|  |

|  |

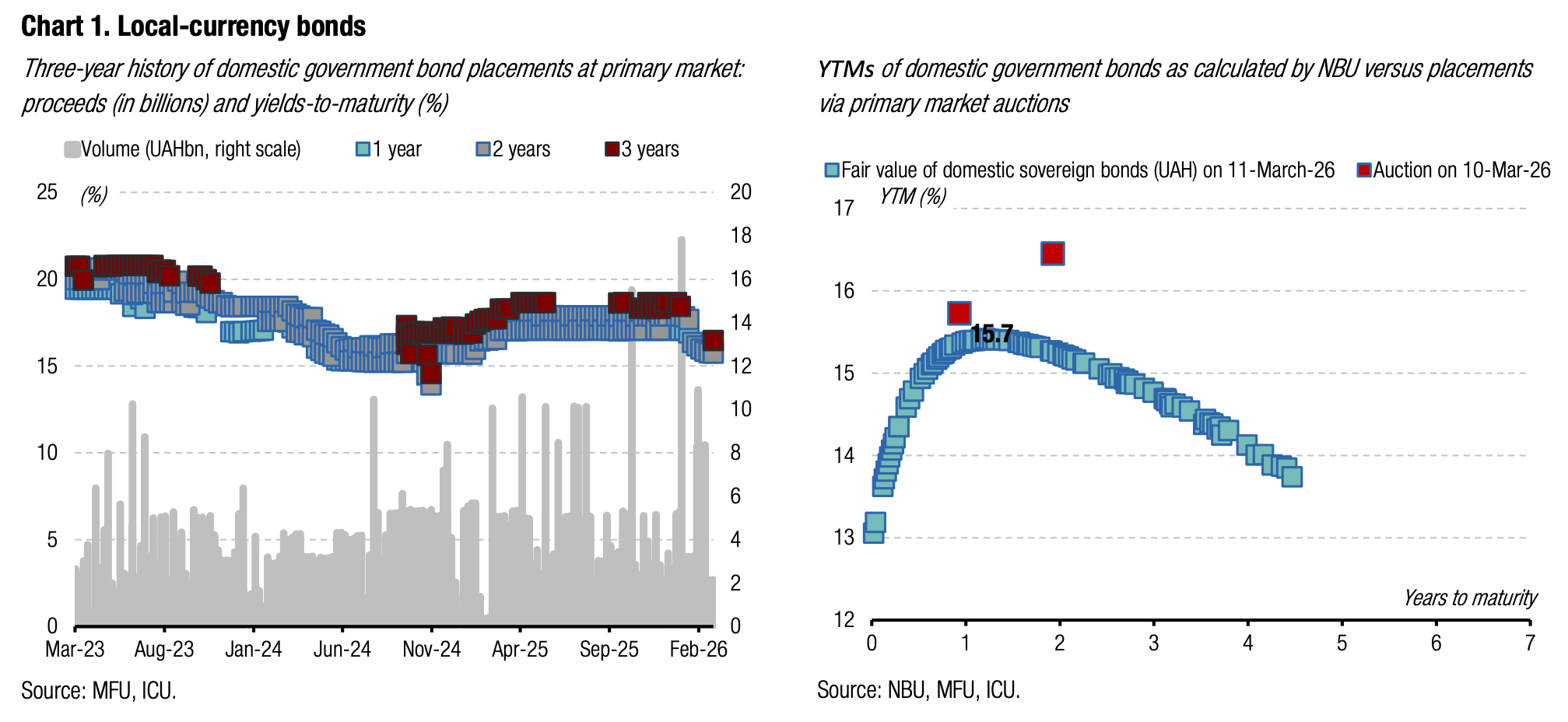

Bonds: Investor focus on longer-term securities deepens

Investors in UAH bonds are increasingly focusing on longer-term instruments amid a several-week-long downward drift in yields at MoF's primary auctions.

Last week, the secondary bond market focused primarily on bonds with maturities of one to two years. These instruments accounted for 42% of trading. Another 36% of the volume was with securities due in two to three years. The share of bills with maturities of up to one year was only 17%. Such a trading structure is significantly different from the first week of March, when trades were distributed almost evenly between these three groups.

