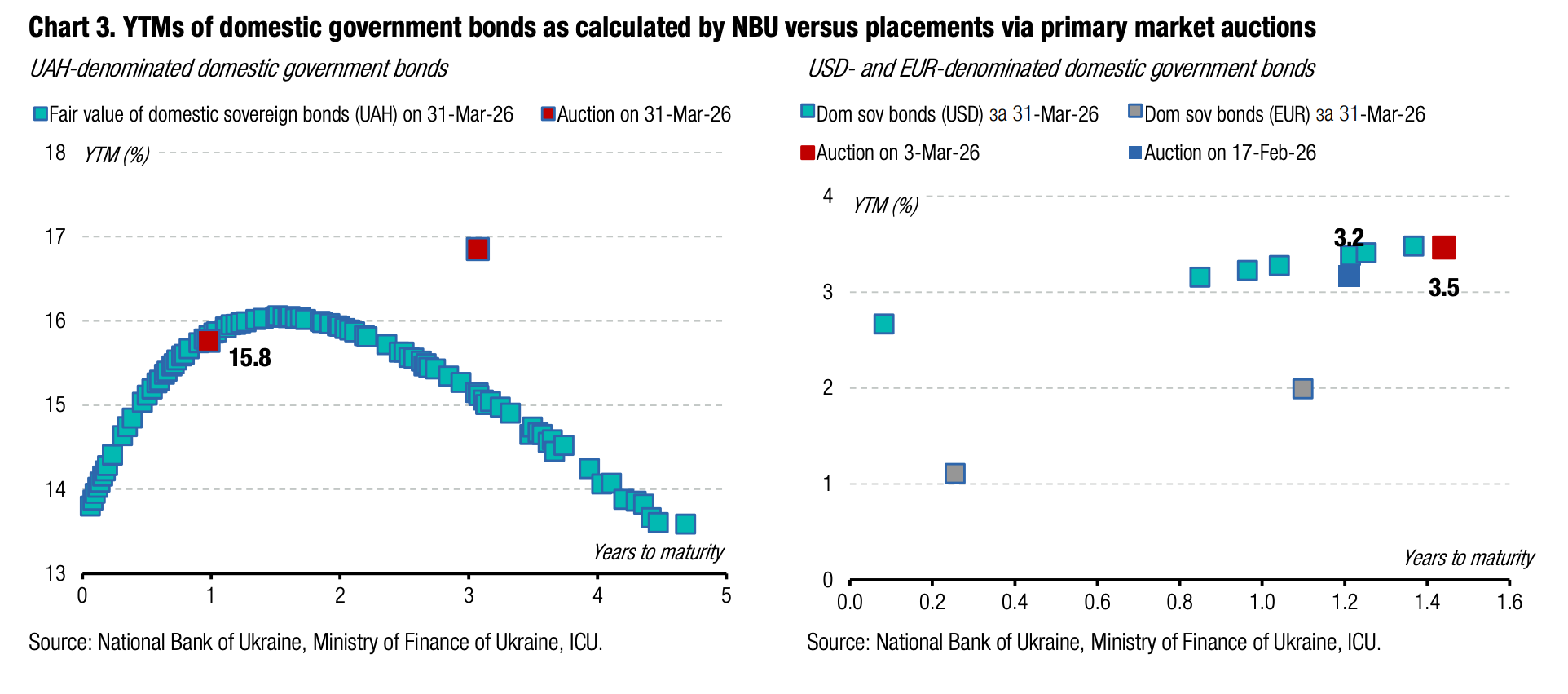

|  |  |

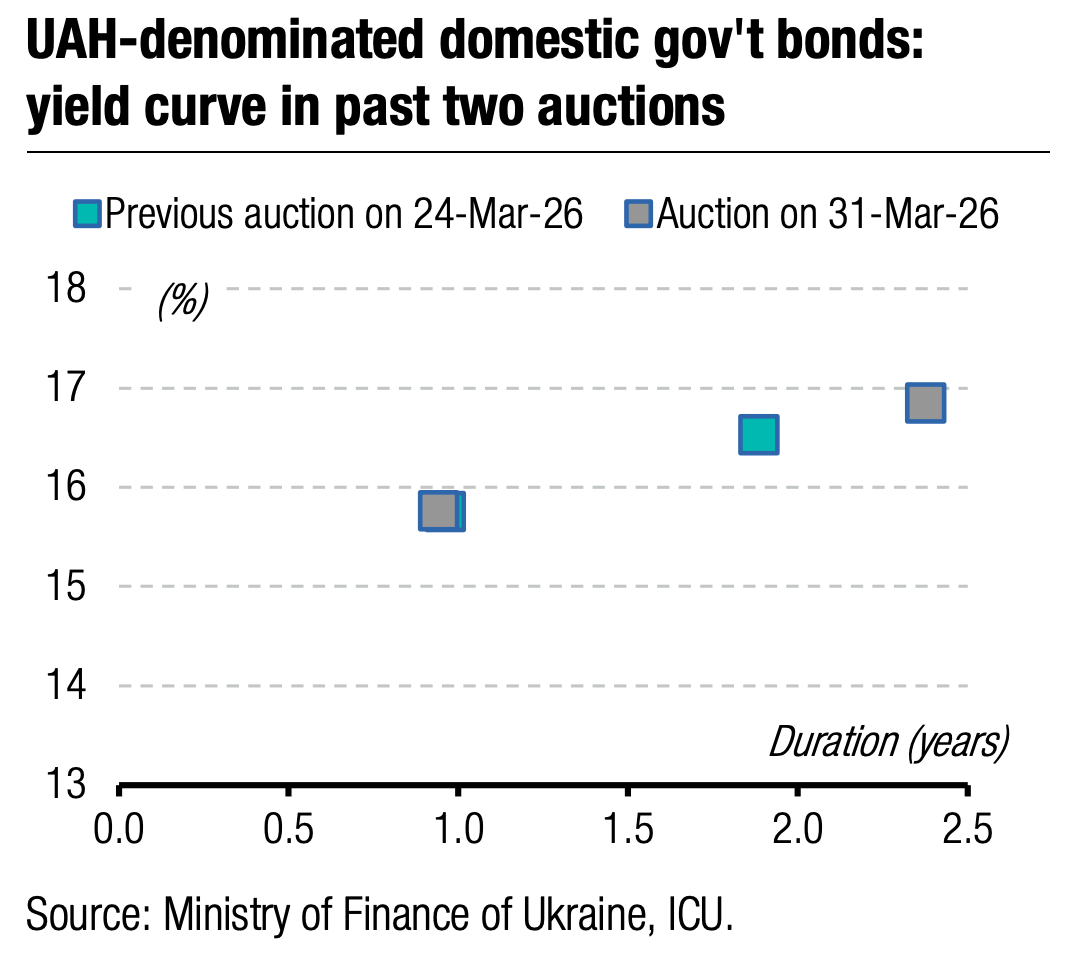

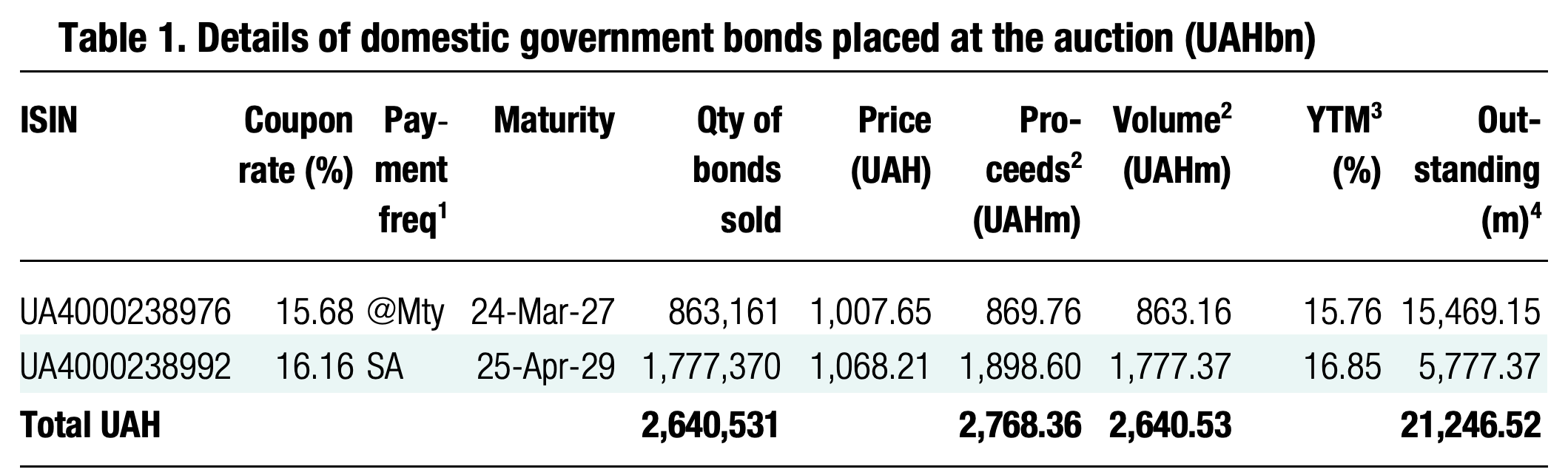

Yesterday's auction demonstrated that the hype around the decline in yields has died down, and bid rates have stabilised mostly at the cut-off level. Demand has fallen below supply, so there is currently no prospect of a further decline in yields.

