|  |

|  |

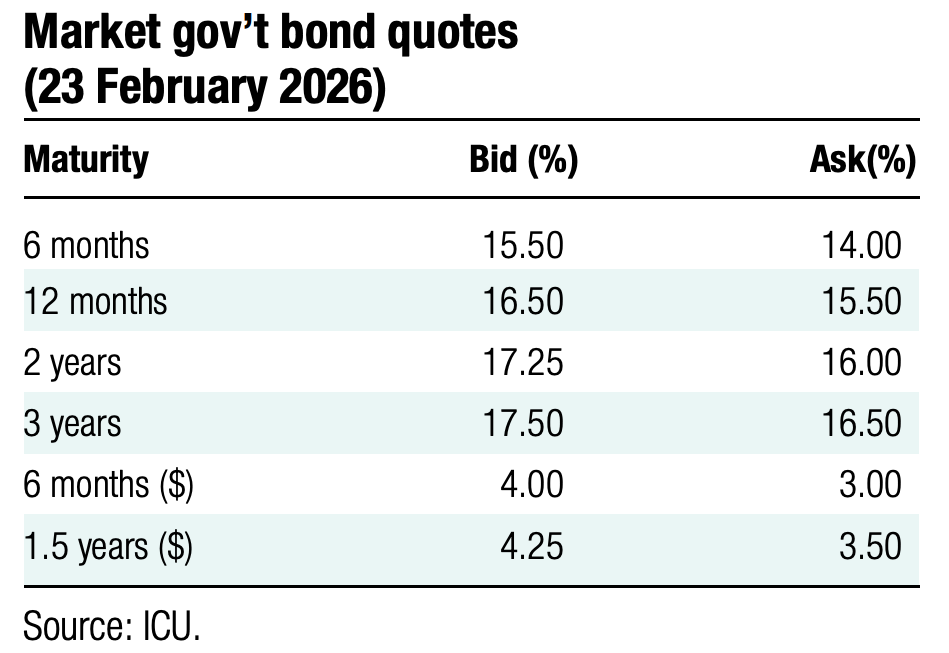

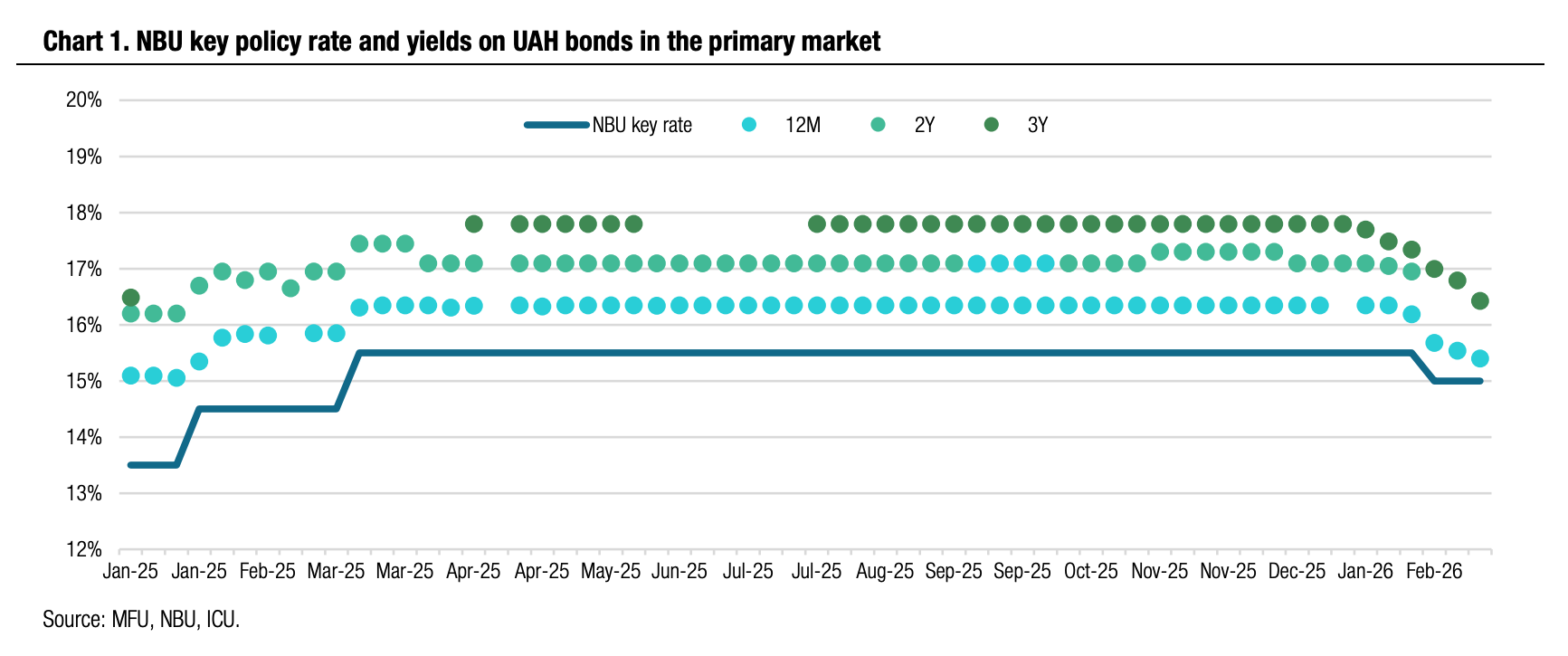

Bonds: MoF cuts maturity premium

The Ministry of Finance made yet more steps to lower yields on UAH bonds, while also significantly slashing the maturity premium.

Last week, the MoF placed both regular and military UAH bonds, a UAH reserve note, and also resumed offer of FX-denominated bills. Yields on all four types of securities dropped (see auction review). The placements of military and regular UAH bonds were the most notable ones as they saw a significant oversubscription and a further decline in yields.

The one-year military bill was 5x oversubscribed and the MoF sold the planned UAH2bn of bonds while reducing yield by another 16bp to 15.34%. The yield on the three-year note was down 37bp to 16.42% on 9x oversubscription. YTD, the weighted average yield on one-year paper in the primary market decreased by 101bp, and that on three-year paper was down by 138bp. This implies the decrease in bond yields is already multiple times greater than the 50bp NBU key policy rate cut YTD.

Such a rapid and uneven decrease in yields indicates a significant decline in the maturity premium. At the beginning of January, the MoF paid 70-75 bp of premium above the yield on 12-month bills for each additional year of maturity. Now, the maturity premium is close to 50bp per additional year. Overall, the difference in rates between one-year and three-year instruments has decreased over the past six weeks from 145bp to 103bp, and may well decrease further.

ICU view: Competition for new bonds in primary auctions remains intense, especially against the backdrop of a significantly lower supply compared with that in early January. At the same time, the MoF clearly shows signs of fatigue of waiting for (much overdue) cuts in the NBU key policy rate in the environment of low inflationary risks and the ministry began to slash bond yields decisively. In view of this, we expect further decline in bond yields, especially for longer maturities. An additional supporting factor for the ministry is a conservative borrowing plan for this year, as the domestic debt rollover is currently planned at below 100%. Accordingly, the yield on one-year bills may soon reach the NBU key rate, and the term premium may decrease further and possibly drop below 40bp per each additional year of maturity. This opens a way for the MoF to offer longer instruments, possibly with a five-year maturity, for which the yield may now be lower than those for three-year notes last year.

