|  |

|  |

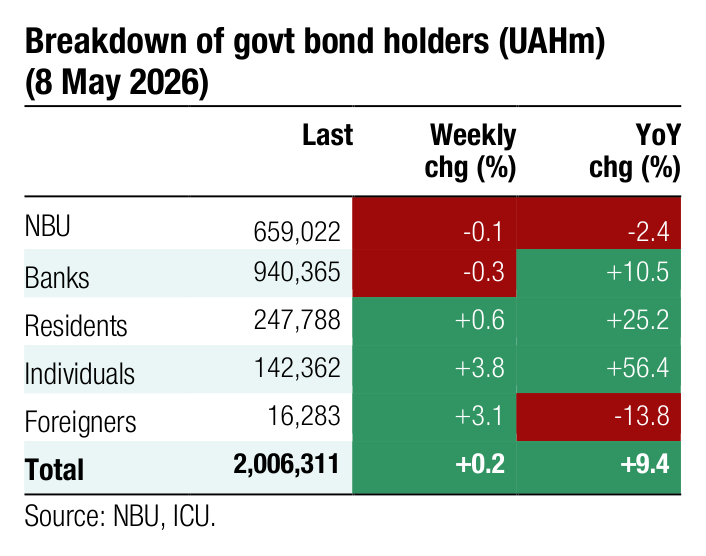

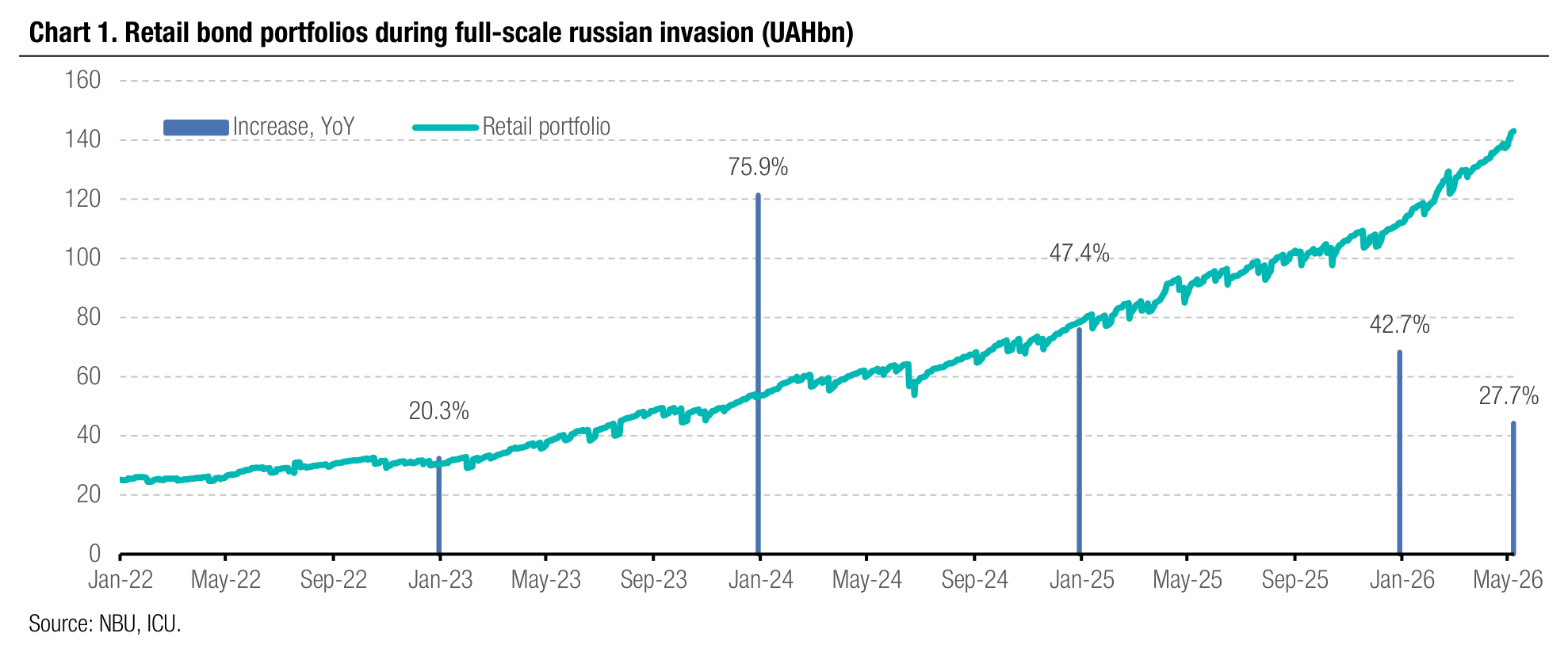

Bonds: Growth of local debt retail portfolio unabated

Households continue to build their portfolios of domestic government bond, and growth remains strong.

Retail portfolios increased by almost UAH5bn in early May and by UAH31bn YTD, and hit a new high of UAH143bn. The total retail portfolio of government bonds is up by 28% YTD and almost six-fold since the beginning of the full-scale war in Feb. 2022.

Other groups of investors are increasing their portfolios much more slowly: the total portfolio of government debt of banks remains little changed YTD, non-bank businesses increased their portfolios by UAH12bn (+5% YTD), and foreign investors – by only UAH0.4bn (+2.4%). Therefore, the share of the retail portfolio in total government bonds outstanding is approaching 11% (excluding bonds held by the NBU).

ICU view: Households continue to build their portfolios of domestic government bond, and growth remains strong. Retail portfolios increased by almost UAH5bn in early May and by UAH31bn YTD, and hit a new high of UAH143bn. The total retail portfolio of government bonds is up by 28% YTD and almost six-fold since the beginning of the full-scale war in Feb. 2022. Other groups of investors are increasing their portfolios much more slowly: the total portfolio of government debt of banks remains little changed YTD, non-bank businesses increased their portfolios by UAH12bn (+5% YTD), and foreign investors – by only UAH0.4bn (+2.4%). Therefore, the share of the retail portfolio in total government bonds outstanding is approaching 11% (excluding bonds held by the NBU).