Bidders for the one-year military bills submitted 22 bids, totalling less than UAH 0.9 bn, i.e., only 43% of the cap. Yields were in the range of 15ꟷ15.15%, i.e. without claims for rate increases. The cut-off remained at 15.15% for the fourth week, and the weighted average yield came very close to it at 15.14%.

Note: [1] payment frequency abbreviations: M - monthly, Qtly - quarterly, SA - semi-annually, @Mty - at maturity date; [2] proceeds and volumes for the USD-denominated bonds are calculated based on the previous day's exchange rate 43.91/USD, 50.95/EUR; [3] yields on coupon-bearing bonds are effective yields to maturity. Sources: Ministry of Finance of Ukraine, Bloomberg, ICU.

The range of bid yields for the three-year note was the same, only 15bp, from 16% to 16.15%. However, the volume of bids with rates below the maximum was insignificant, so the weighted average rate was similar to the cut-off rate – 16.15%. However, total demand amounted to UAH1.8bn, which is 11% below the cap and almost 2x that of the one-year paper.

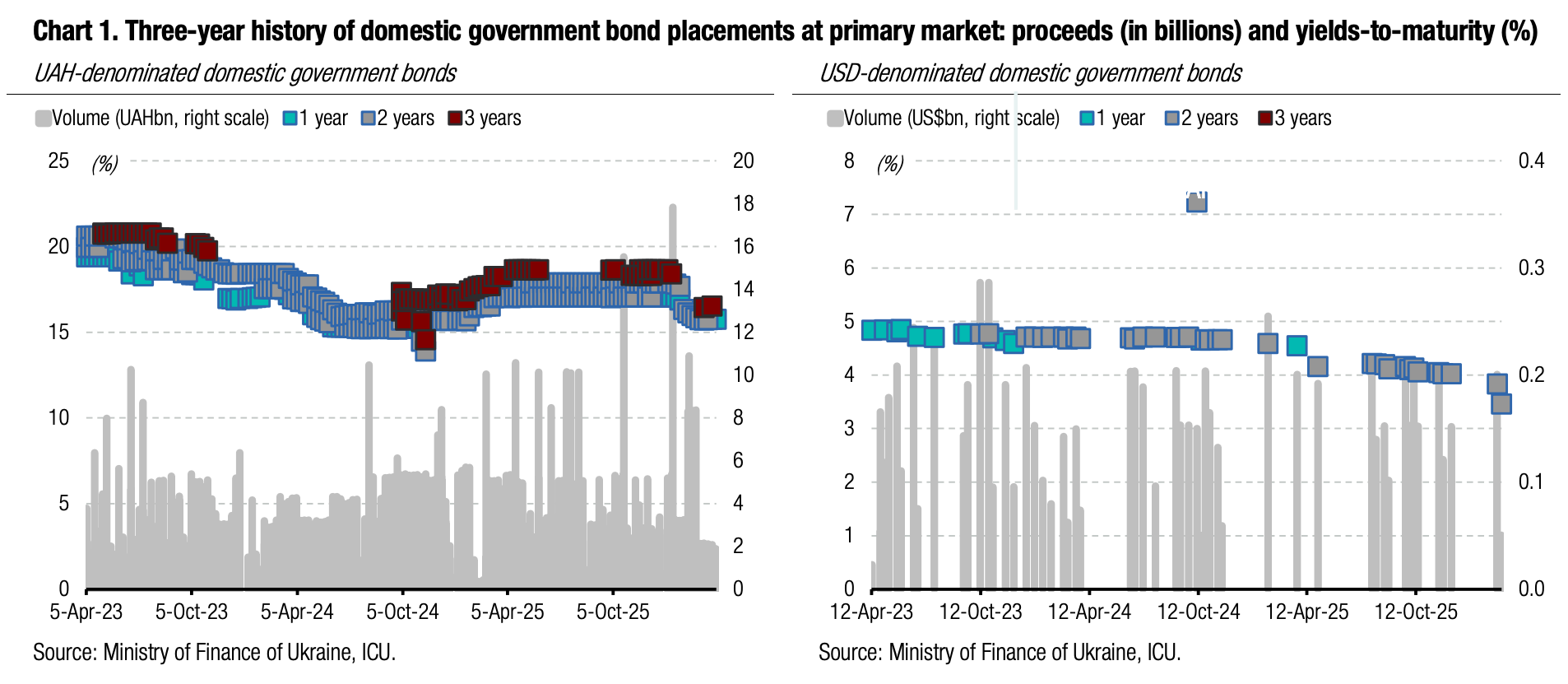

Thus, the yields of one-year bills in the primary market have decreased by 120bp YTD, or 2.4x of the NBU key rate cut, and the yields of three-year notes by 165bp, or more than 3x the NBU key rate cut. The term premium that buyers of three-year securities receive in addition to the yield of one-year bonds is 100bp, or 45bp less than at the beginning of the year.

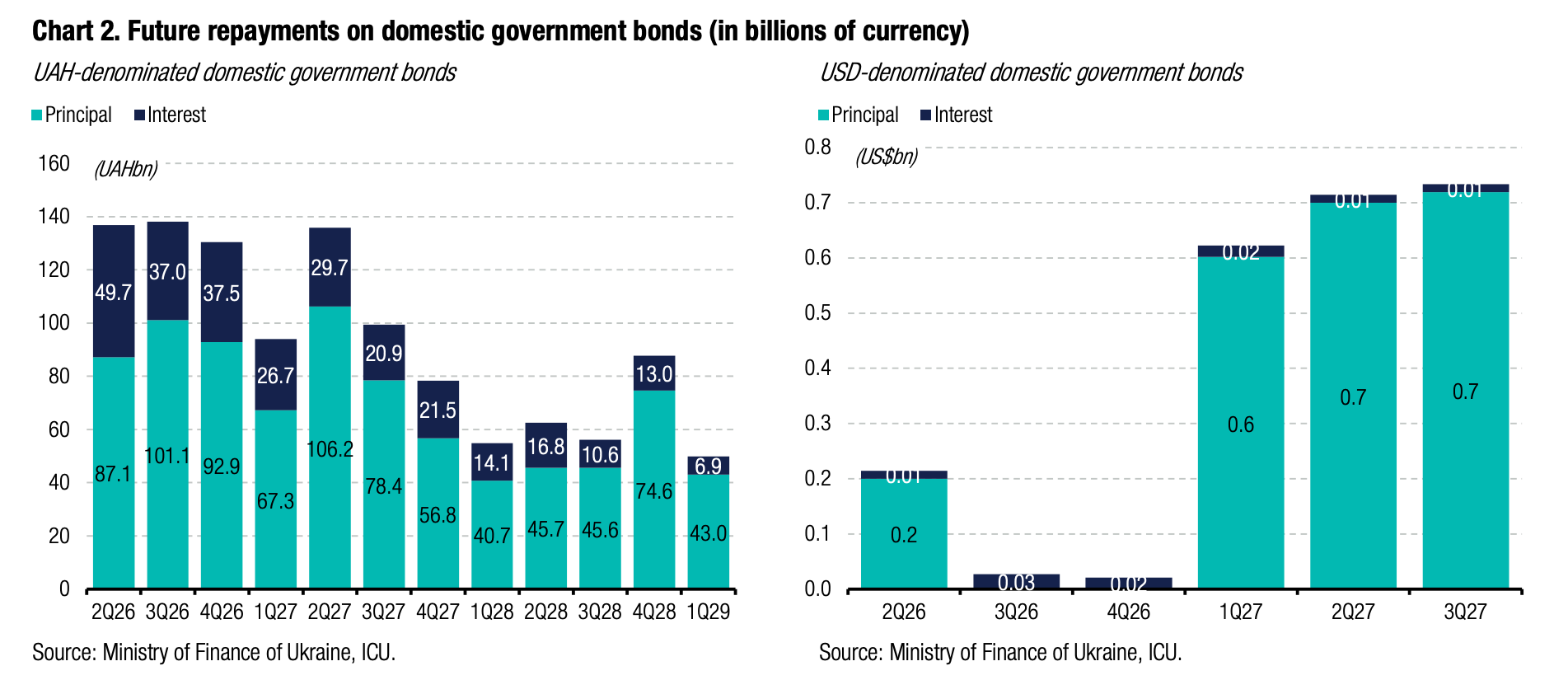

Appendix: Yields-to-maturity, repayments