The largest volume of transactions was with four securities that mature at the end of March 2027 (12%), in June 2027 (10%), in September 2028 (19%), and in March 2029 (8% of the total volume of trading in UAH bonds).

YTMs in the secondary market continued to decline. YTMs of bonds due June 2027 and September 2028 decreased by almost 50bp over the past week, by approximately 120bp over the past four weeks, and by approximately 200bp YTD. Moreover, the current YTM for paper maturing in March 2029 is at least 20bp lower than for bonds maturing in September 2028.

ICU view: The MoF's gradual steps to reduce yields in the primary market have significantly outpaced the NBU's rate cuts, thereby affecting yields in the secondary market. The term premium is narrowing significantly, and the yield curve shows signs of inversion for some segments on the back of investors' drive to lock in current yield levels for a longer period. Although we do not expect a change in the NBU's key rate at this week's monetary policy meeting, the National Bank may well cut the rate later in 1H26. Meanwhile, the Ministry of Finance will likely continue to encourage investors to compete in the primary market, and bond yields may continue to decline further, albeit at a slower pace.

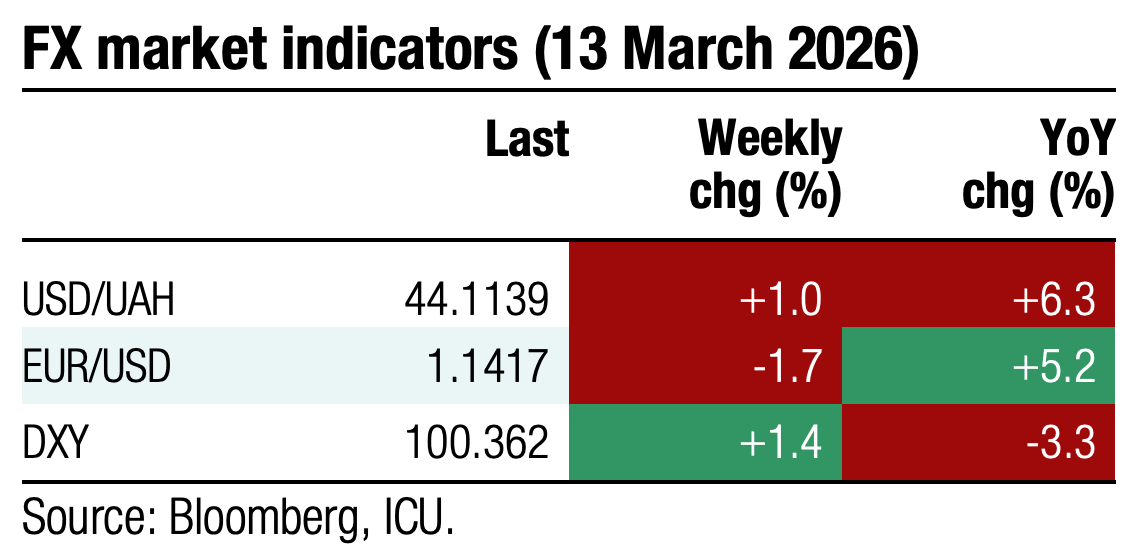

