Ukrainian bond market

MoF maintains proactive stance

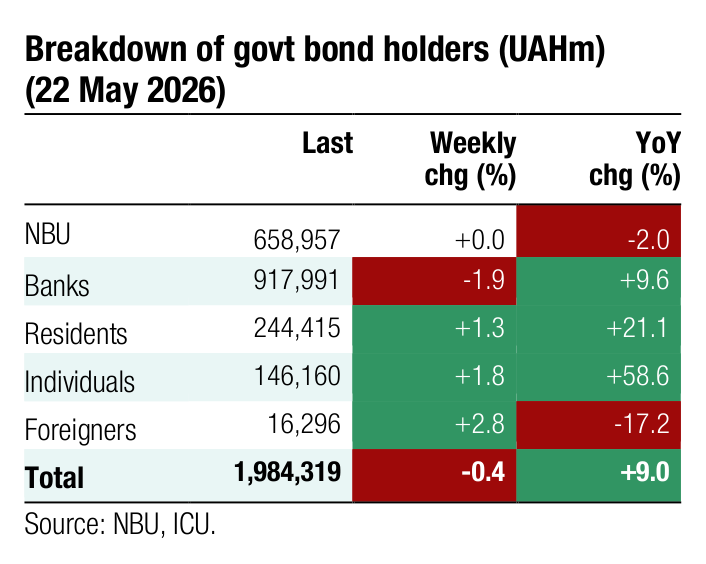

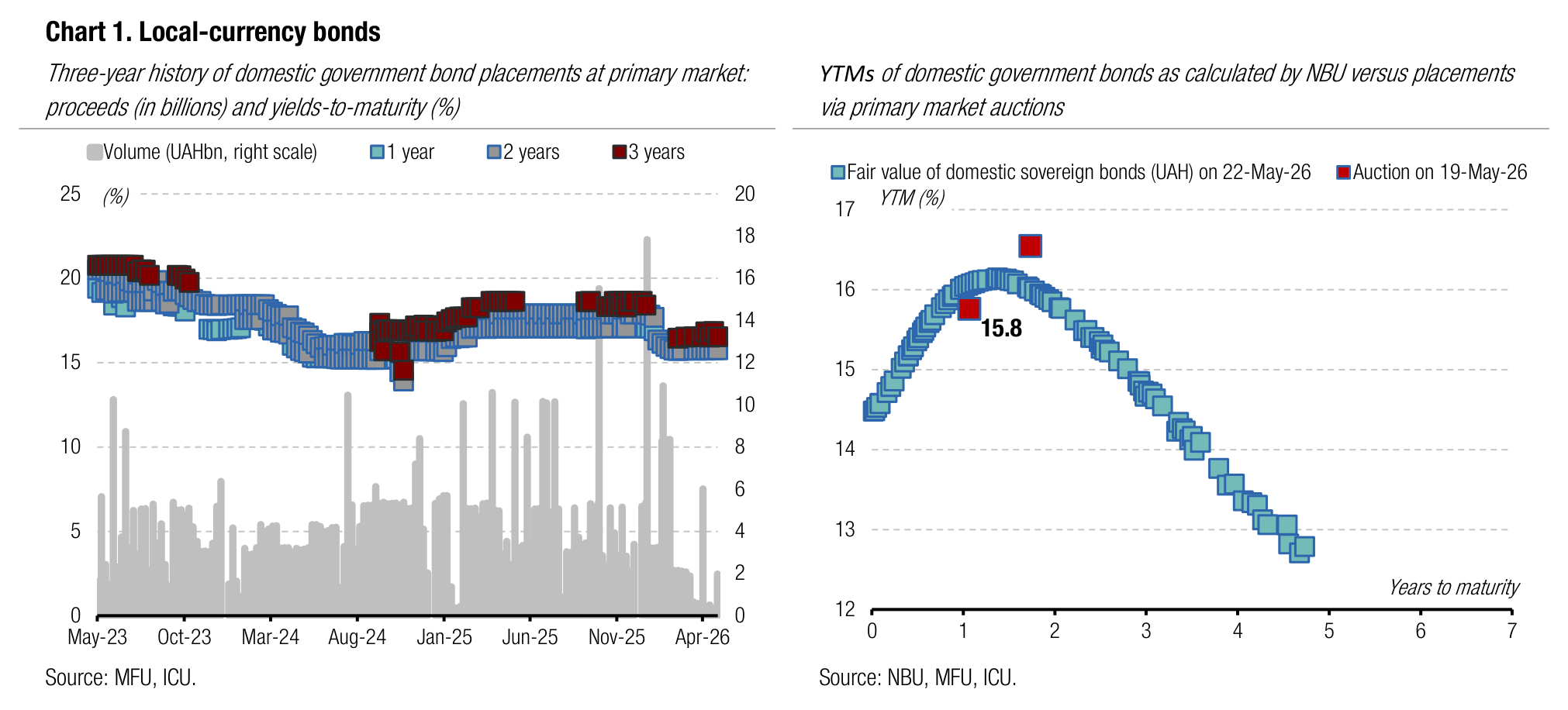

Last week, the Ministry of Finance held its fifth bond exchange auction YTD to smooth out the debt redemption schedule.

On Wednesday, the MoF offered holders of bonds due this June an exchange for bonds maturing in June 2028. The MoF exchanged UAH3.9bn par value of bonds or UAH4.2bn at market prices. The total amount of exchanged bonds reached almost UAH48bn YTD.

ICU view: The Ministry of Finance continues to proactively use the bond exchange mechanism. Last week, more than a quarter of the issue due on June 10, was exchanged. Despite an active bond exchange stance, YTD net borrowings have been declining in recent weeks. The draft amendments to the state budget submitted to Parliament in early May do not envisage any changes to the domestic borrowing plan, so we expect the YTD rollover rate (in all currencies) at approximately 100% at end- 1H26.

