|  |

|  |

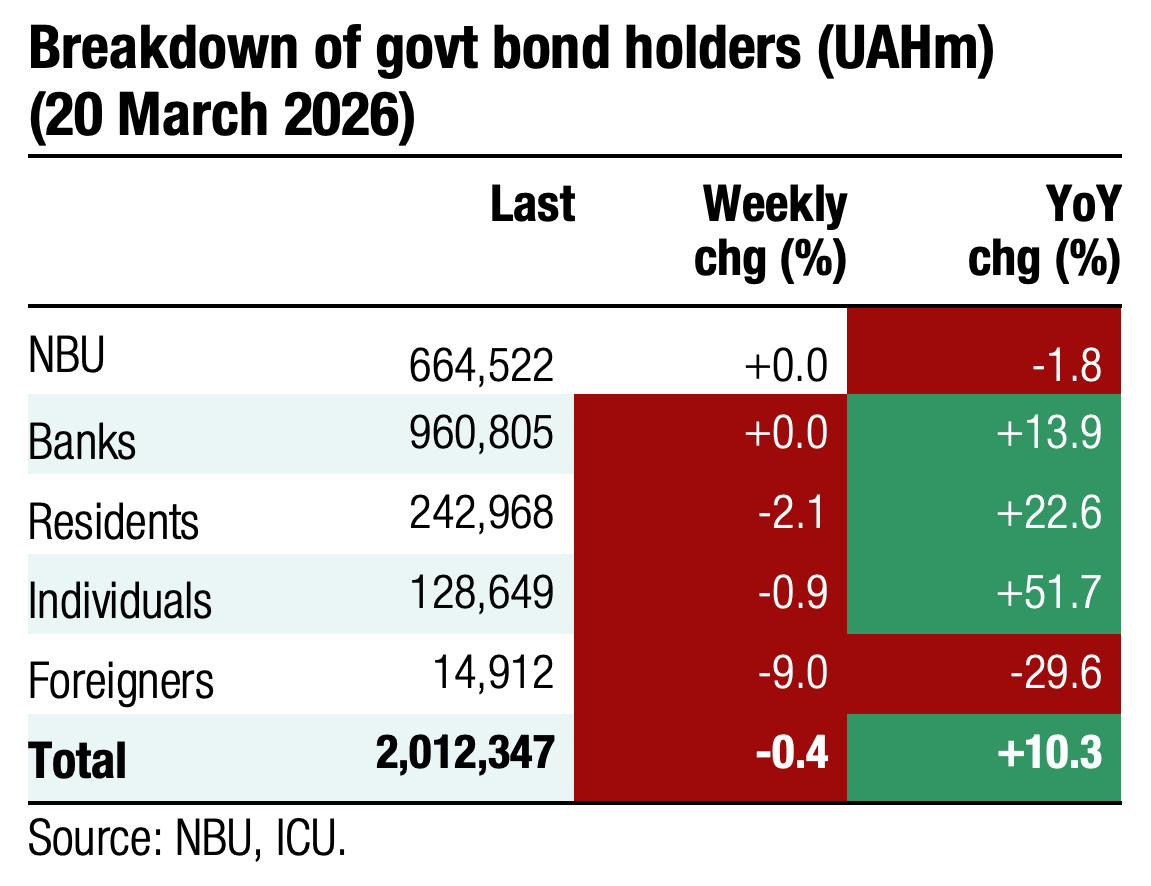

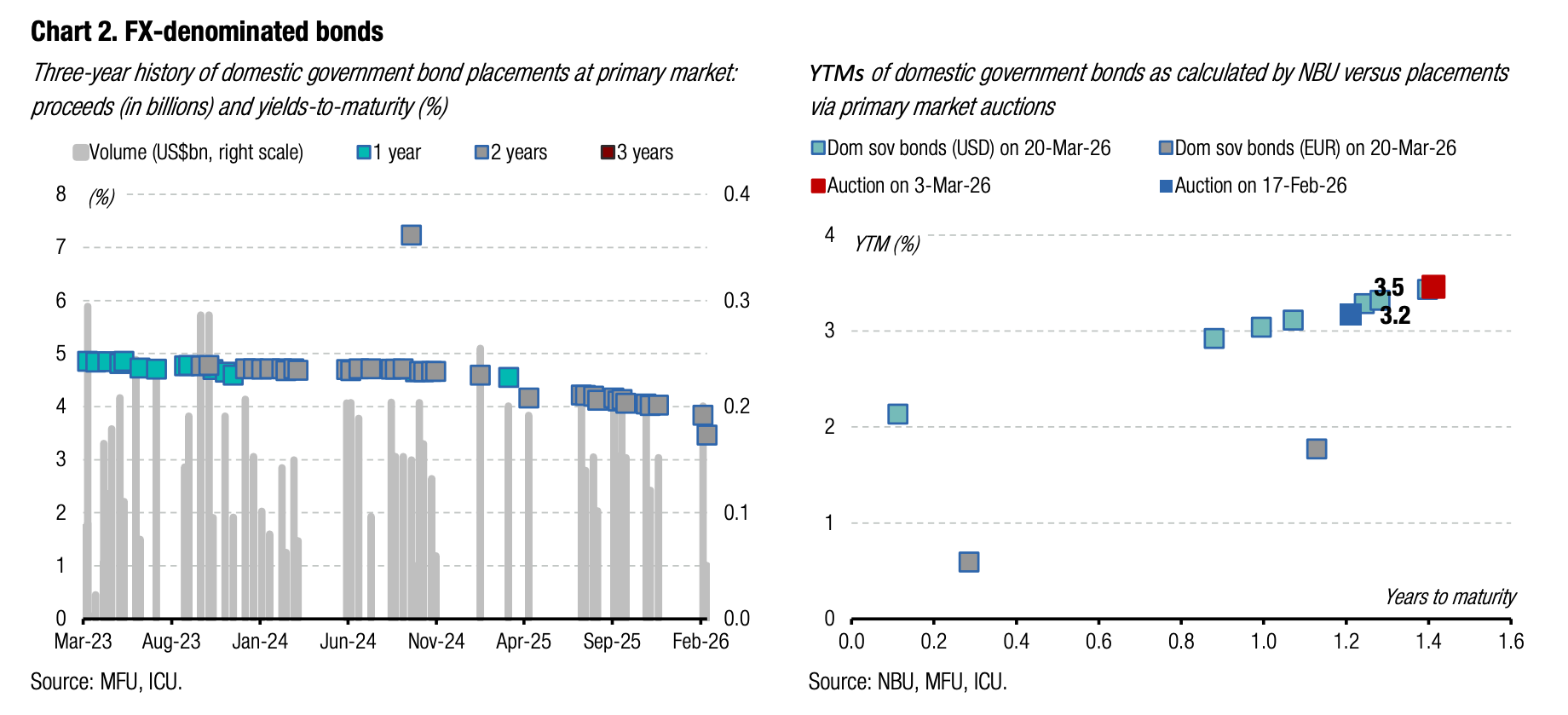

Bonds: Potential rate cuts on UAH bonds almost exhausted

The decline in yields on UAH bonds has almost ended, and only minor changes, within a few basis points, are likely in the near term.

