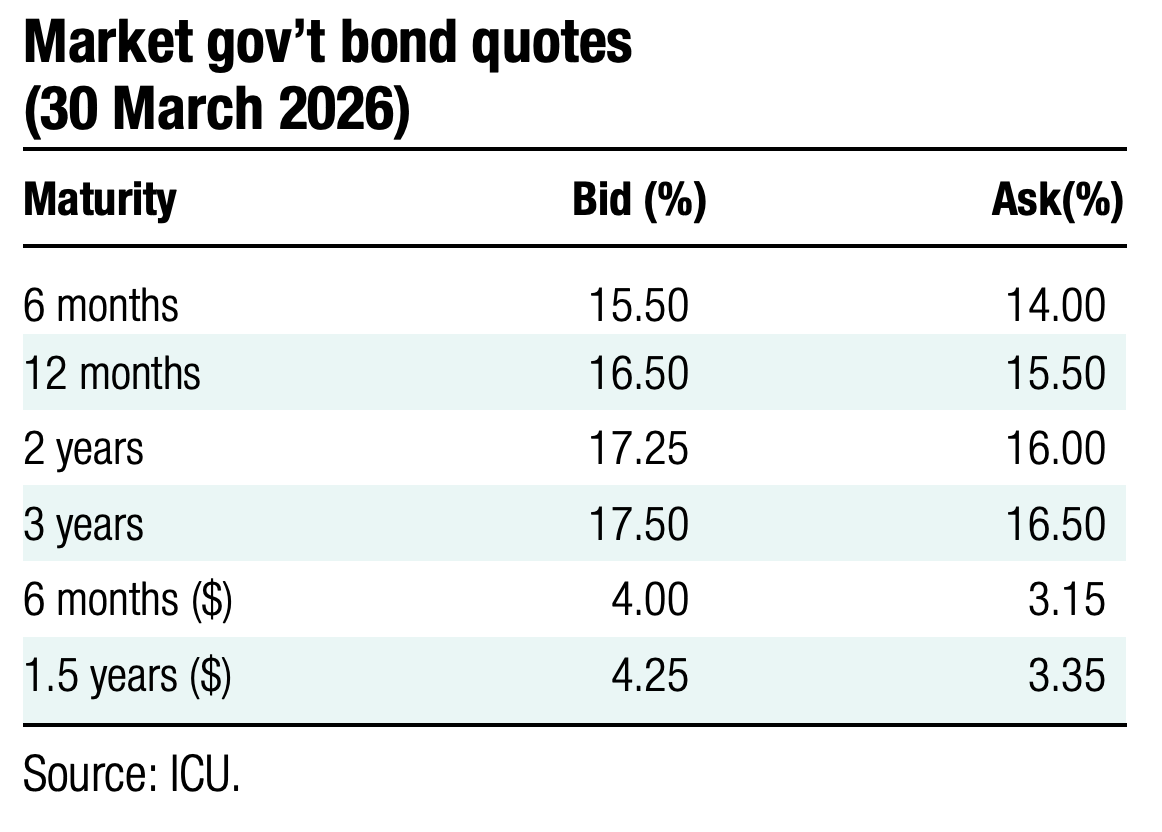

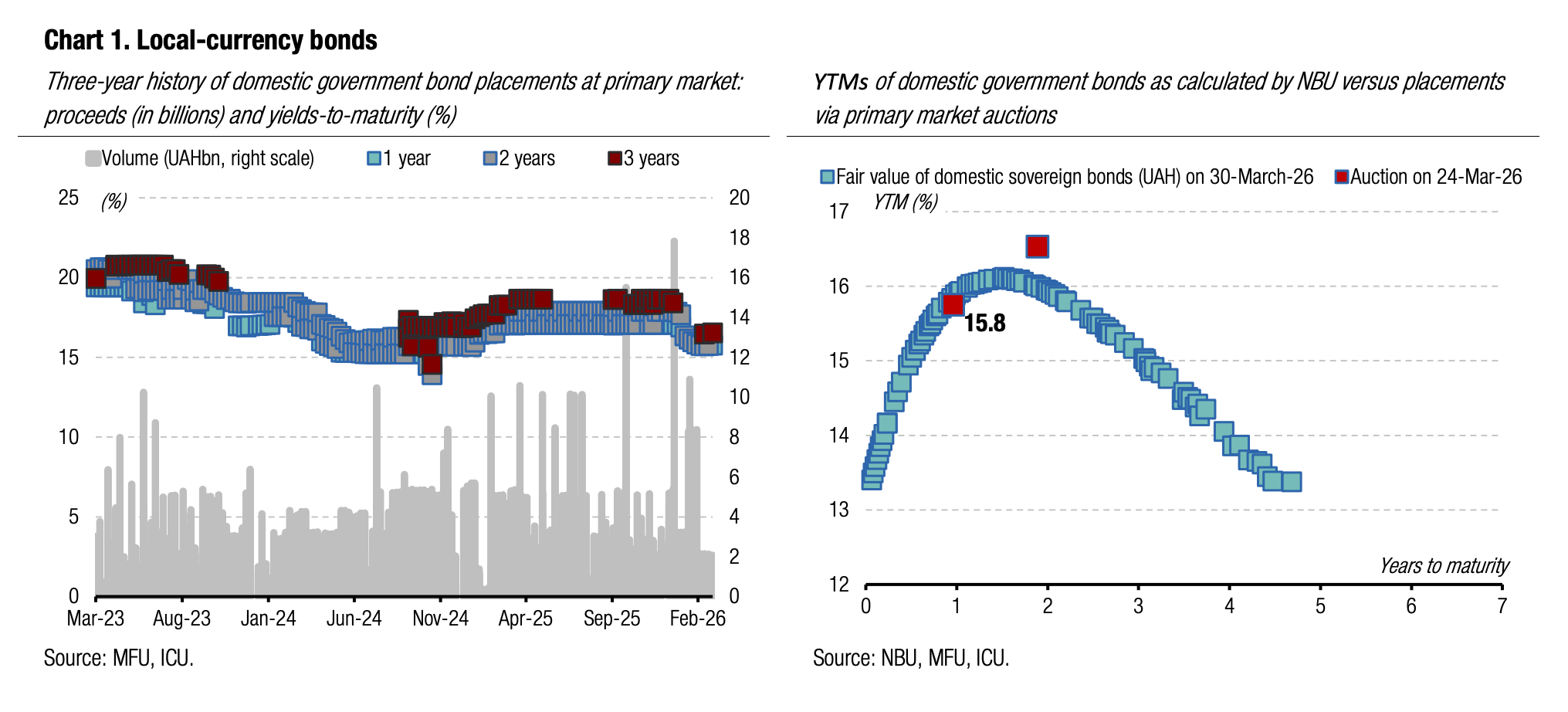

Bonds: Yields of government bonds stabilise

At the primary auction last Tuesday, the cut-off rates did not drop for the first time in two months. On the contrary, the weighted average yields increased and nearly reached the cut-off rates.

Demand for UAH bonds was low last week. The volume of bids for a one-year military paper was below supply, and the bid-to-cover ratio for the two-year security was just 1.1x. The MoF refused to increase the yield of the one-year instrument and maintained the 15.15% cut-off rate, with the weighted average yield rising by 1bp to 15.13%. The cut-off rate for two-year paper remained at 15.87%, the same as two weeks ago. However, the weighted-average rate increased by 7bp to 15.85%. See details in the auction review.

Thus, the cut-off rate for the one-year security remains unchanged for the third week, and the weighted average rate is currently only 2bp below. Similarly, the yield on the two-year instrument is now 2bp lower than the cut-off rate.

