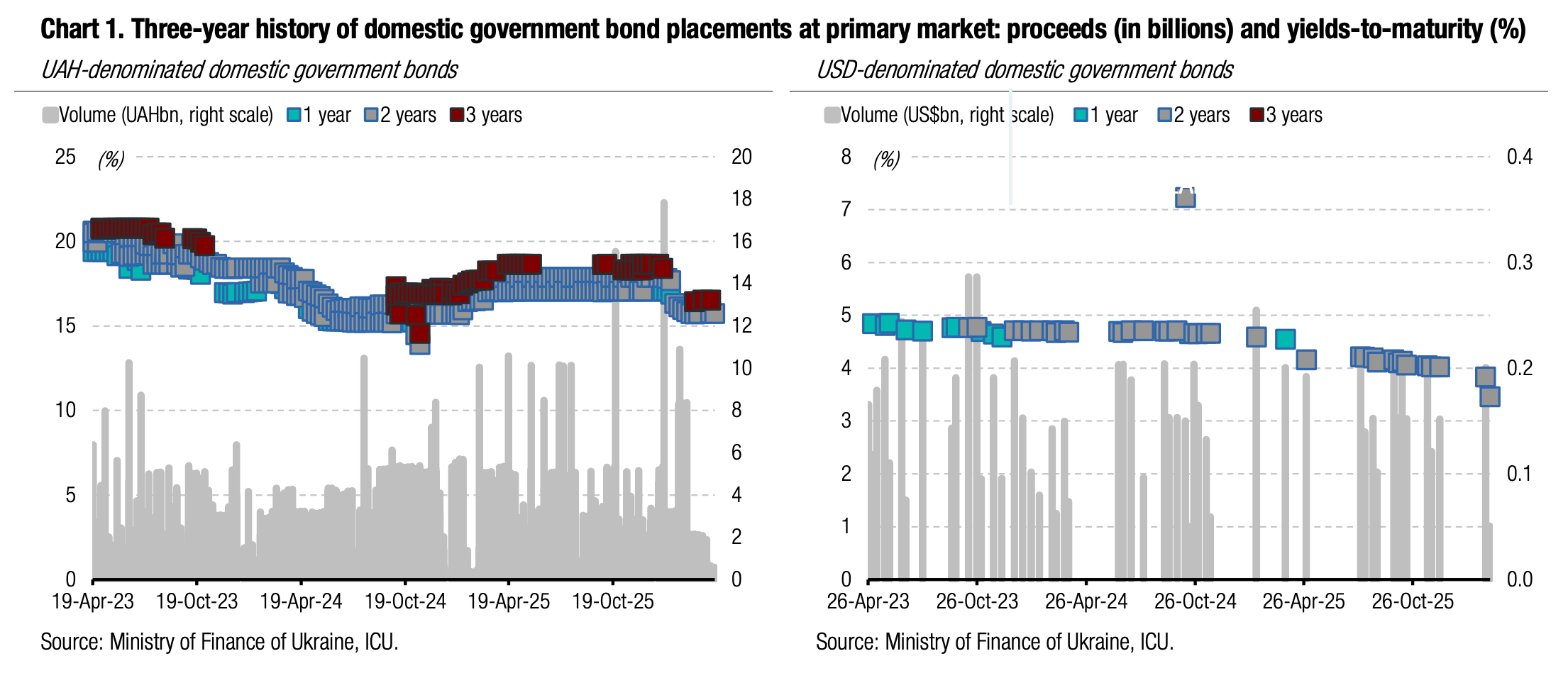

|  |  |

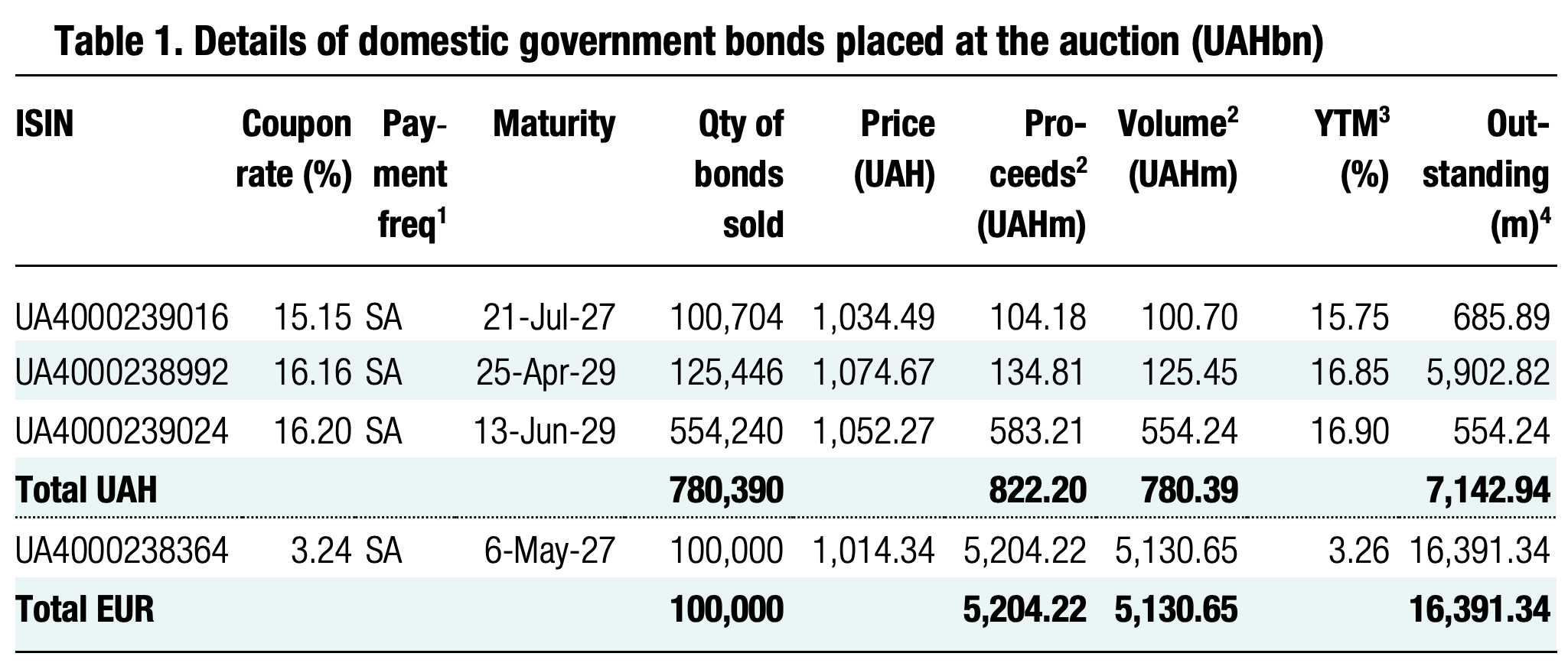

Yesterday, the Ministry of Finance launched a new three-year UAH instrument, but it did not attract significant demand. Only bonds in euros were oversubscribed.