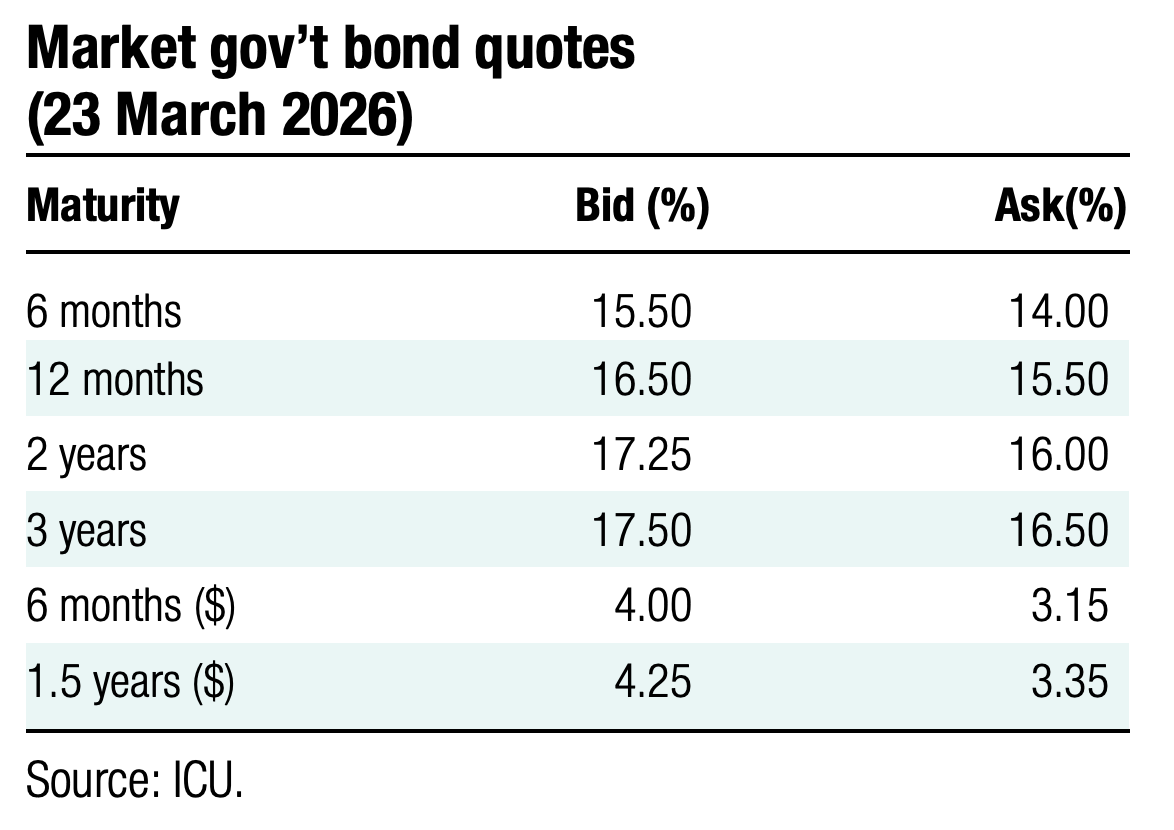

At last week's auction, yields on one-year military paper did not change, while the cut-off rate slid by 5bp to 16.15% for the three-year note with weighted average yield adjusting down by a mere 3bp to 16.13%. Meanwhile, demand fell sharply. It was below the offer for one-year securities, and more than halved, from UAH18bn to UAH7bn, for three-year securities. See details in the auction review.

For one-year and three-year securities, the spread between the minimum bid and cut-off rates narrowed to 15bp. The second placement this year of a two-year bond will take place tomorrow, and this spread may narrow from 37bp two weeks ago to 15-20bp.

Rate adjustments in the secondary market also slowed reflecting the pattern of the primary auctions. According to the NBU, YTMs of bonds with maturities of one to three years were in the range of 15.5%-16.8% for the past two weeks.

ICU view: The MoF significantly outpaced the NBU in reducing interest rates, so last week's NBU decision to keep key policy rate unchanged (see comment below) leaves the MoF with almost no room to reduce the yields further. The NBU is interested in keeping monetary conditions appropriately tight to maintain the attractiveness of UAH instruments, and we are unlikely to see an NBU key rate cut soon given the huge uncertainly related to Iran war. In addition, the NBU noted that if risks increase, it may even need to raise the key rate. Therefore, the current level of yields on UAH bond may remain steady in the coming months.