Eurobond sentiment upbeat on positive media coverage

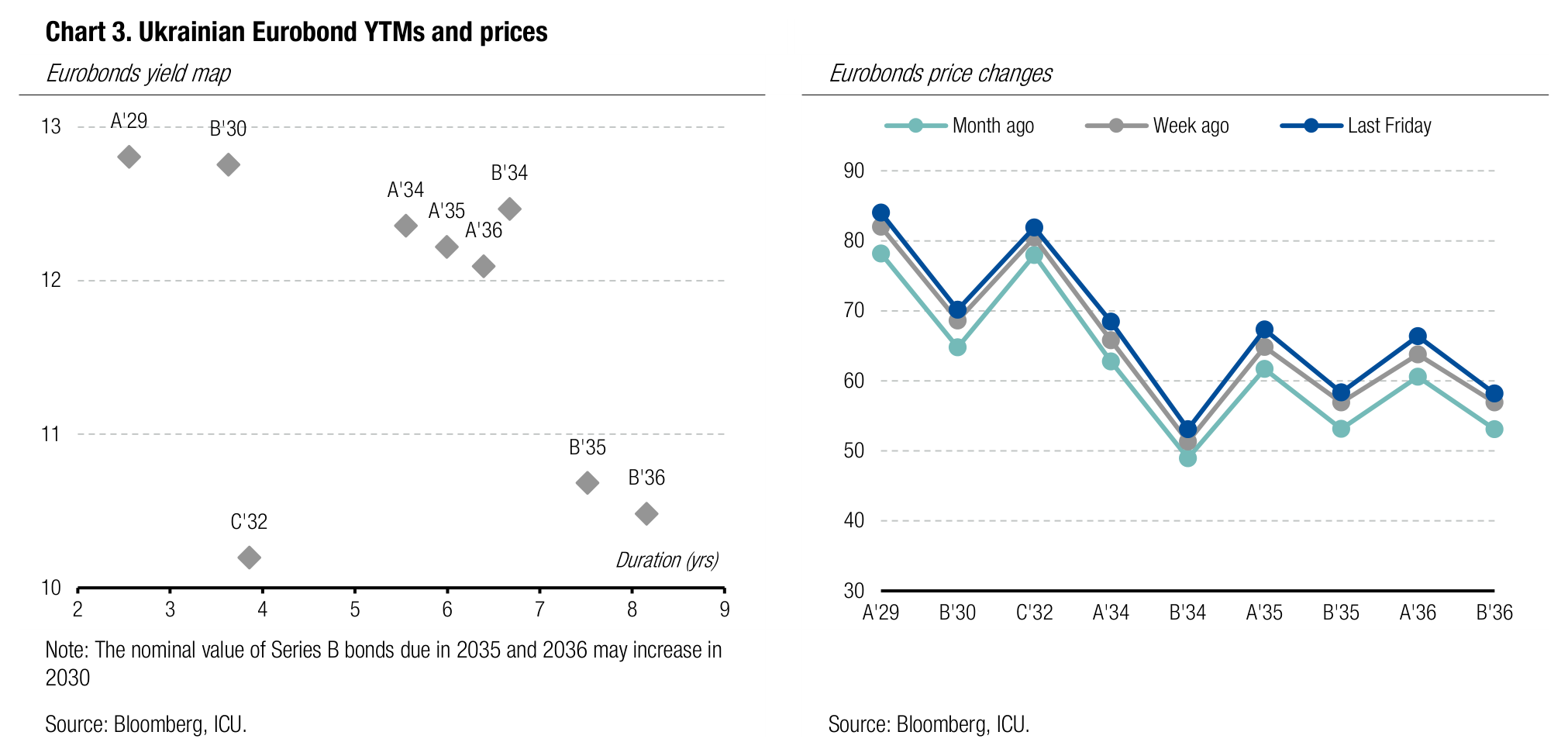

Ukrainian Eurobonds rose again last week as international investors were encouraged by overly optimistic Western press coverage of the war.

Early last week, the Financial Times published an article stating that the Chinese president indicated that putin might eventually regret his decision to invade Ukraine. The Chinese side later denied this statement.

On Thursday, a Bild article highlighted three main russian failures in the war: heavy losses on the frontline, the lack of fresh territorial advances, and Ukrainian counterattacks that reach infrastructure and military facilities deep behind the frontline.

The week concluded with a Bloomberg text that, like the above-mentioned ones, stated Ukraine and its allies are increasingly confident that the russian invasion is losing steam, as Ukraine stabilises the frontline and successfully prevents the enemy's spring offensive.

All in all, the Ukrainian Eurobonds rose another 3% last week, and almost 25% since the end of March, when prices collapsed amid global turbulence. Eurobonds maturing in 2029 rose on Friday to 84 cents, the highest since the 2024 restructuring. The Series C bonds issued at the end of 2025 and due in 2032 reached 82 cents. The Series B Eurobonds with maturity in 2035-36 also rose in price, but remain well below the highs, as the prospects of additional issuance are getting increasingly bleaker.

ICU view: The active coverage by the global media of the current situation on the front and Ukraine's strengthening bargaining power lends more ground for investor optimism. Yet, we believe the optimism is hardly justified and the prospects of ending the war in the foreseeable future are still illusory, especially given the lack of US interest in this matter during the ongoing Iran crisis.