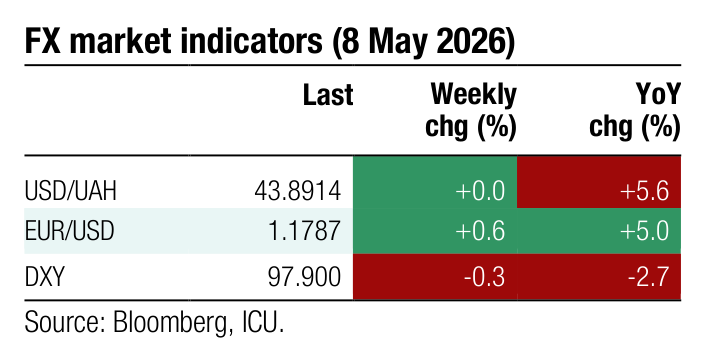

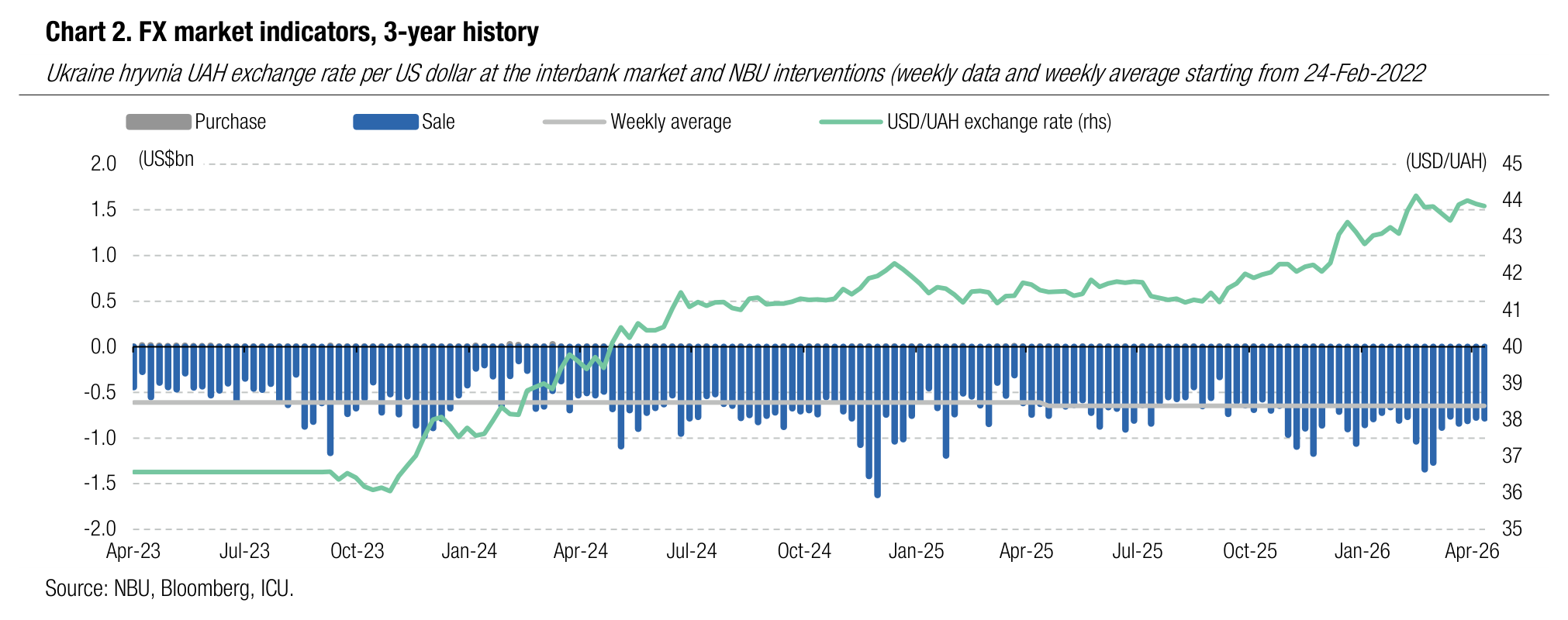

FX: NBU keeps hryvnia below UAH44/US$

After pushing the hryvnia exchange rate back to below UAH44/US$ at the end of April, the central bank did its best to keep USD/UAH almost unchanged throughout the past week.

The NBU began last week by weakening the official hryvnia rate to UAH44/US$, but eventually did not allow it to approach that level. The fluctuations band was pretty narrow, and the hryvnia strengthened slightly towards the end of the week. The NBU spent US$784m in interventions, nearly same size as a week before.

ICU view: Last week, the NBU once again demonstrated that, at this stage, it has no clear appetite for further hryvnia devaluation. That is despite that fact that FX sale interventions remain significantly higher than over the same period a year before.

