|  |  |

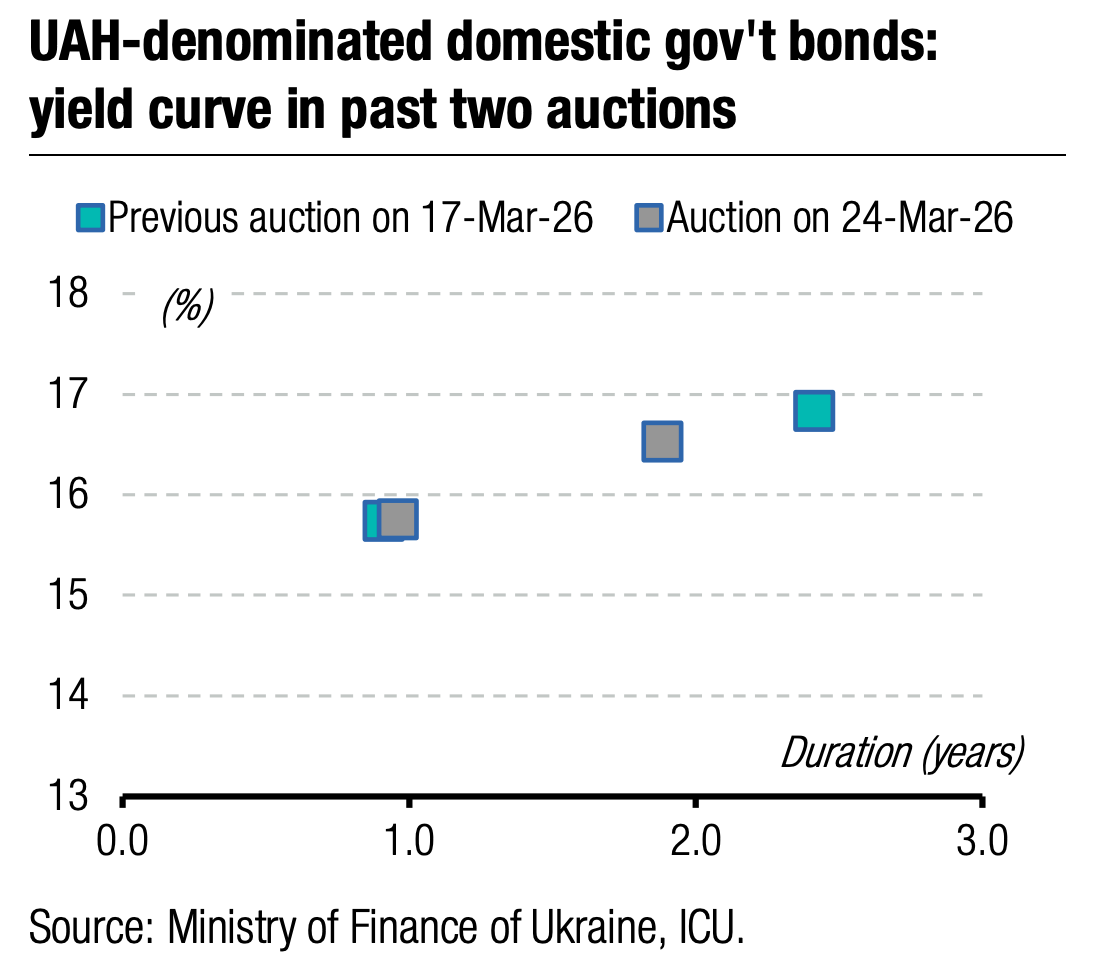

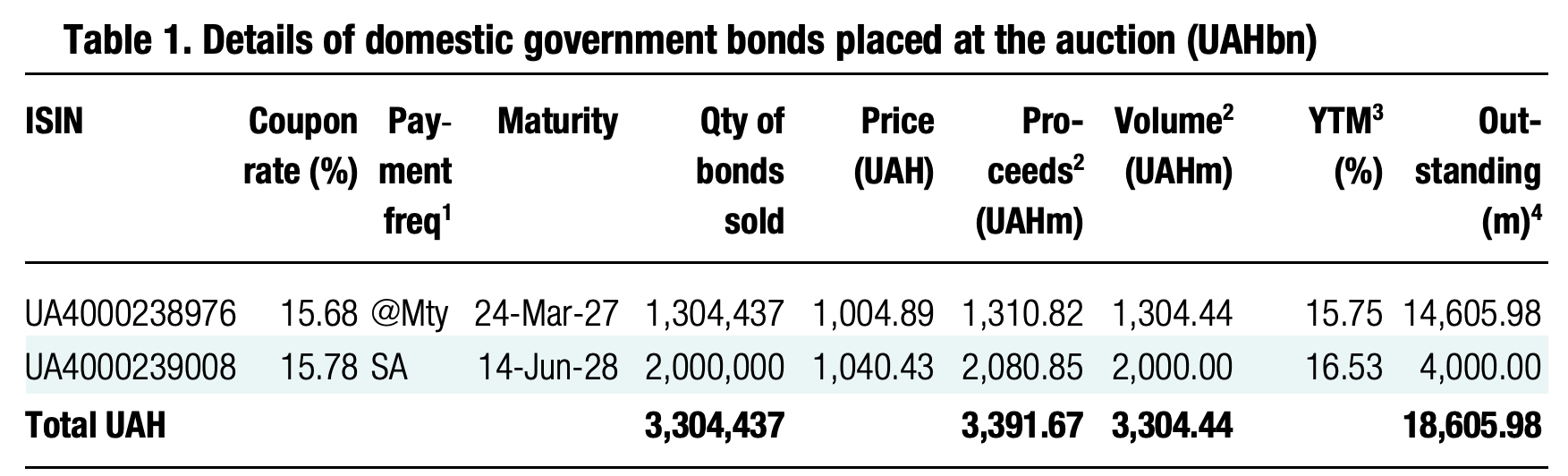

Yesterday's auction saw the first material increase in weighted average yields this year, which came as close as possible to the cut-off rates.

For the second time in a row, demand for one-year military bills was lower than supply, but there were already two bids above the cut-off rate of previous auctions. Therefore, the MoF rejected them, selling only UAH1.3bn of bills. The cut-off rate remained at 15.15%, the same as the two previous auctions. At the same time, the weighted average yield increased by another 1bp to 15.13%, and is now only 2bp below the cut-off rate.

Note: [1] payment frequency abbreviations: M - monthly, Qtly - quarterly, SA - semi-annually, @Mty - at maturity date; [2] proceeds and volumes for the USD-denominated bonds are calculated based on the previous day's exchange rate 43.91/USD, 50.95/EUR; [3] yields on coupon-bearing bonds are effective yields to maturity. Sources: Ministry of Finance of Ukraine, Bloomberg, ICU.

The placement of two-year securities was even more interesting. The minimum rate in bids increased by 10bp to 15.6%, and the maximum bid rate decreased by 24bp to 15.9%. However, since demand exceeded supply by 10%, the ministry satisfied all non-competitive demand at the weighted-average rate and most competitive bids at their yields up to 15.87%, unchanged from the auction two weeks ago. At the same time, the weighted average rate increased by 7bp to 15.85%, and is now also only 2bp below the cut-off rate.

Currently, the decline in yields has paused, which may last for at least a few weeks. The NBU will not rush to lower the key policy rate, so the potential opportunity for the Ministry of Finance to reduce yields has now been exhausted. In a few weeks, we can see demand consolidate at the cut-off rate, where it will stay until expectations of a reduction in the NBU discount rate again reach critical mass.