Foreign exchange market

NBU sets new lows for the hryvnia

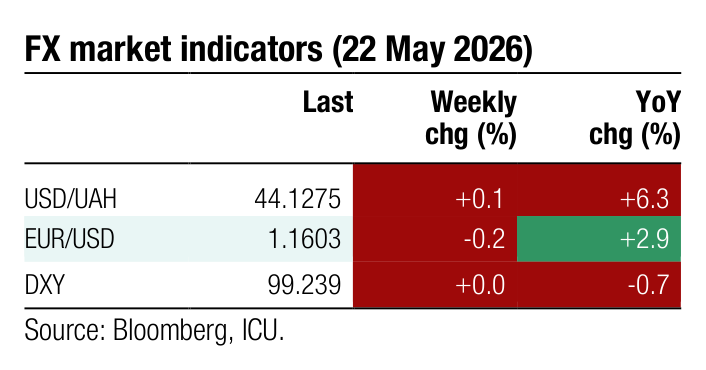

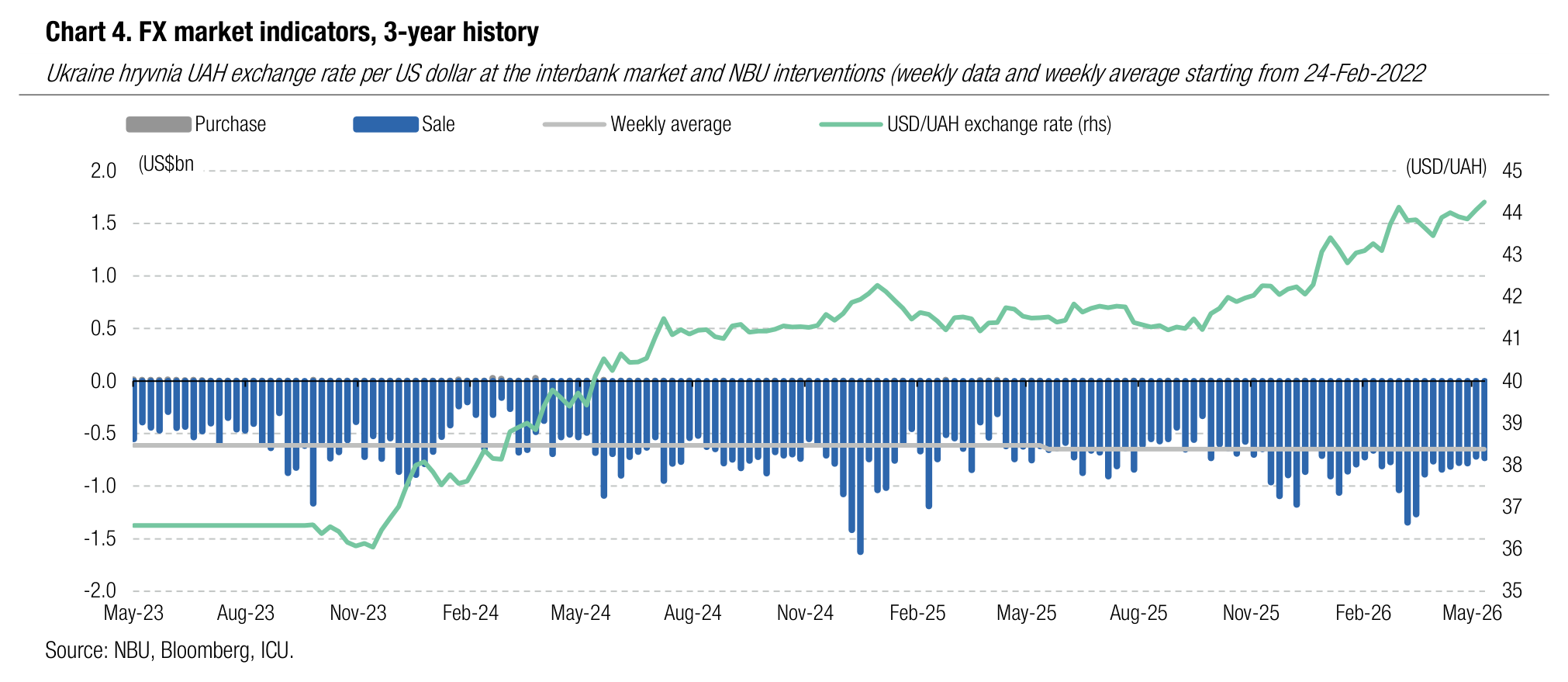

Last week, the NBU allowed the hryvnia to weaken to a new historical low without any specific market preconditions.

Over the four business days of last week, the foreign currency deficit was US$454m, slightly above previous weeks but significantly below shortages in January-April. NBU interventions edged up 2% WoW to US$734m.

The National Bank allowed the hryvnia to fall to UAH44.3/$ on the interbank market on Friday and set the official exchange rate for today at UAH44.26/US$, which is up 0.4% WoW and 4.5% YTD.

ICU view: The NBU continued to widen the hryvnia's exchange rate fluctuations last week, which may be a targeted move ahead of the IMF mission visit to Kyiv this week. The FX market deficit is now close to this year's lows, but the FX market shortage and NBU interventions remain higher in YoY terms.