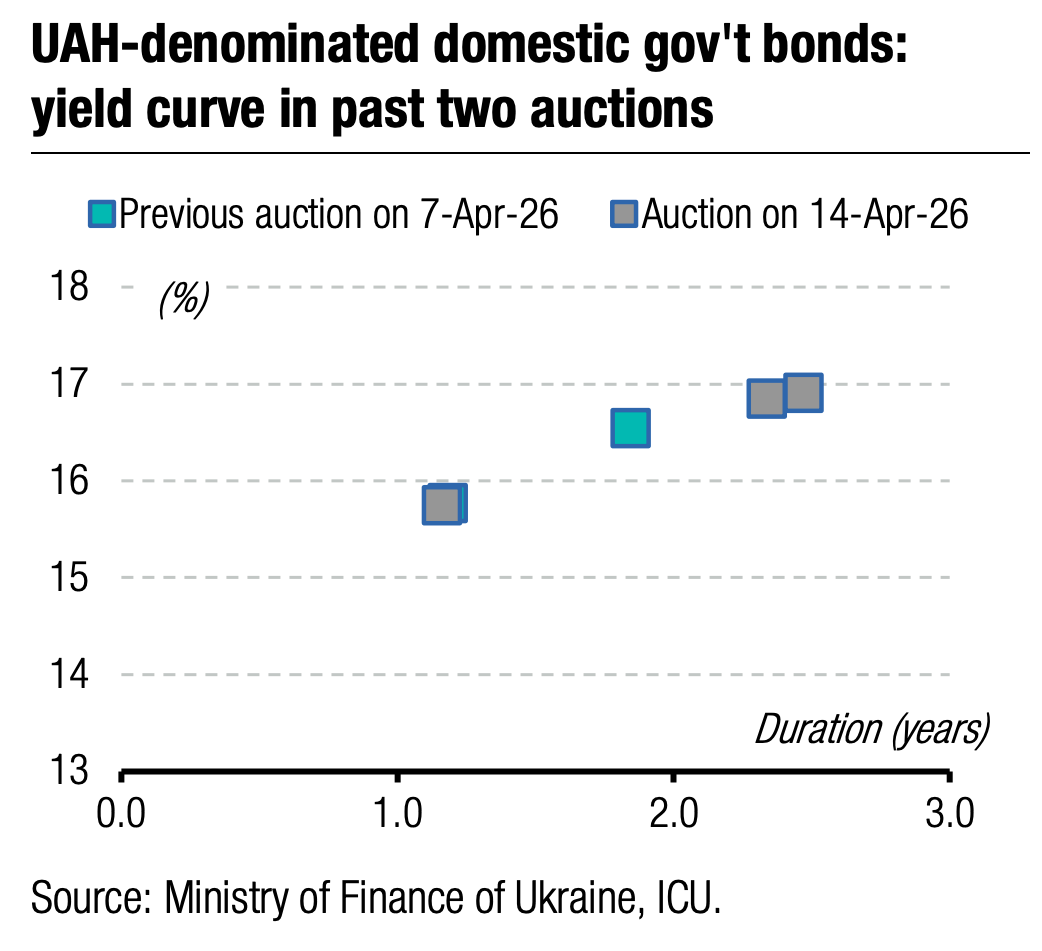

The 15-month bill received 14 bids, but only for UAH101m with yields in the range of 15.1%-15.15%. Therefore, the ministry satisfied all of them in full, setting the weighted average yield at 15.13%.

There were fewer bids for the three-year note, only nine, but for UAH125mn. The yields in the bids were also in a narrow range, 16.1%-16.15%, so the MoF satisfied all of them. However, unlike the 15-month paper, the ministry set the weighted-average rate at the cut-off rate.

Note: [1] payment frequency abbreviations: M - monthly, Qtly - quarterly, SA - semi-annually, @Mty - at maturity date; [2] proceeds and volumes for the USD-denominated bonds are calculated based on the previous day's exchange rate 43.91/USD, 51.31/EUR; [3] yields on coupon-bearing bonds are effective yields to maturity. Sources: Ministry of Finance of Ukraine, Bloomberg, ICU.

The Ministry of Finance also offered a new bond with maturity in June 2029. Interest in it significantly exceeded demand for other UAH bonds. There were 14 bids totalling UAH634m, but the ministry decided that a 25bp premium would be too much over three-year securities. Therefore, the MoF set the cut-off rate and weighted average yield at 16.2%, i.e. with a premium of only 5bp to the three-year note. Accordingly, two bids for UAH80m were rejected.