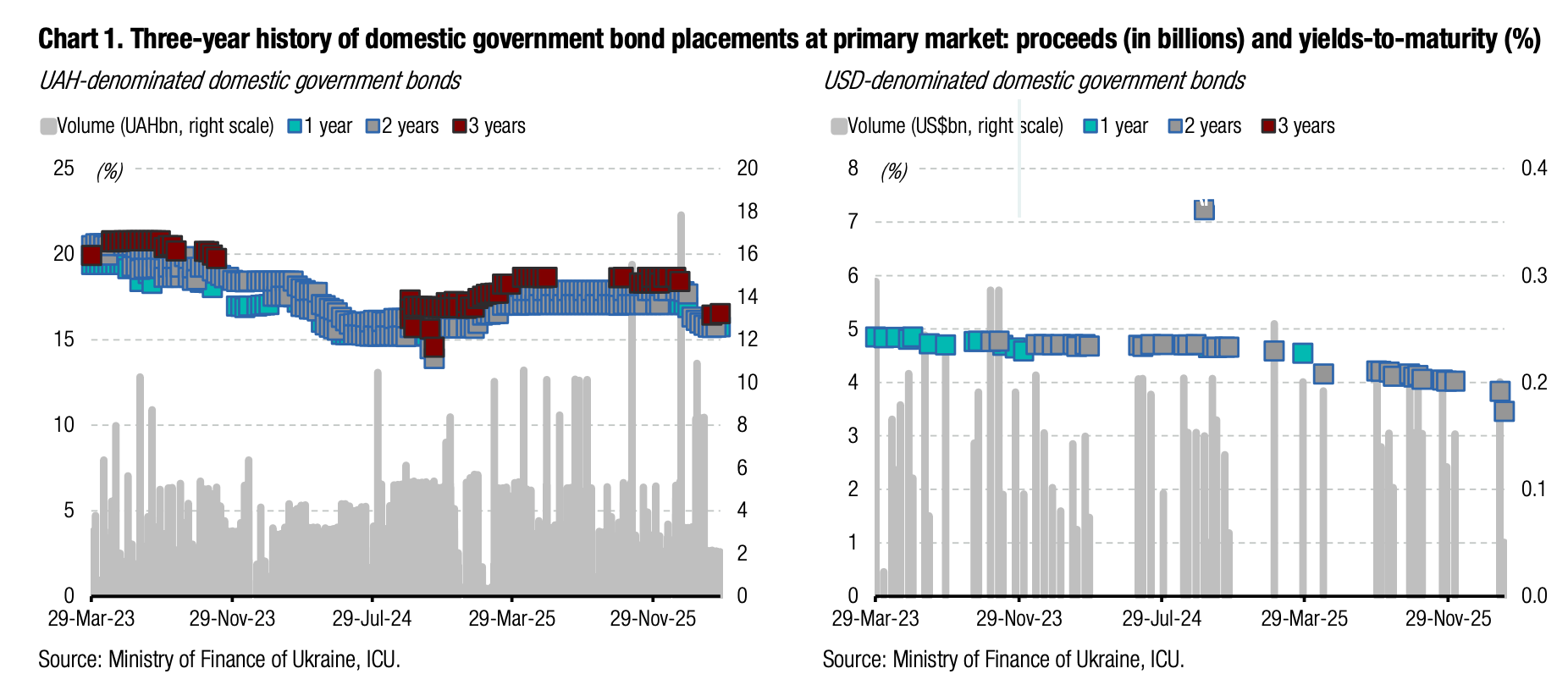

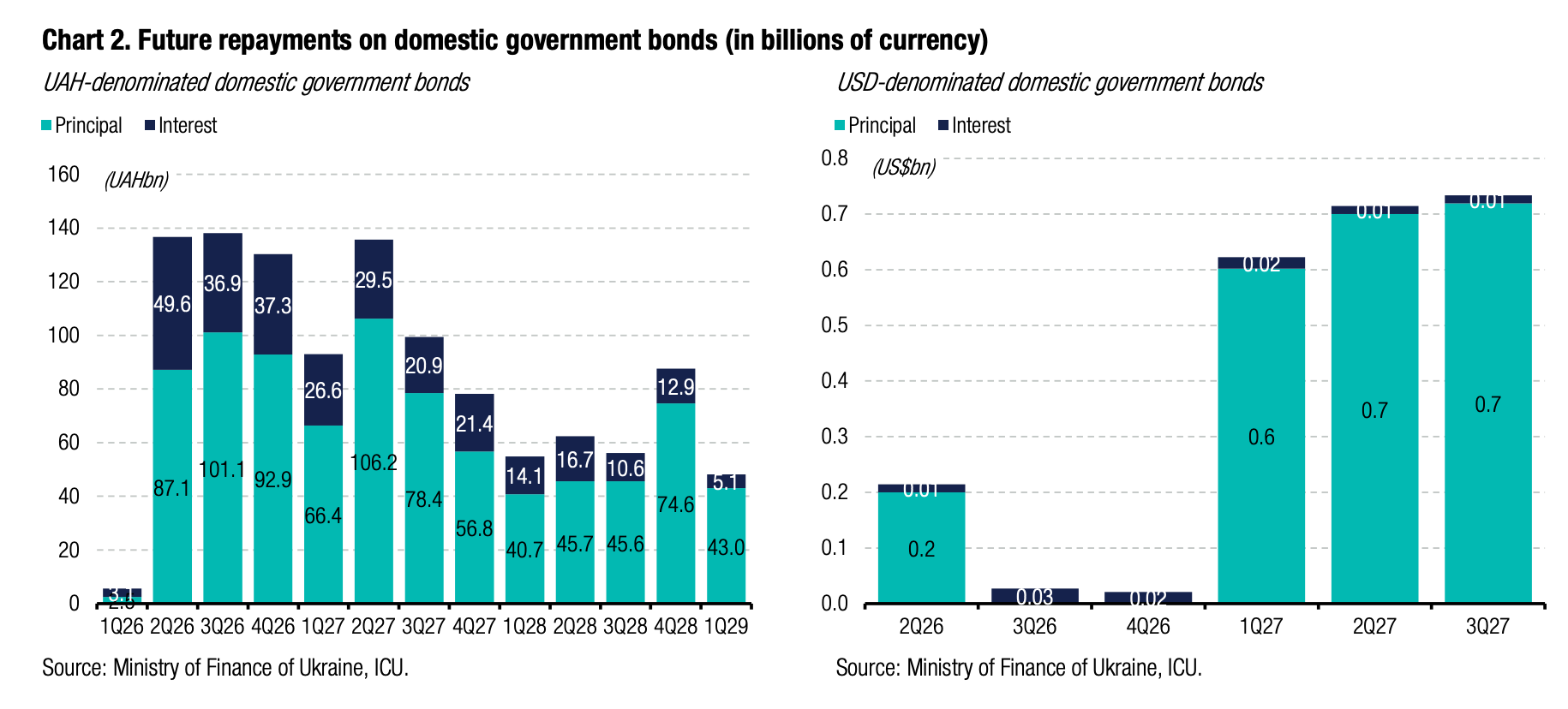