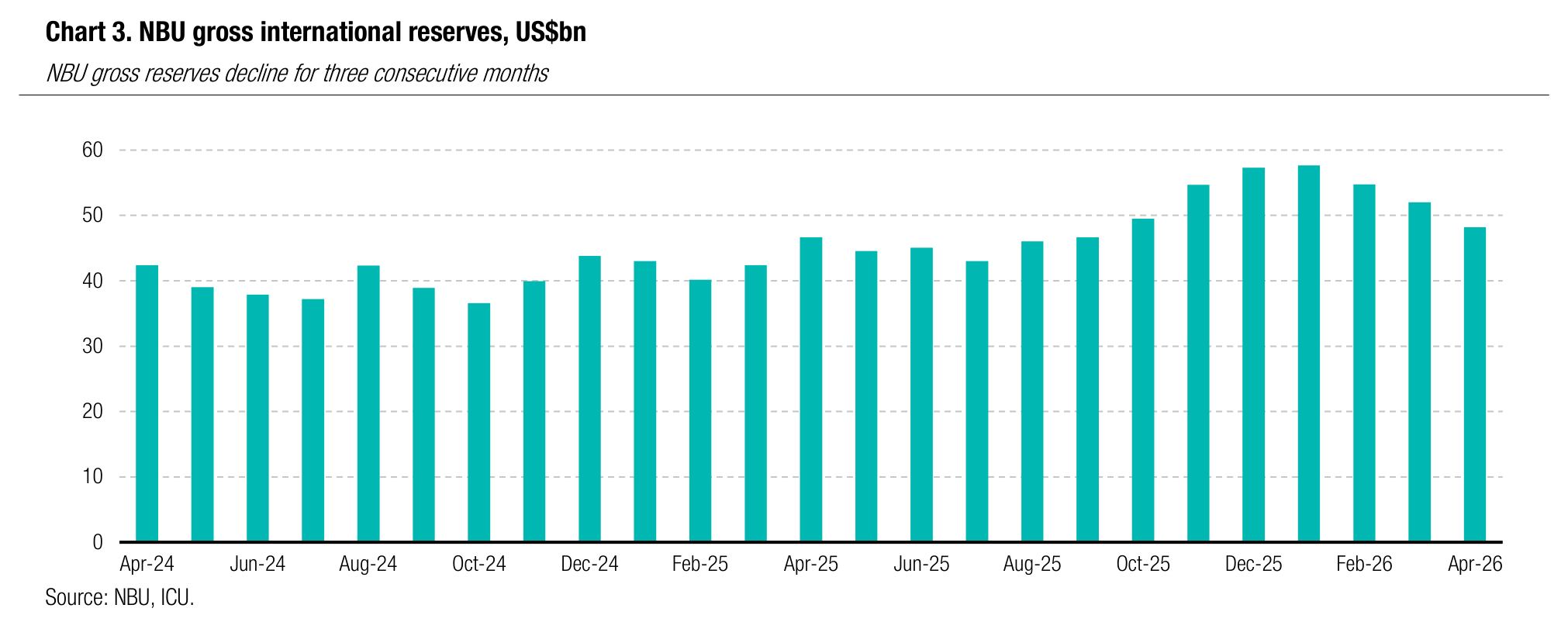

Economics: NBU reserves down 7% in April

Gross international reserves of the NBU declined 7.3% in April and 15.8% YTD to US$48.2bn. The reserves stood at 4.9-month equivalent of the future imports, according to the NBU estimates.

The sharp decline in reserves was driven by persistently high net FX sale interventions by the NBU that stood at US$3.6bn during April. Additionally, external debt servicing by the government and the NBU amounted to US$0.5bn in April. Meanwhile, the reserves were not replenished with foreign financial aid, which was negligible during the month. The US$1.0bn ERA facility from the UK was not counted towards the NBU reserves due to the targeted nature of the funds for Ukraine defense purposes. Net revaluation effect of the NBU reserves was at positive US$0.4bn.

ICU view: The inflows of the foreign financial aid in the form of grants and loans was insignificant in March and April, and FX sale interventions by the NBU were not offset with the inflows of fresh donor money. Now that the EU Ukraine Support Loan has been approved, we expect larger funding inflows and NBU reserves should recover to above US$50bn swiftly. The NBU will, thus, remain in a comfortable position to control the FX market and the hryvnia exchange rate at least through end-2027.

