| |

|  |

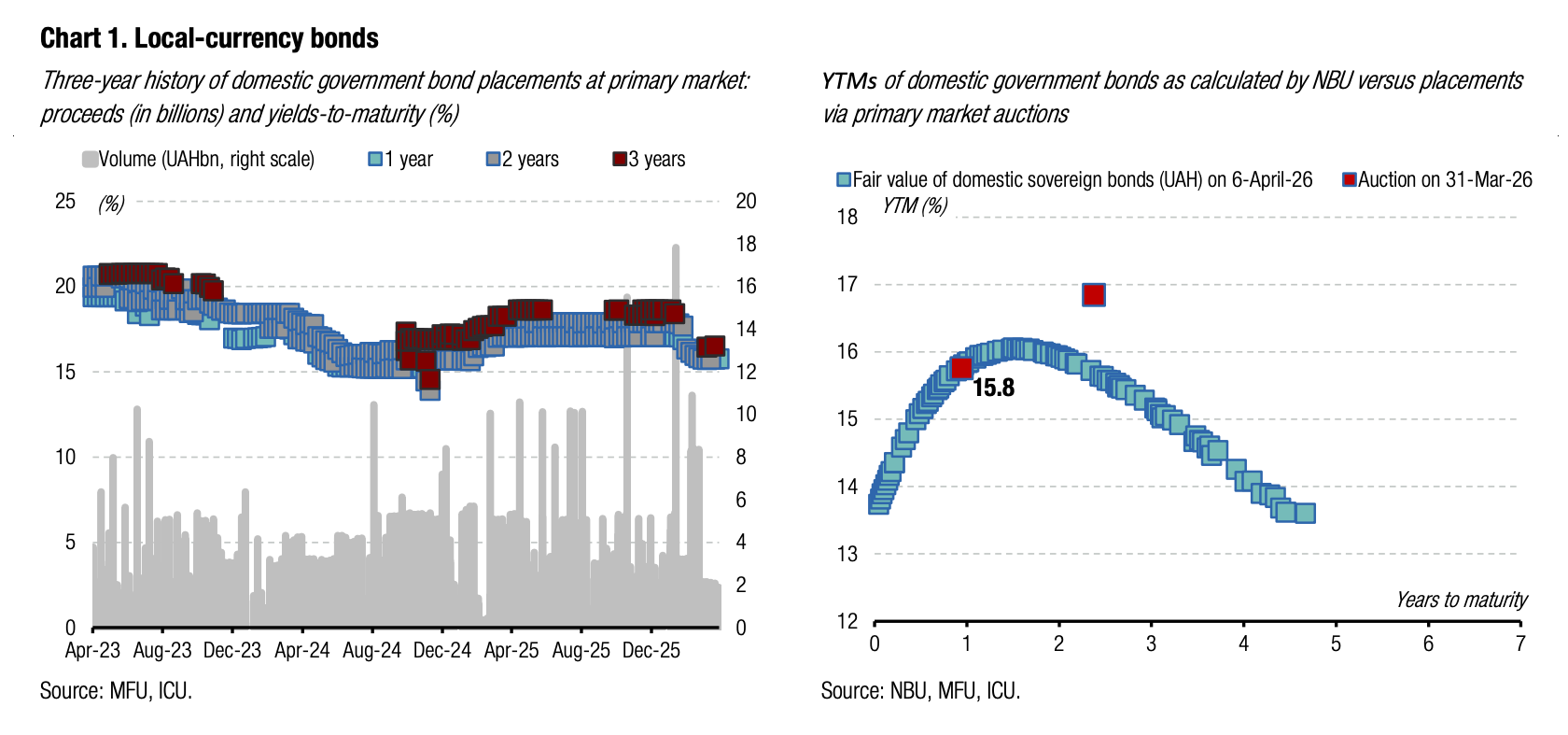

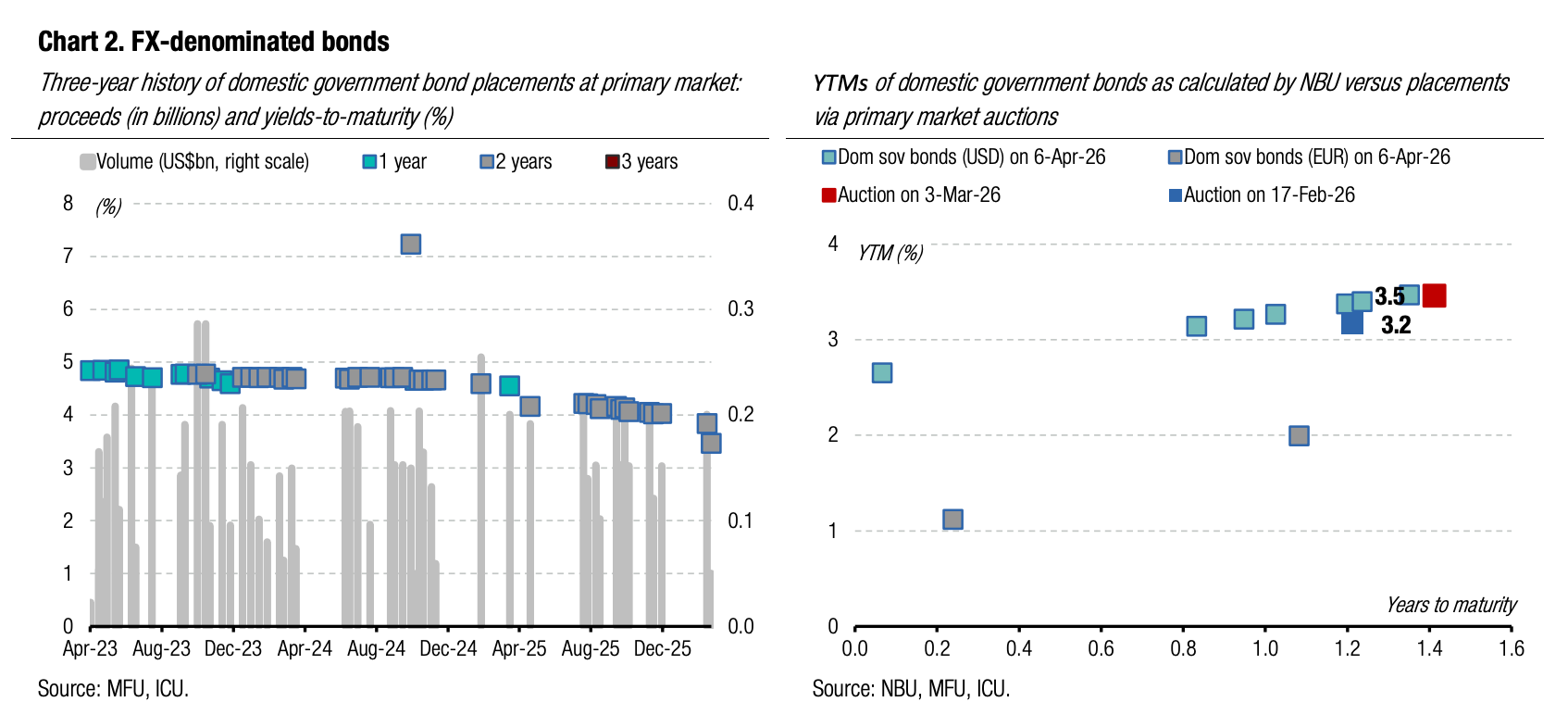

Bonds: MoF maintains domestic debt rollover above 100%

The Ministry of Finance continues to maintain a rollover rate for domestic debt at above 100%. Yet, net borrowings significantly decreased in March compared with January and February.

In March, the Ministry of Finance redeemed only UAH bonds for a total of UAH21.5bn, including UAH8.4bn of bonds maturing at the end of April that were exchanged for longer-term securities at an exchange auction in March. Meanwhile, new placements of UAH bonds stood at UAH25.6bn, including bonds issued for the exchange operation. Thus, the rollover of UAH debt in March was 119%. On top of that, the MoF sold US$50m of FX-denominated bills while no redemptions happened during the month. In hryvnia equivalent, net borrowings in all currencies totalled UAH6.3bn in March, significantly down from UAH20.6bn in January and UAH16.3bn in February.

Overall, the domestic debt rollover was 139% in 1Q26, little changed from 2M26. The rollover rate was 152% for hryvnia debt (162% in 2M26), 55% for US dollar debt (44% in 2M26), while for debt in euros, all EUR91m are net borrowing.

ICU view: Following two months of active borrowing and high rollover, the MoF sharply reduced net borrowings in March. The Ministry of Finance's further plans will be largely shaped by the prospects for receiving external financial assistance. If the EU approves the Ukraine Support Loan at least until mid-May, the MoF will continue to place domestic bonds at a comfortable pace targeting a rollover of about 100%. However, significant delays with the EU loan may force the government to increase domestic borrowing significantly.