Also, last Wednesday, the MoF held a swap auction, offering to exchange a bill maturing in a month for a new three-year note. All bids came in exclusively at the cut-off level of the previous regular auction, so both the cut-off rate and the weighted average rate were set at 16.15%.

ICU view: The NBU's decision to keep the key policy rate helped stabilise interest rates in the primary market. The volume of bids with yields below the cut-off rates may decrease, and yields will likely stabilise at the current levels. Rates may remain unchanged in the coming months until preconditions for further monetary policy easing reappear. In its communication following the Monetary Policy Committee meeting, the NBU noted that the key policy rate may rise should risks rise. However, in the current environment, we do not anticipate an increase in UAH bond yields in the near future.

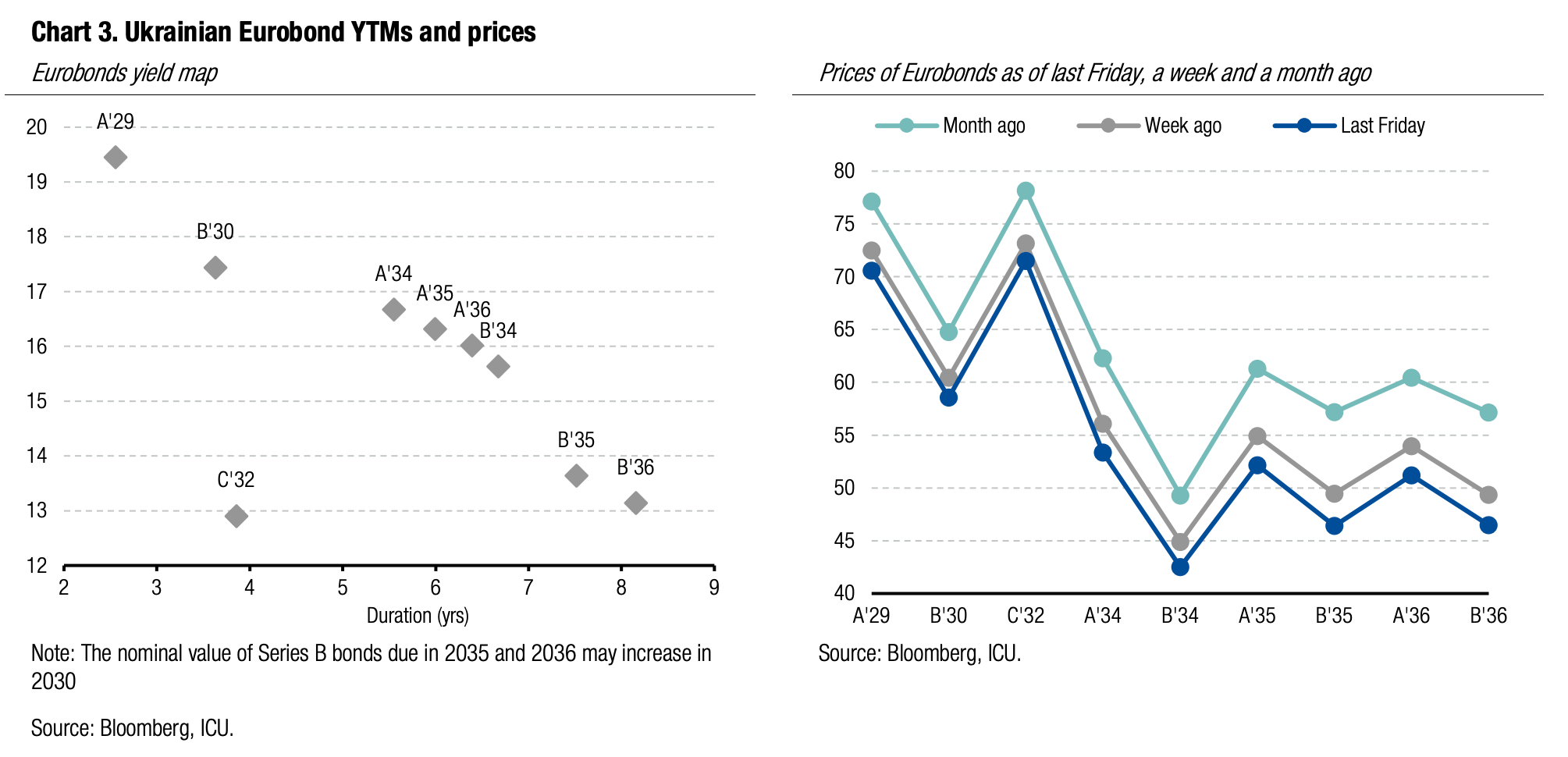

Bonds: Eurobonds fall on global turbulence

Ukrainian Eurobond prices continued to fall last week following deterioration of global sentiment towards emerging markets.

Since the war in Iran started, global sentiment towards emerging markets has gradually deteriorated. The EMBI index fell by more than 4%. The long pause in US-moderated peace talks between Ukraine and russia added even more fuel, and resulted in an almost 14% drop in Ukrainian Eurobond prices since the beginning of March. Another negative contributor was the delay with EU funding due to Hungary’s veto and slow reform progress in Ukraine.

ICU view: Ukraine Eurobond holders see less and less reason for optimism with regard to a likely peace deal. Due to a prolonged war in Iran, the prospect of resuming trilateral talks is becoming increasingly illusory. The deterioration in global sentiment towards emerging markets will continue to add more pressure on Ukrainian Eurobonds.