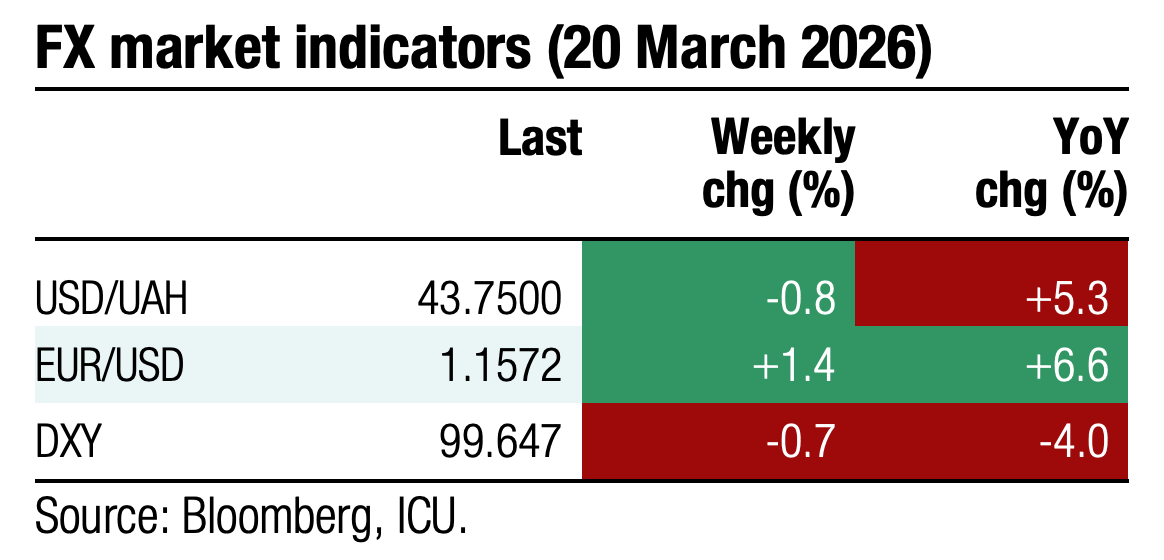

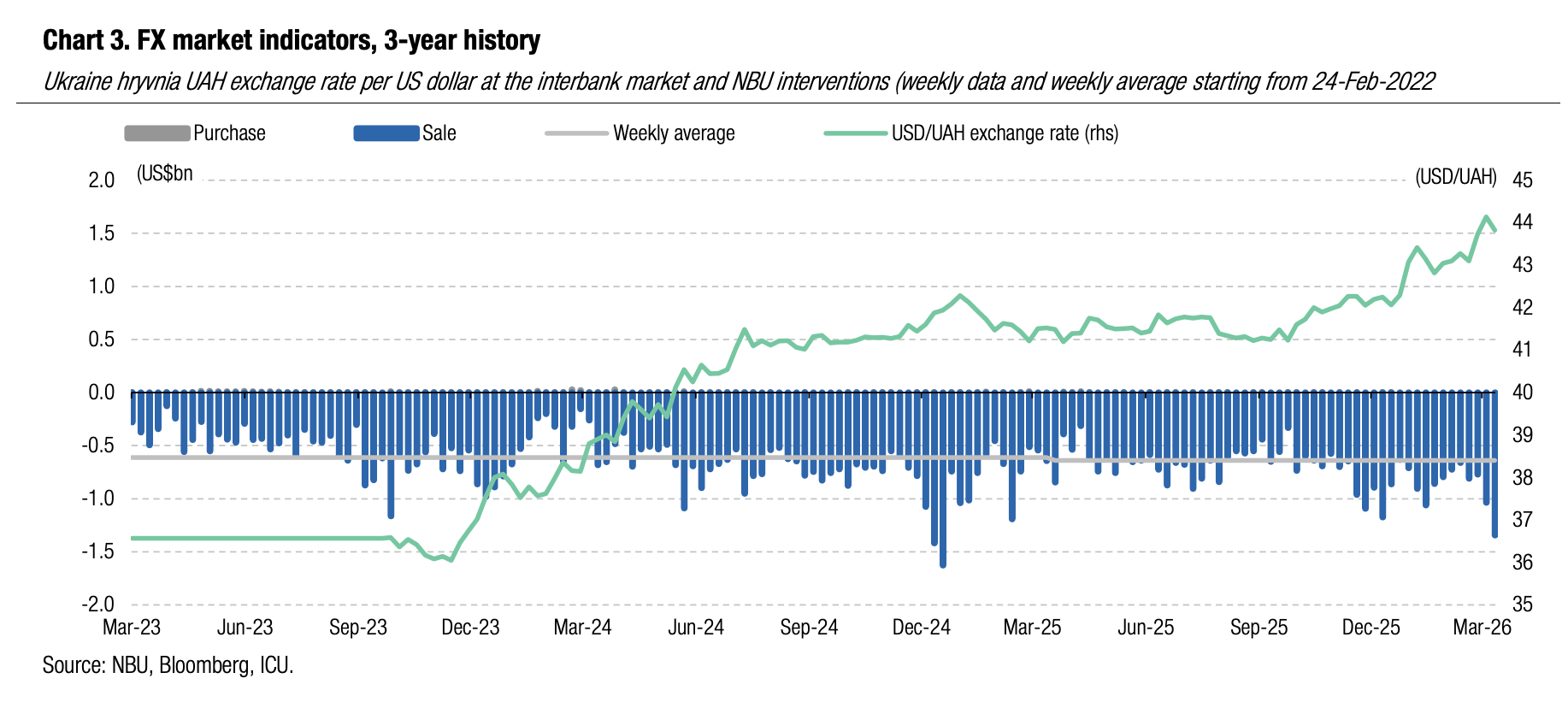

FX: NBU interventions surge to support hryvnia

Last week, the NBU ended up with the largest FX sell intervention this year to keep the hryvnia below UAH44/US$.

The hard currency deficit increased by almost 70% last week. Net FX purchases amounted to US$915m in four business days. Specifically, net purchases increased by 76% WoW to US$683m in the interbank FX market, and by 50% WoW to US$232m in the retail segment. The key driver of the gap was a significant decrease in foreign currency sales by bank clients (legal entities) in the interbank FX market accompanied a higher demand for hard currency.

The NBU's weekly interventions surged 30% WoW to US$1.3bn, the largest volume since December 2024.

The NBU strengthened the hryvnia by 0.7% WoW, setting the official exchange rate for today at UAH43.82/US$, while the interbank FX market closed at UAH43.6/US$ last Friday.