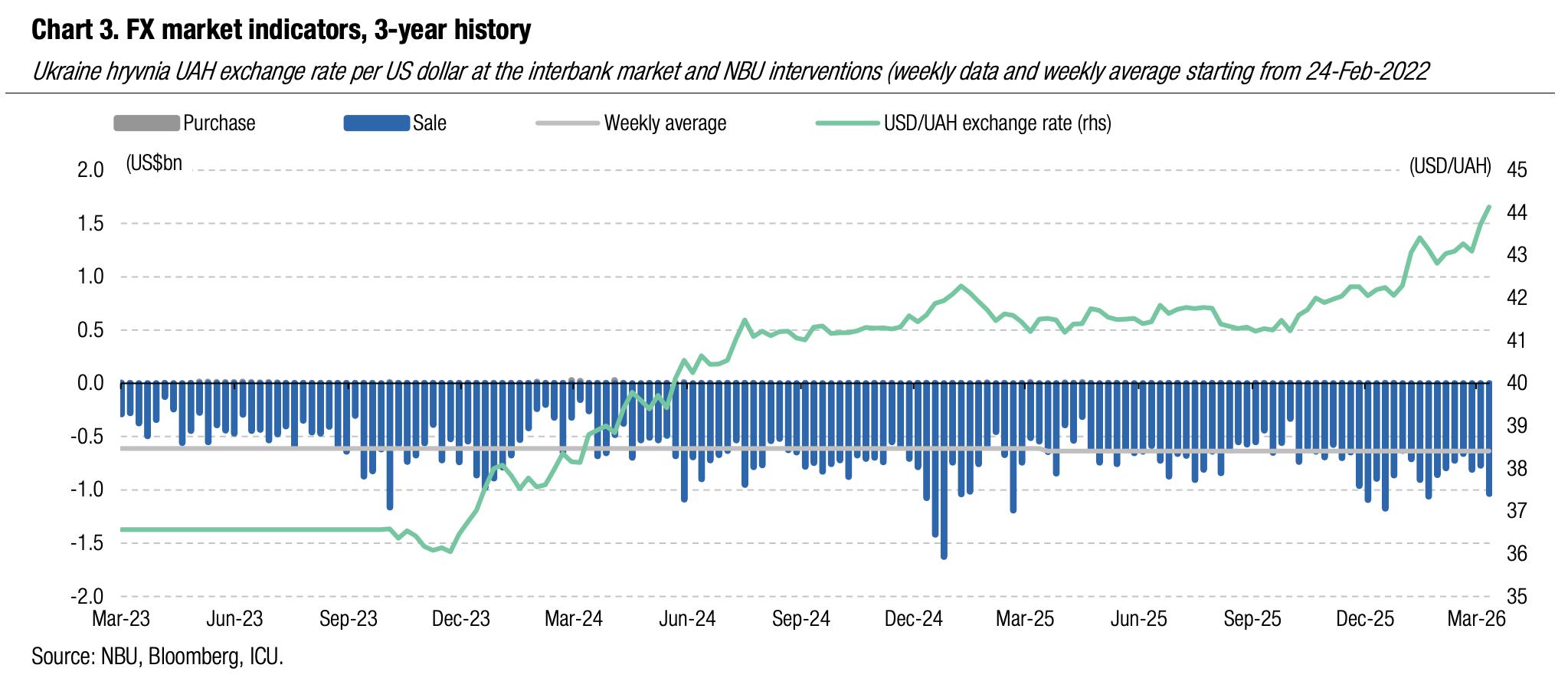

FX: NBU continues to weaken hryvnia

The National Bank weakened the hryvnia exchange rate to over UAH44/US$ last week; it stood firm to prevent further depreciation on Friday.

The total foreign currency shortage slid by 6% WoW to US$594m with increase in the interbank FX market and significant decline, by 36%, in the retail segment. These data exclude Friday numbers that will be available later.

At the same time, the National Bank significantly increased interventions. Over the week, it sold over US$1bn, and nearly a third of that on Friday.

On Thursday, quotes in the interbank FX market reached UAH44.3/US$ (with the official rate set at UAH44.16/US$ for Friday), a new historic low for the hryvnia vs. US$. The official hryvnia exchange rate is set at UAH44.14/US$ today, so the hryvnia has weakened by 0.9% WoW and by 4.2% YTD.

ICU view: Last week’s hryvnia weakening likely exceeded the NBU’s desired pace and the central bank stood firm on Friday to prevent further depreciation. We remain of the view that the NBU must take steps to strengthen the hryvnia temporarily to prevent depreciation expectations from solidifying. Therefore, we expect the NBU to fully curb FX market imbalances and return the exchange rate to below UAH44/US$ this week.