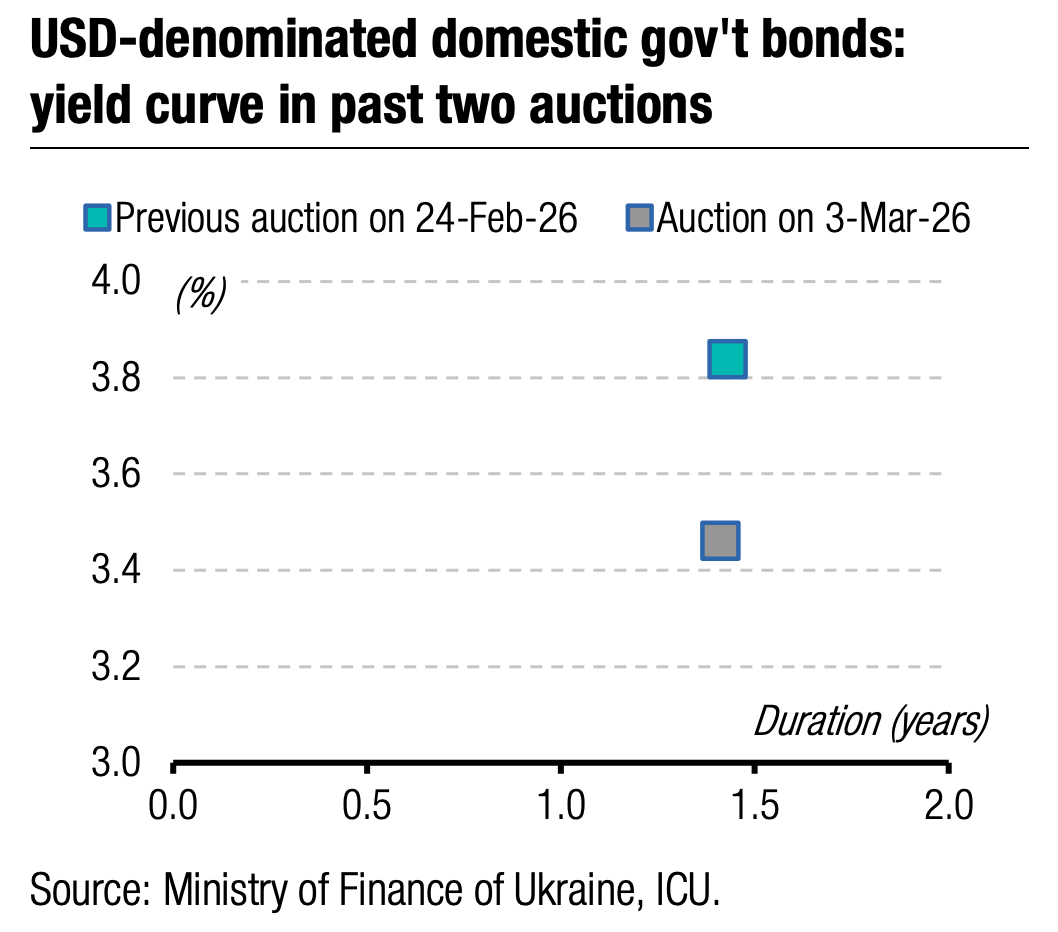

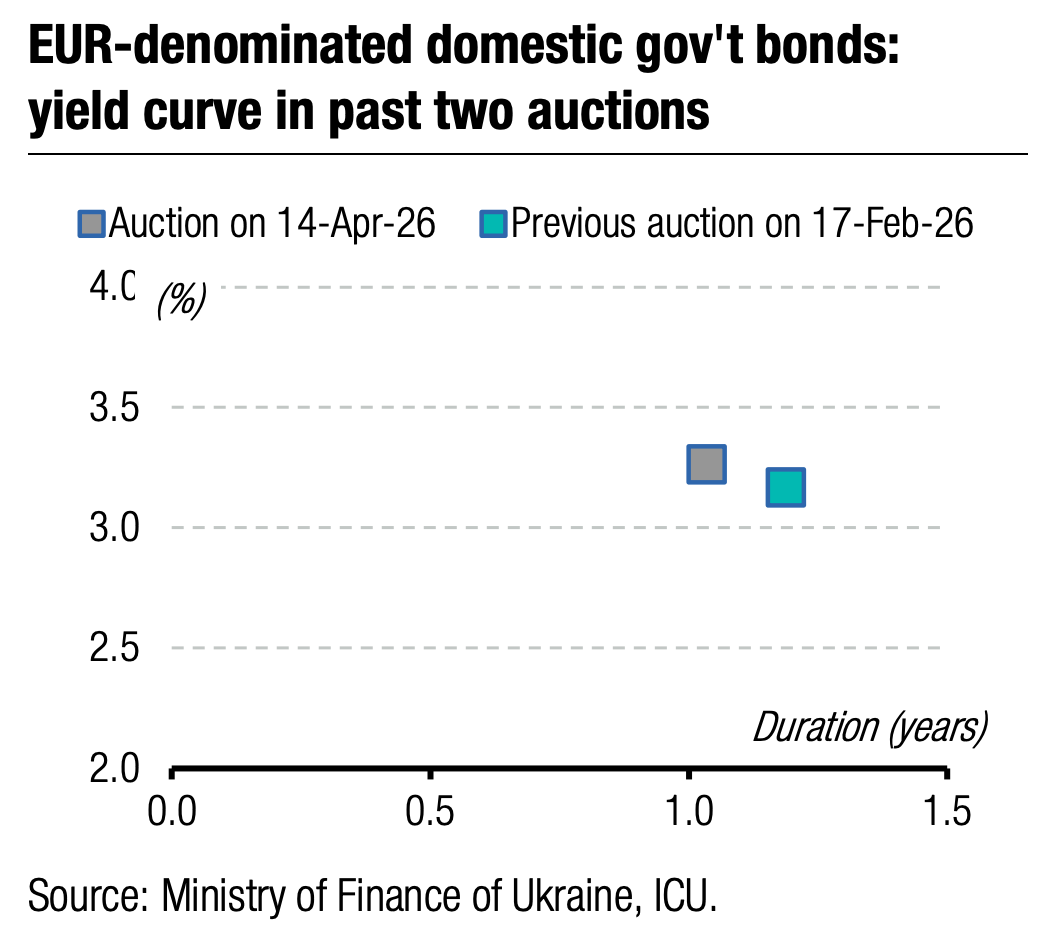

In addition, the ministry ended the pause in the issuance of FX-denominated bonds, which had lasted more than a month, and offered EUR-denominated bills. The bid-to-cover ratio was 1.3 times, so the Ministry of Finance was able to attract the planned funds. The cut-off rate remained at 3.25%, but the weighted average yield increased by 10bp to 3.24%. The MoF satisfied all bids, but some of them only partially within the cap.

The auction demonstrated that yields across all bonds have stabilised. There is currently no aggressive demand, but the Ministry of Finance is not ready to pay more, especially when attracting small amounts of funds.