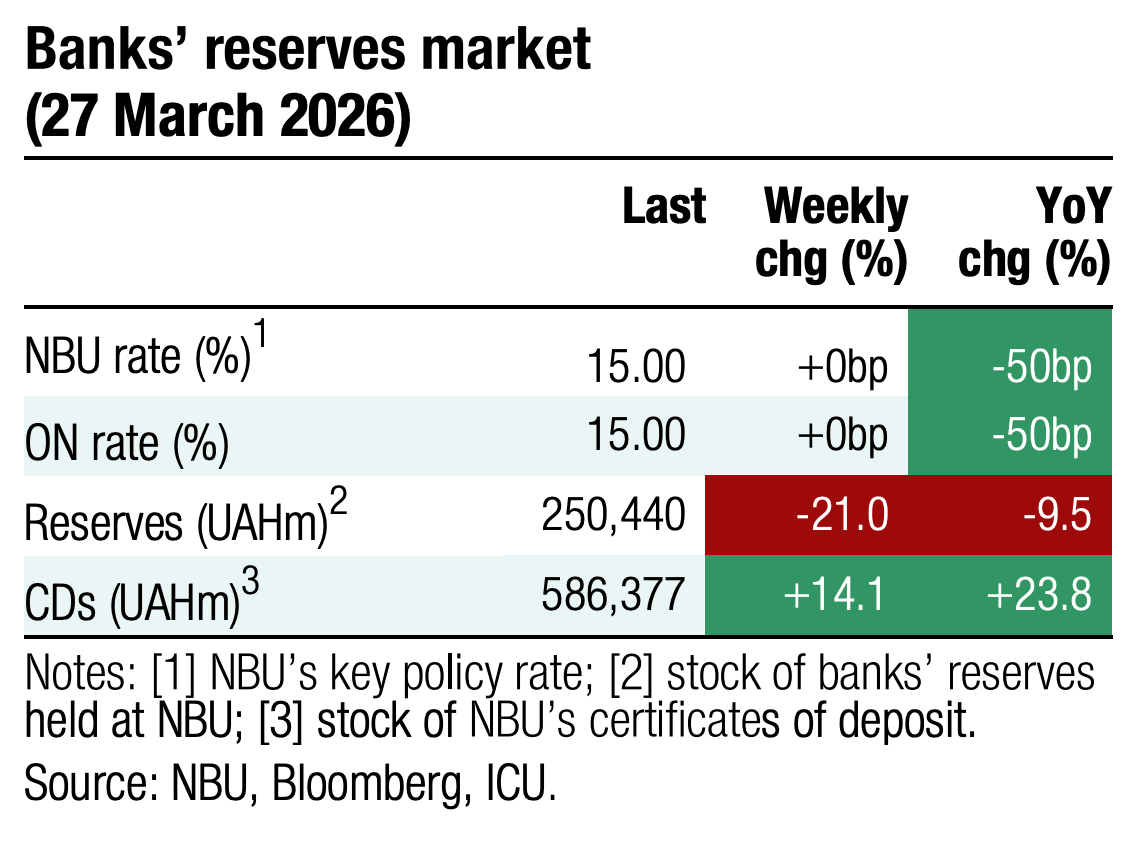

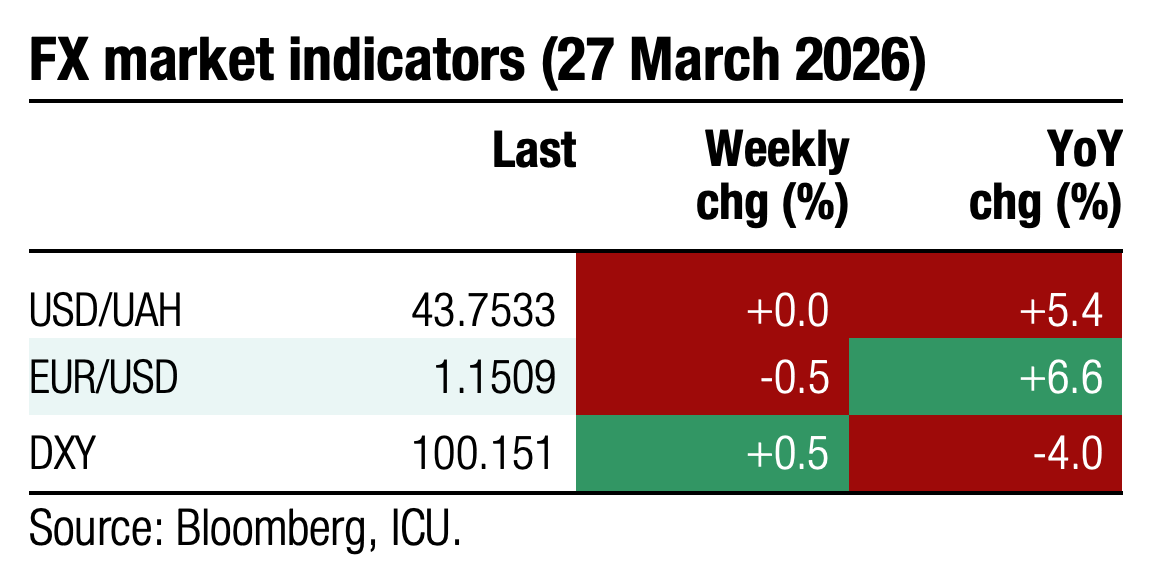

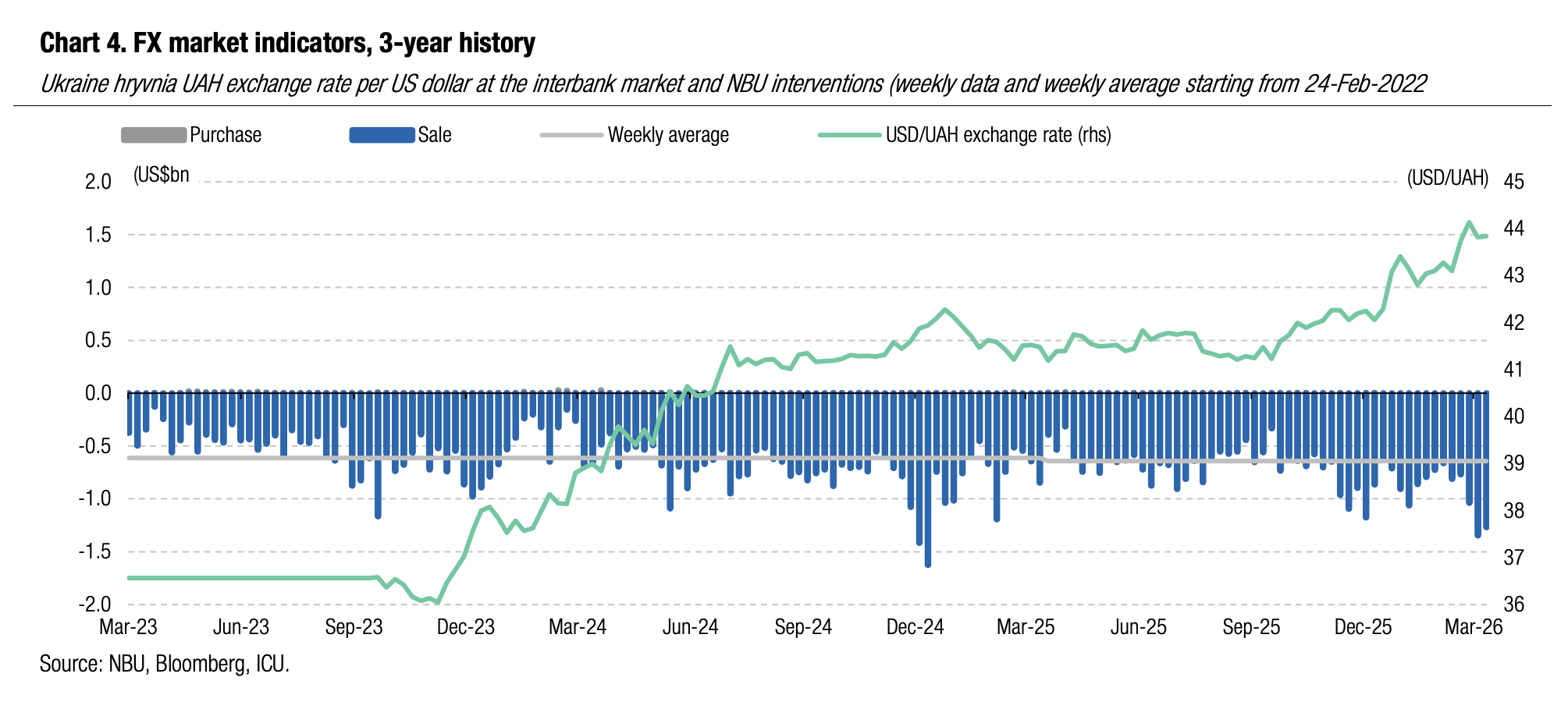

Bonds: NBU keeps interventions high

The NBU’s interventions last week were almost unchanged as it sought to satisfy growing FX demand.

The foreign currency shortage stayed high above US$0.9bn. The key factor was a 14% WoW (to US$1.8bn) increase in FX purchases by bank clients (legal entities) in the market. At the same time, the sale of hard currency by bank clients was low, resulting in a net purchase of US$0.8 bn, up 17% WoW.

The retail segment reacted positively to the NBU's determination to keep the hryvnia exchange rate below UAH44/US$. Net purchases of foreign currency by households almost halved to US$128m over four business days.

All in, the NBU had to sell almost US$1.3bn, down 6% WoW.

ICU view: The stabilisation of the exchange rate helped reduce anxiety among the population leading to a 1/5 reduction in foreign currency purchases. However, imbalances in the interbank FX market only deepened, as demand from oil-product importers, who need more funds to purchase motor fuel abroad, was likely supplemented with demand from state institutions that need FX for defence goods.