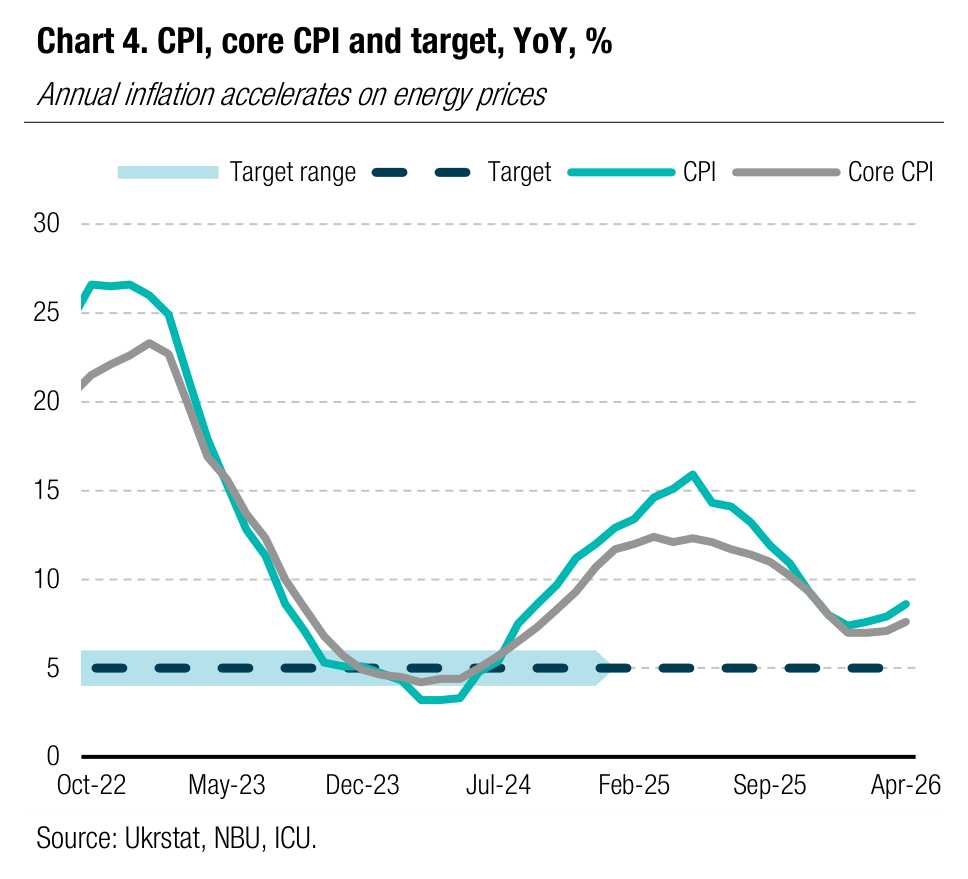

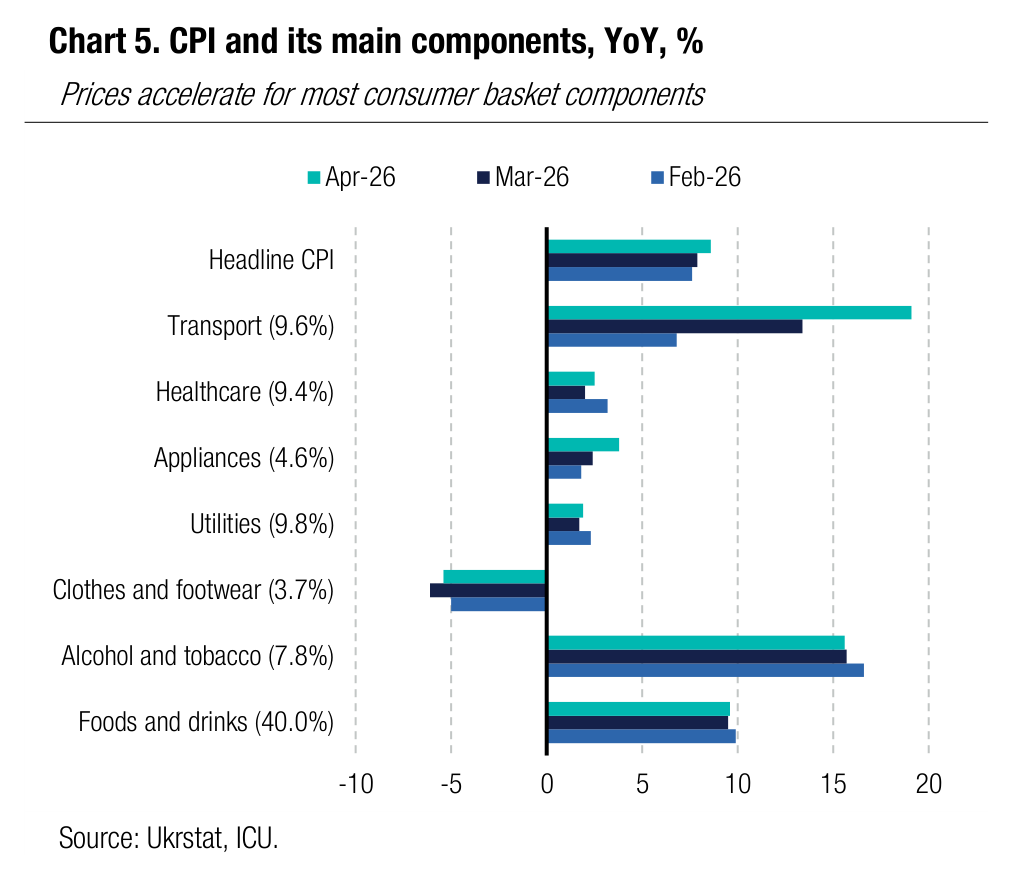

Economics: Inflation speeds up on energy costs

Annual CPI accelerated to 8.6% in April from 7.9% in March. Core inflation up to 7.6% YoY.

In monthly terms, consumer inflation was up 1.4% in April with prices for food contributing around 0.7-0.8pp. and prices for motor fuel and transportation contributing around 0.4pp. In YoY terms fuel and transportation prices accelerated to 19.1%, the rate last seen in 2Q23. Food prices were up 1.9% MoM with annual pace accelerating only marginally to 9.5% from 9.3% in March. Annual price growth picked up across the majority components of consumer basket.

|  |

ICU view: April inflation statistics reflect the spike in global energy prices due to Iran war, which started to show secondary effects as goods producers and service providers continue to pass higher fuel costs on customers. Also, secondary effects have not yet fully transpired and may add to inflationary pressures in the coming months if the energy crisis is not resolved. Our base-case scenario assumes the global oil prices will decrease meaningfully by the end of 2Q, but even so, end-year inflation is now likely to be in the range of 8ꟷ9%.