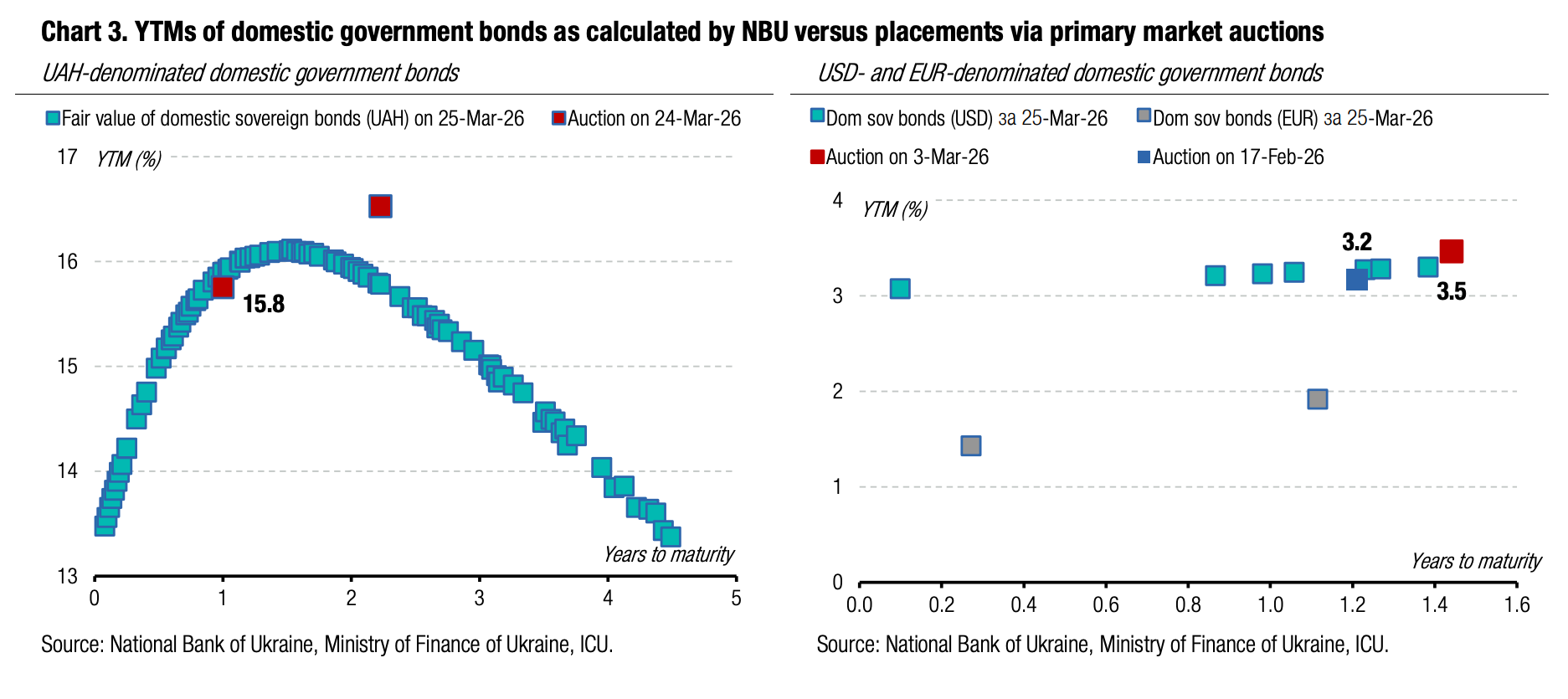

Appendix: Yields-to-maturity, repayments