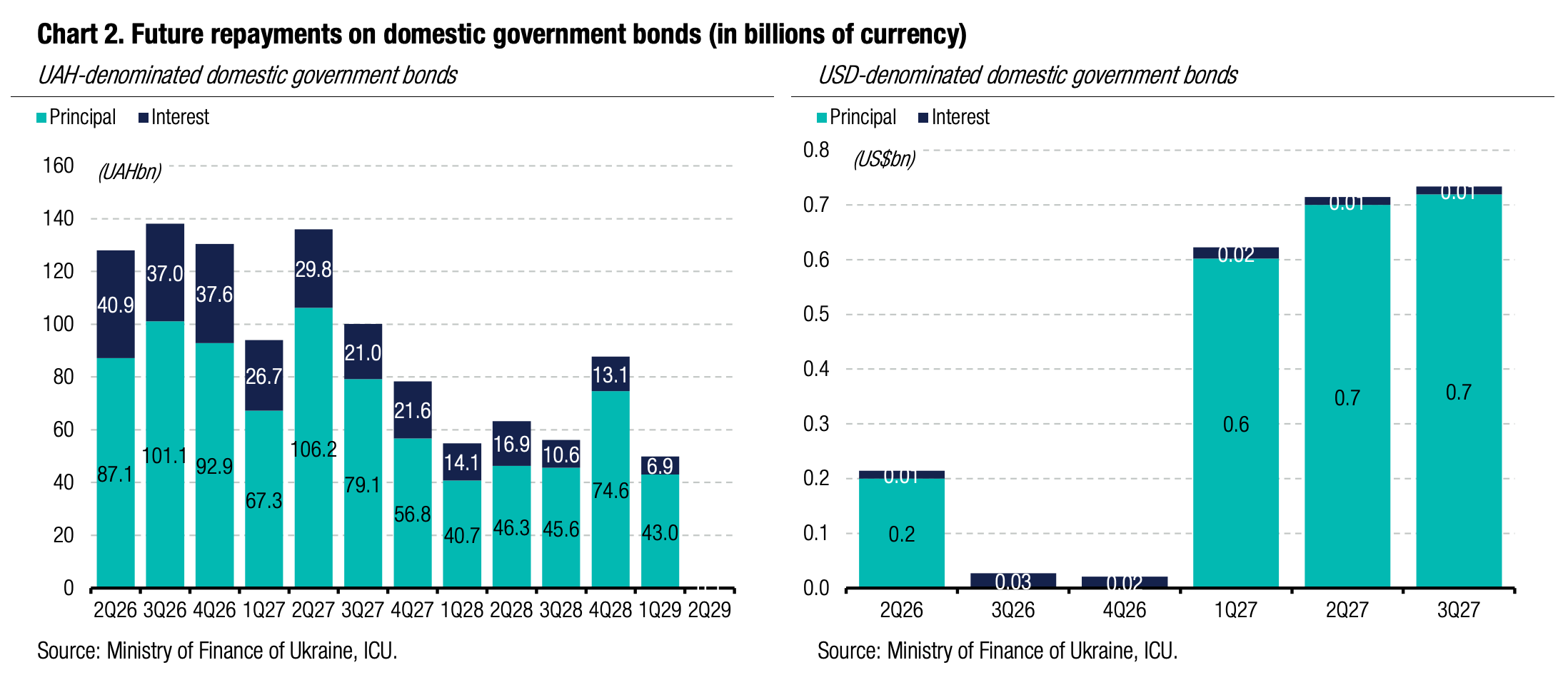