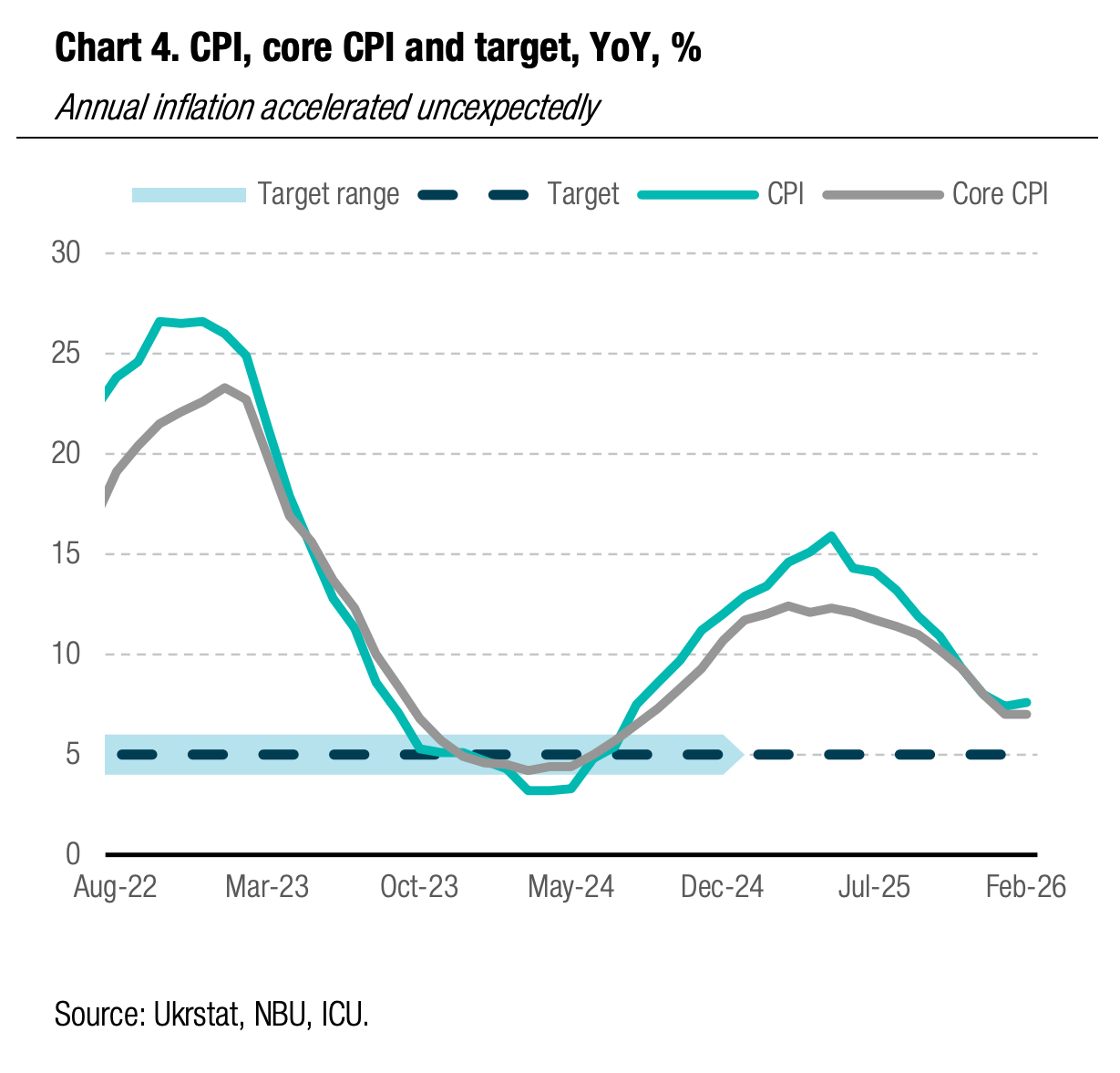

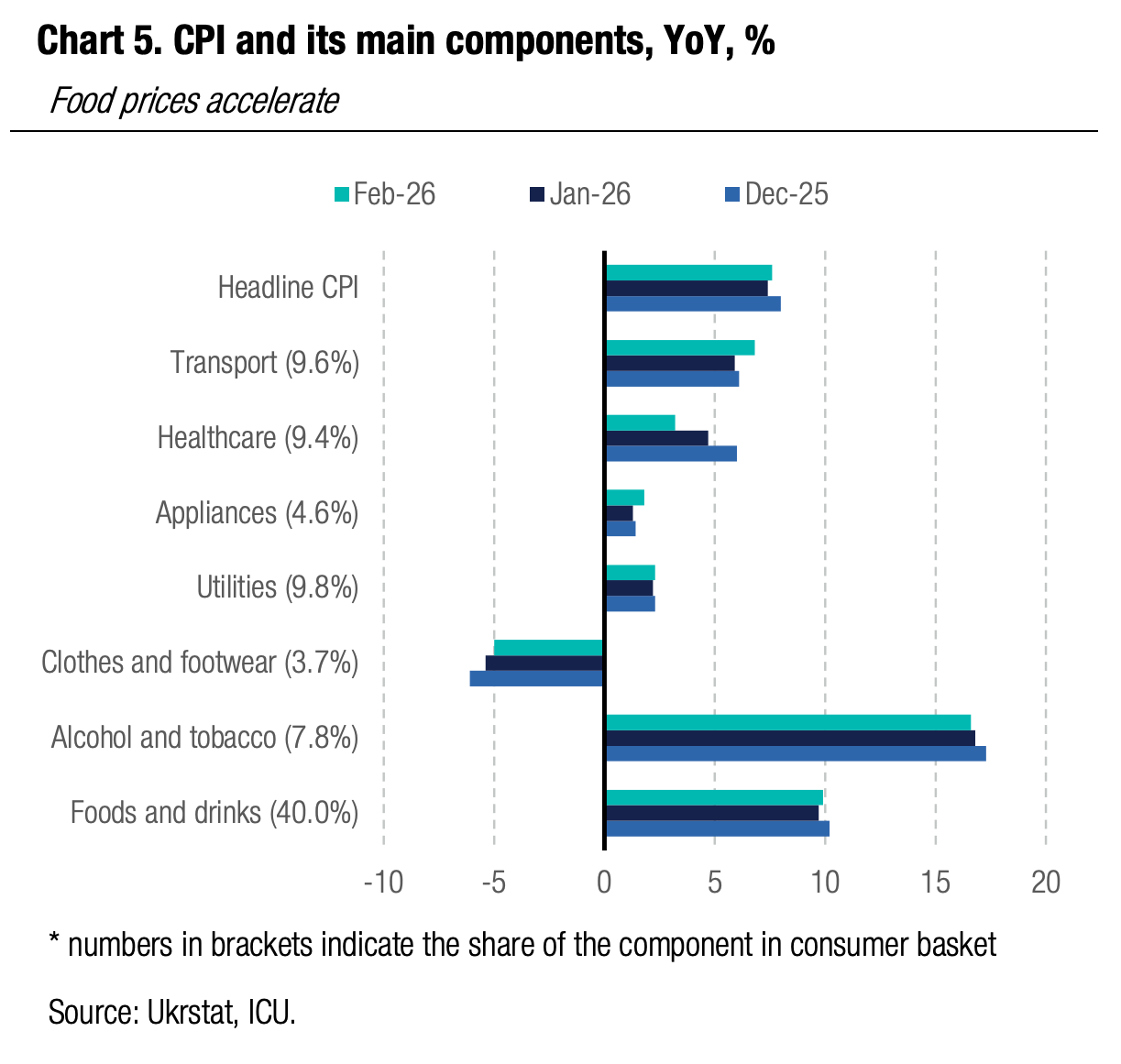

Economics: Consumer prices accelerate unexpectedly

Annual headline CPI climbed to 7.6% in February from 7.4% in January.

The pick up in CPI primarily came on the back of food as food prices accelerated to 9.7% in February from 9.5% a month before. Within the food category, fruits and vegetables were the key contributors to higher prices. Other noteworthy price moves include acceleration in communication tariffs (as mobile network operating companies pass higher cost of alternative electricity supplies onto customers) and in the transportation segment (as motor fuel prices started to pick up before the outbreak of the Iran war). Prices for hotels and restaurants – the segment that is very sensitive to labor-cost pressures – continued to decelerate marginally in February.

|  |

ICU view: Acceleration of inflation in February was a negative surprise as we expected a marginal deceleration of the annual pace last month. The key explanation for this discrepancy is an unusually high increase in prices for fruits and vegetables in February. Looking forward, we expect the downward inflation trend to resume in March, driven by the stability of food prices. A spike in motor fuel prices on the back of the Iran war will definitely have negative first and second round effects to consumer prices and is now a major risk to our end-2026 CPI forecast of 6.3%. Yet, other than that, the mix of inflationary and deflationary factors remains in line with our expectations. Given significant uncertainty around the length of the global oil shortages and persistence of high motor fuel prices, we expect the NBU will keep the key policy rate unchanged this week but will likely resume cuts later in 2Q26.