ICU view: The National Bank is clearly concerned with maintaining the attractiveness of hryvnia assets and ensuring the stability of the FX market. Last week, it took clear, bold action to reduce panic and stabilise the hryvnia exchange rate below UAH44/US$. According to the NBU, higher geopolitical uncertainty and a related turbulence in global financial and commodity markets is the main reason for the US dollar's appreciation against many currencies, including the hryvnia. The NBU signals it remains in a comfortable position even with the current level of interventions and expects substantial inflows of international aid in the coming months. We continue to expect the hryvnia exchange rate to end the year close to UAH45/US$.

ʼ

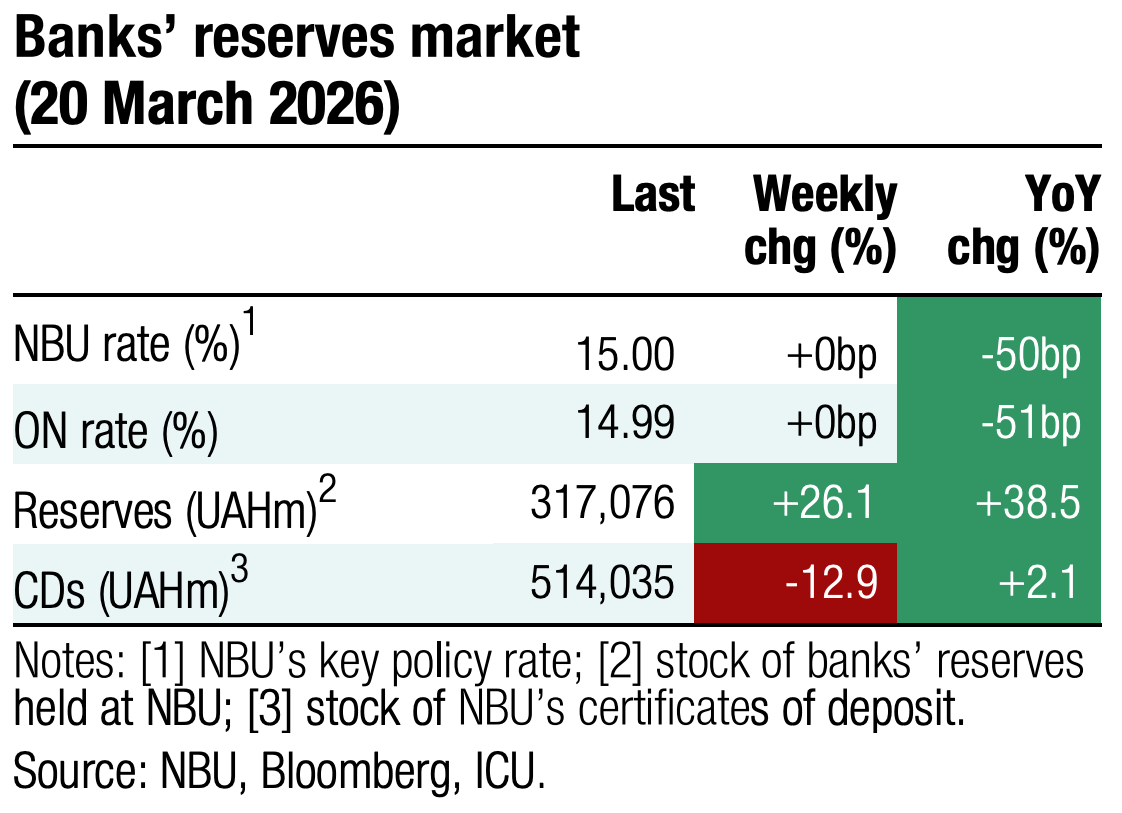

Economics: NBU keeps key rate unchanged at 15.0%

The regulator maintained the key policy rate at 15.0%, postponing further monetary easing amid risks of intensifying inflationary pressures and deteriorating inflation expectations.

Following a prolonged period of decline, headline inflation slightly accelerated to 7.6% YoY in February, while core inflation remained at 7.0%. The deterioration in expectations was likely driven by the challenging energy situation and the simultaneous price increases for everyday goods.

Geopolitical risks have also intensified significantly over the past month. The war in the Middle East has led to a substantial increase in fuel and gas prices, which has already affected domestic prices in Ukraine. Consequently, the inflation trajectory in the coming months will highly likely be somewhat higher than the NBU's January forecast envisaged. To maintain the attractiveness of hryvnia instruments and preserve currency market stability, the regulator decided to pause the easing cycle.

ICU view: The war in Iran significantly increases upside risks to inflation. We believe that the 2026 year-end key rate forecast of 14.5% is more likely to be revised upwards rather than downwards at this point. Yet, we do not think at this point that a rate hike in 2026 is the most probable outcome.