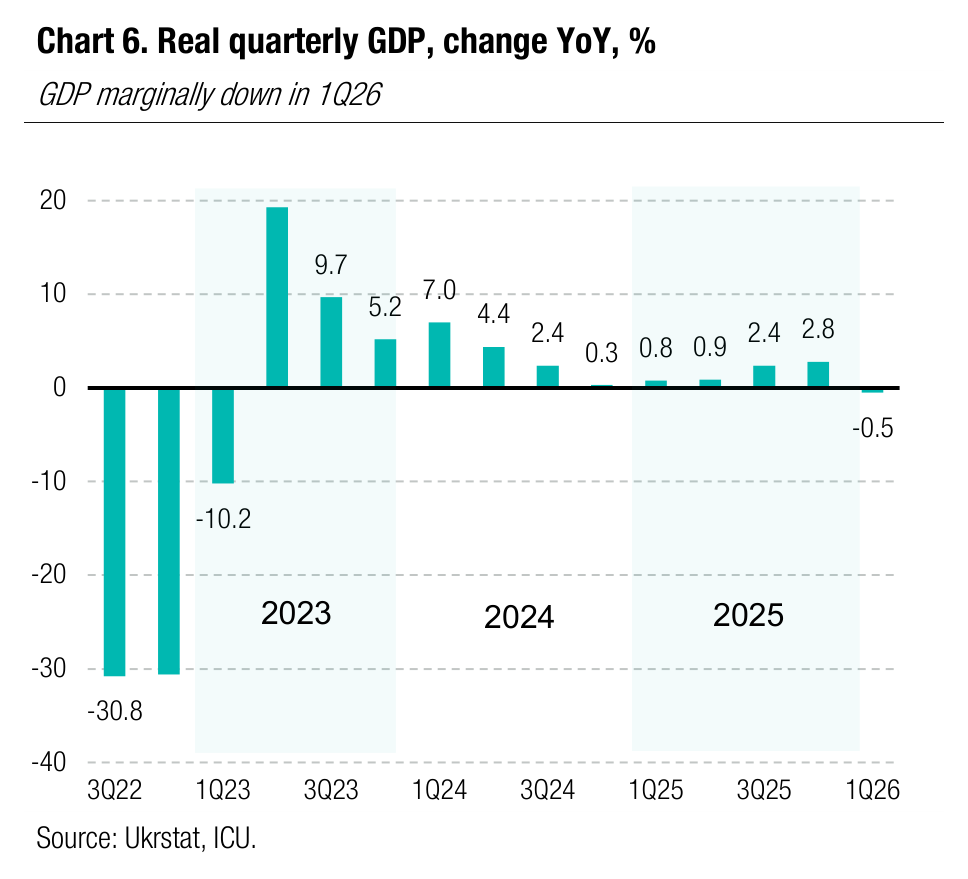

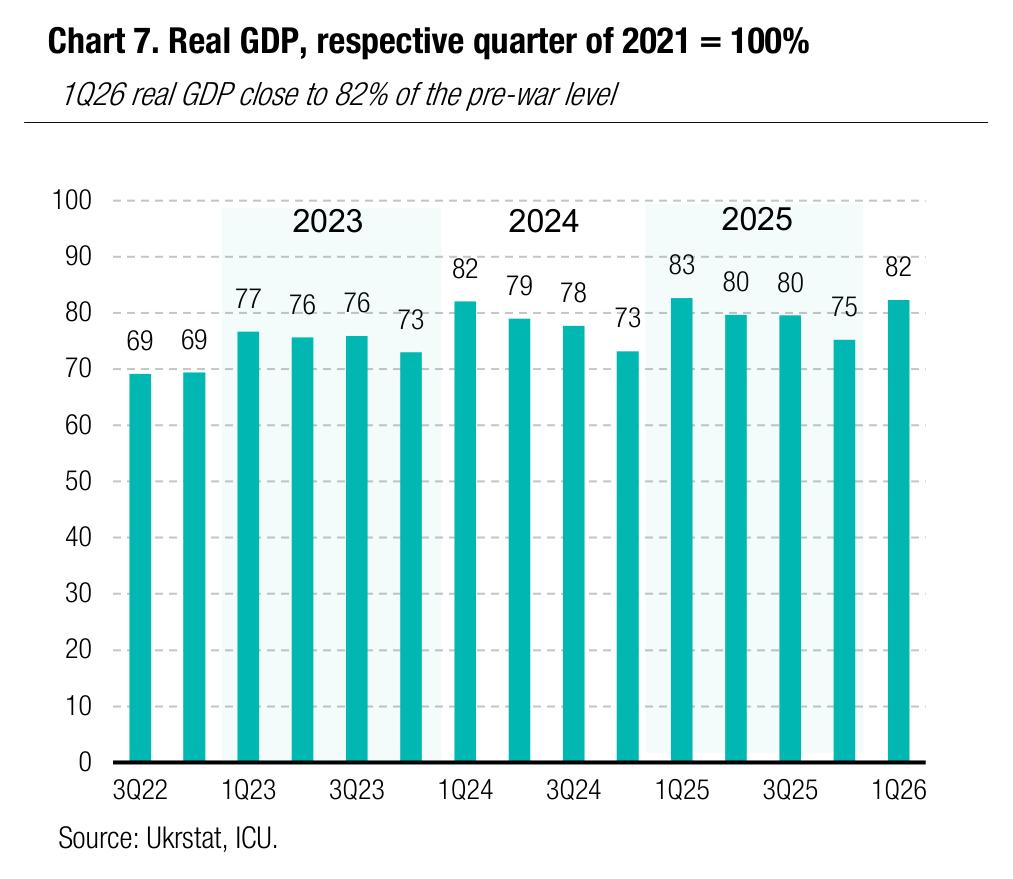

Economics: GDP edges down in 1Q26

Ukraine’s GDP was down 0.5% YoY in 1Q26 according to UkrStat preliminary estimates.

|  |

ICU view: The breakdown of GDP components will be available in June. At this stage it is clear that massive power blackouts in January and February due to russia’s attacks on energy infrastructure were the main culprit of the economic contraction. We expect the situation to improve and the economy to return to growth in 2Q26 but we think the existing constrains, including the security situation and weak business / consumer sentiment will keep the full year growth close to 1% YoY.