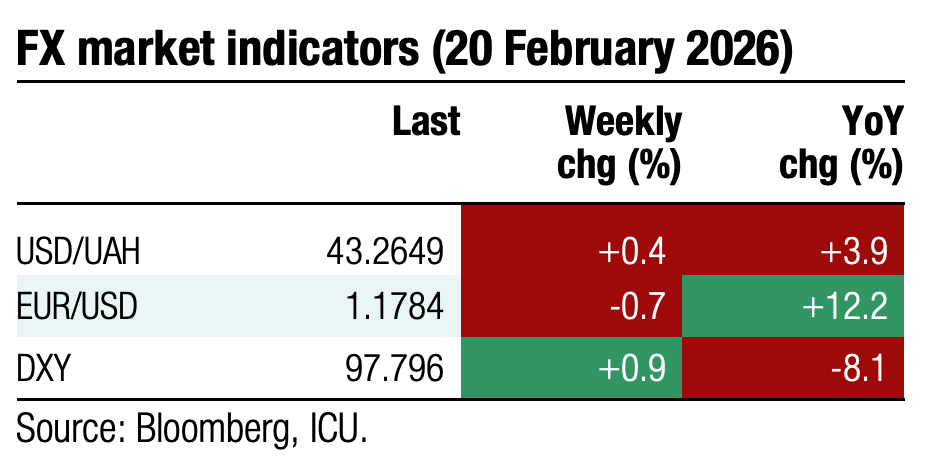

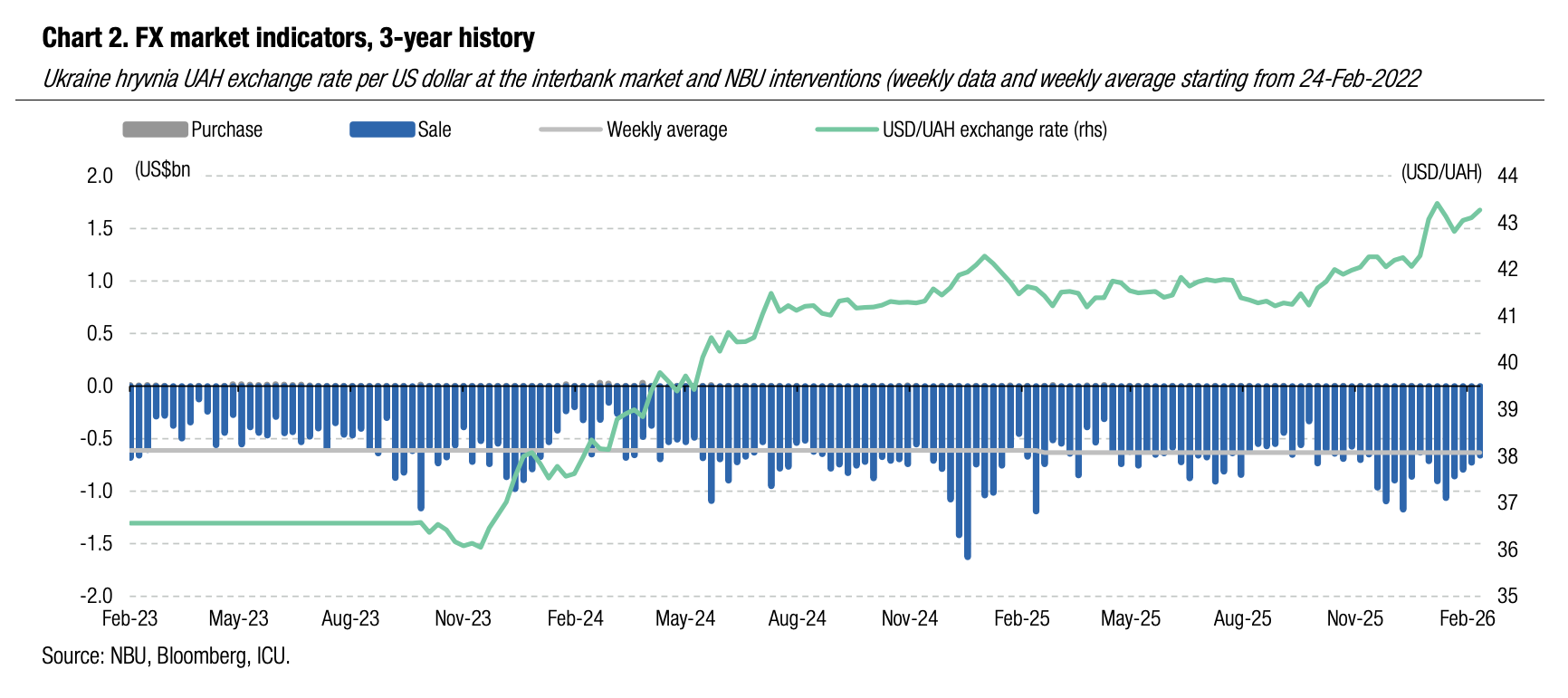

FX: NBU continues to restrain hryvnia fluctuations

Last week, the NBU allowed the hryvnia to weaken slightly despite a decrease in the foreign currency deficit and smaller interventions.

The National Bank weakened the official hryvnia exchange rate last Wednesday to UAH43.29/US$, but later reversed the move to finish the week at UAH43.27/US$. The FX market shortage was down by almost a quarter WoW, to US$383m. The NBU reduced interventions by a tenth to US$661m, slightly above the average weekly volume of interventions over the four years of the full-scale war.

ICU view: After the hryvnia weakened in December-January, the National Bank currently has no clear appetite for further devaluation and kept hryvnia volatility in a narrow range over the past several weeks. This approach may persist until the NBU stabilises the volume of FX sale interventions at a comfortable level, probably close to $600 million (the average weekly intervention size in 2025). However, we maintain our forecast of a gradual weakening of the exchange rate to UAH45/US$ by the end of the year.