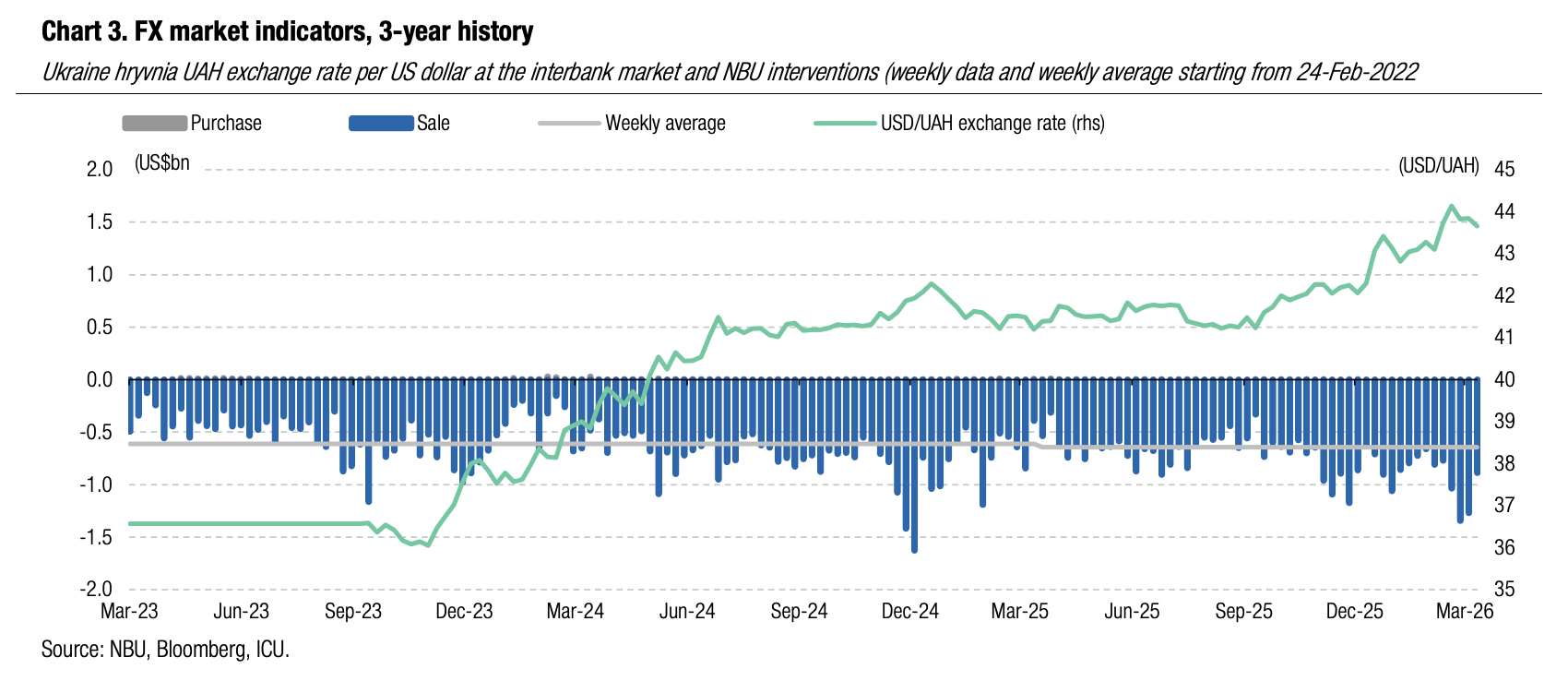

FX: NBU reduces interventions sharply

Last week, the NBU sharply reduced its FX sale interventions, although they remained at a high level. At the same time, the NBU continued to strengthen the hryvnia.

The National Bank continued to sell foreign currency actively last week, but total interventions were cut significantly to US$888m. That is close to the average weekly volume of interventions YTD and a third less than this year's maximum in mid-March. In total, in 1Q26, the NBU's net sale interventions reached US$11.5bn, which is US$2.1bn or 22% more than in 1Q25, when the NBU sold an average of US$750m per week.

The NBU also continued to strengthen the hryvnia gradually, setting the official exchange rate on Friday at UAH43.65/US$, while the interbank FX market closed last week with quotes near UAH43.5/US$.

Demand for hard currency decreased across both the interbank FX market and retail segments. Net purchases of foreign currency by bank clients (legal entities) fell by 35%, while net purchases in the retail segment slid by 12%. Thus, the total foreign exchange deficit decreased by a third to US$630m.

ICU view: The National Bank FX sales fully covered the excess demand reducing exchange rate concerns of both households and corporates. Noteworthy, net FX purchases in the retail segment decreased at the beginning of April, which is a noticeable trend reversal after they previously have been rising for many consecutive weeks. While the situation stabilized, we expect net FX sales by the NBU will continue to exceed interventions in the same period of the previous year. It seems that the NBU remains committed to keeping the exchange rate below UAH44/US$ at least for the coming weeks.