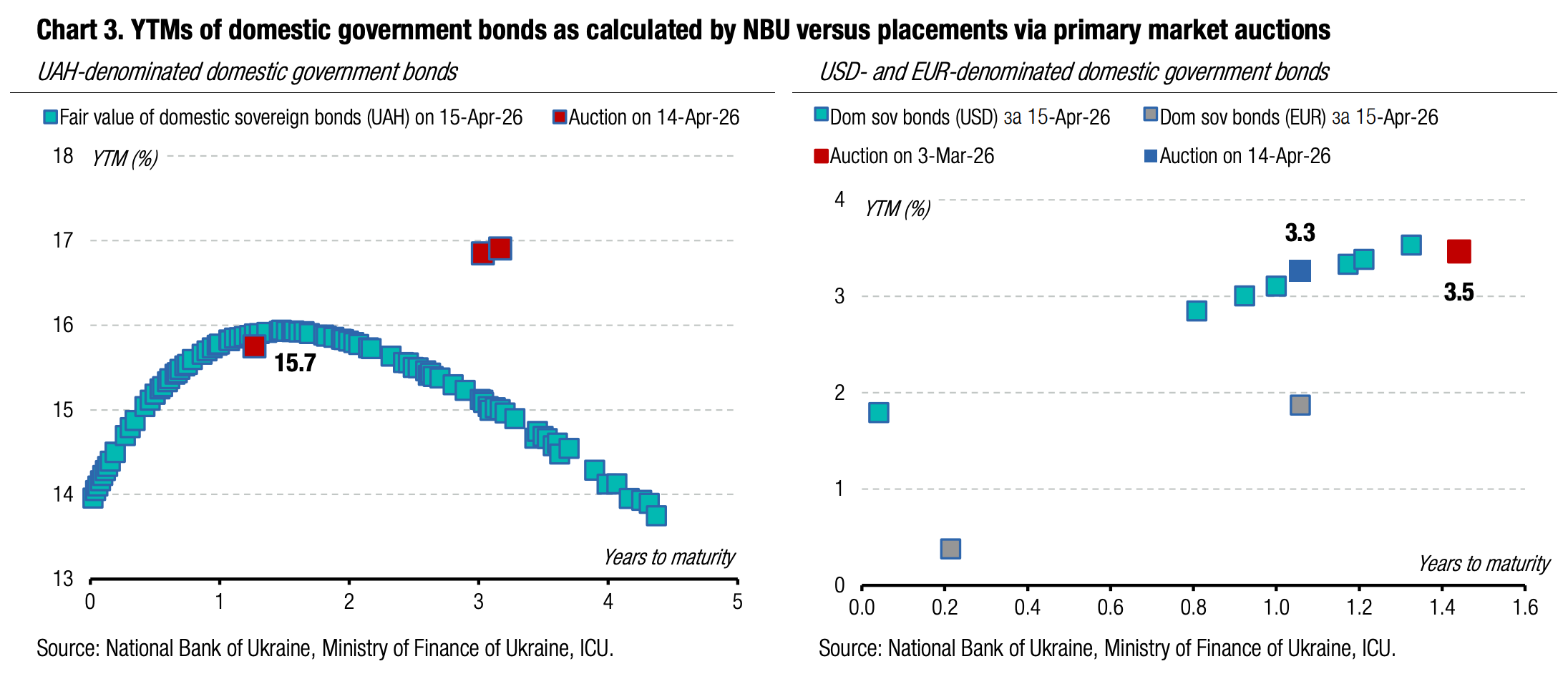

Appendix: Yields-to-maturity, repayments